MNI ASIA MARKETS ANALYSIS: Fed Speakers Return, Miran Low Dot

HIGHLIGHTS

- Treasuries look to finish near early session lows Friday, random walk session with no obvious headline or flow driver for a midmorning bounce.

- Fed speakers are back from media blackout following Wednesday's 25bp rate cut: Mn Fed Kashkari does "not believe we should be on a preset course for a series of rate cuts."

- New Fed Governor Miran confirms in a CNBC appearance that he was the bottom dot on the new Dot Plot that saw rates ending the year at 2.75-3.00% (implying a total of 150bp of cuts going into the September meeting).

- Stocks extended record highs - Information Technology sector shares continued to lead gainers in the second half.

US TSYS

MNI US TSYS: Tsys Finishing Near Lows, Fed Speakers Out of Blackout

- Treasuries look to finish near session lows Friday, no obvious headline, data, Block or knock-on support in EGBs for random moves off lows.

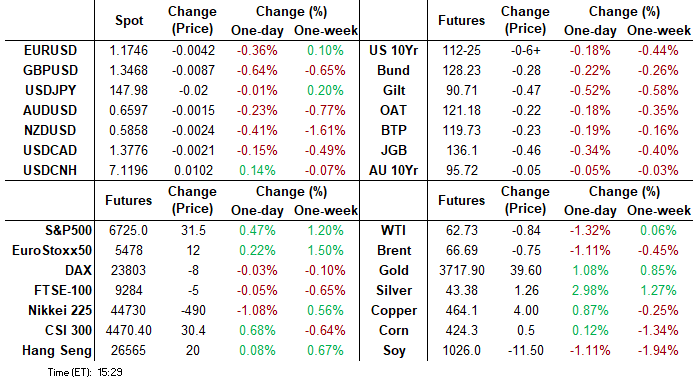

- Currently, the Dec'25 10Y trades -6 at 112-25.5 (yld 4.1293% +.0249) vs. 112-22 low - initial technical support at 112-23.5/112-15.5 (Low Sep 19 / High Aug 5 and 14); resistance well above at 113-29 (High Sep 11 and the bull trigger). Curves mildly steeper: 2s10s +1.056 at 54.941, 5s30s +.037 at 105.990.

- Fed speakers returned from media blackout after Wednesday's 25bp rate cut:

- New Fed Governor Miran confirms in a CNBC appearance that he was the bottom dot on the new Dot Plot that saw rates ending the year at 2.75-3.00% (implying a total of 150bp of cuts going into the September meeting).

- SF Fed President Daly didn't reveal much about her current rate view in a Q&A at an AI conference. She's probably one of the members on the "median" of 3 cuts in the updated September Dot Plot, but doesn't vote in 2025 or 2026.

- Mn Fed Kashkari does "not believe we should be on a preset course for a series of rate cuts."

- The dollar index trades in positive territory Friday, exhibiting session gains of around 0.3% as we approach the close. Broadly, the greenback maintains a very supportive tone following the solid post-Fed recovery, with the DXY now residing ~1.5% above the fresh cycle lows that were printed on Wednesday.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.14% (-0.24), volume: $2.894T

- Broad General Collateral Rate (BGCR): 4.11% (-0.24), volume: $1.154T

- Tri-Party General Collateral Rate (TCR): 4.11% (-0.24), volume: $1.125T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.08% (-0.25), volume: $92B

- Daily Overnight Bank Funding Rate: 4.08% (-0.25), volume: $185B

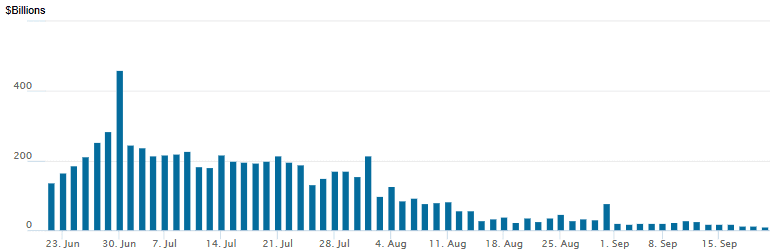

FED Reverse Repo Operation

RRP usage slips to new low of $11.363B with 13 counterparties this afternoon from $13.707B Thursday, usage at lowest levels since early April 2021. Compared to this year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR & Treasury option flow looked mixed overnight: Treasury calls and SOFR puts on modest volumes. Underlying futures extending lows ahead the NY open, TYZ5 back to September 4 levels.

Projected rate cut pricing recedes slightly from late Thursday levels (*): Oct'25 at -22.8bp (-22.9bp), Dec'25 at -45bp (-44.4bp), Jan'26 at -56.7bp (-56bp), Mar'26 at -69.5bp (-69.1bp).

SOFR Options:

+2,000 SFRV5/SFRX5 96.37 straddle spd, 5.0 net

+25,000 SFRZ5 96.00/96.12 3x2 put spds, 1.5-1.75 ref 96.345

+10,000 2QZ5 96.37/96.50 put spds, 1.5 ref 96.895

5,950 SFRZ5 96.00/96.12/96.50/96.62 put condors

+2,500 SFRZ5 96.00/96.18 put spds vs. 96.43/96.62 call spds, 0.0 net

+1,000 SFRZ6 99.00/100.00/101.00 call flys, 1.5

2,500 0QZ5 96.68/96.93/97.18 call flys ref 96.99

+2,800 2QZ5 96.37/96.50 put spds, 1.5 ref 96.895

+3,000 SFRX5 96.12/96.31/96.43 broken put flys, 1.75 vs. 96.31/0.05%

+12,500 3QZ5 95.87/96.25 put spds, 2.5 ref 96.70

Treasury Options:

-8,000 TYX5 111.5/140 strangles, 30

over +38,500 TYZ5 111 puts, 20 ref 112-24.5 (includes strangles below)

4,000 TYZ5 111/112 strangles ref 112-25

4,700 TUZ5 103.87/104.37/104.5/104.87 broken put condors

3,000 TYV5 111/112 strangles, ref 112-27

2,700 TUX5 103.75/104.87 strangles ref 104-10.5

+12,500 TYV5 113 straddles, 35 ref 112-29, appr vol 4.26%, expires nest week

8,000 TYX5 109/110 put spds ref 112-24.5

over -30,000 TYV5 113/TYX5 111.5 put, 12 net/Oct over - paper bought Oct put on Tuesday is rolling out and down

over 20,000 TYX5 111.5 puts, 14-15

over -21,900 TUV5 104.37 puts, 7-6.5

-1,500 TYX5 114 calls, 16

-3,000 wk2 TY 113 calls, 30 ref 112-28/0.46% (exp 10/10)

+2,500 TYV 113.25 calls, 9 vs. 112-28.5/0.30%

over 4,100 USV5 115 puts, 8 last

-5,000 wk3 FV 109.5 puts, 5-4.5

2,200 TYX5 114 calls, 16 ref 112-25

5,000 TUZ5 105.25 calls, ref 104-09.88

+1,500 USX5 118/121 call spds, 35 ref 116-11

+1,800 TYV5 112 puts, 3 vs. 112-25/0.10%

MNI BONDS: EGBs-GILTS CASH CLOSE: Gilts Underperform On Renewed Fiscal Concerns

European curves bear steepened lightly Friday.

- Gilts underperformed, with the latest UK public sector borrowing figures showing further fiscal deterioration and weighing on the long-end.

- Elsewhere, the calendar was relatively light to conclude a busy week. In dovish-leaning data: German PPI came in below consensus, while French employment expectations weakening.

- With no impactful US data in the European afternoon, German and UK yields closed at/near both session and weekly highs.

- The UK and German curves both bear steepened on the day. Periphery / semi-core EGB spreads tightened around 1bp.

- The week as a whole saw light twist steepening in the UK curve (2Y -0.2bp, 10Y +4.4bp), with the German curve bear steepening (2Y +0.5bp, 10Y +3.3bp).

- Next week's European calendar is a little lighter, and headlined by September flash PMIs.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 1.2bps at 2.023%, 5-Yr is up 2bps at 2.326%, 10-Yr is up 2.2bps at 2.748%, and 30-Yr is up 2.8bps at 3.337%.

- UK: The 2-Yr yield is up 2.1bps at 3.982%, 5-Yr is up 2.9bps at 4.132%, 10-Yr is up 3.9bps at 4.715%, and 30-Yr is up 5.2bps at 5.559%.

- Italian BTP spread down 1.2bps at 78.5bps / Spanish down 1.2bps at 54.8bps

MNI EGB OPTIONS: No Shortage Of Large Euribor Structures To Close Week

Friday's Europe rates/bond options flow included:

- RXV5 128/127ps, sold at 17 in 6k

- RXV5 127.5/126.5/125/123p condor vs 130/131.5cs, bought the cs for -6 and -5.5 in 10k (said to be closing)

- RXX5 127.50/126.50/125.50/123.00 broken put condor vs 130.00/132.00cs, bought the Condor for 2 in 7.25k

- ERZ5 98.12/98.25cs, bought for 1 in 10k

- ERZ5 98.06/98.12cs sold at 0.75 in over 20k Total

- ERH6 98.12/98.25 call spread paper paid 2.75 on 10K

- ERM6 98.25/98.3125/98.375c fly, bought for 0.25 in ~28k

- ERU6 98.8125/98.6875/98.5625/98.4375 put condor, paper pays 1.5 in 4k

- SFIM6 96.90/97.00cs, bought for 1 in 5k

- SFIM6 96.40/96.60/96.80c fly vs 96.00p, bought the fly for -0.25 up to flat in 7.5k

MNI FOREX: Notable Dollar Recovery Following Sharp Swings This Week

- The dollar index trades in positive territory Friday, exhibiting session gains of around 0.3% as we approach the close. Broadly, the greenback maintains a very supportive tone following the solid post-Fed recovery, with the DXY now residing ~1.5% above the fresh cycle lows that were printed on Wednesday. Despite the impressive 1.65% range this week, the DXY is just a modest 0.05% higher since last Friday’s close.

- The week’s most notable move was for EURUSD, given the pair briefly extended above 1.19 for the first time since mid-2021 and substantially narrowing the gap to the psychological and popular year-end forecast level of 1.2000. Short-term weakness back towards the 1.1750 region is considered technically corrective at this juncture.

- Keeping it in the majors, USDJPY also made a false range breakout, briefly sliding below the 146.21 bear trigger and sliding down to 145.50. Subsequently, a strong reversal has been assisted by a bullish candle pattern on Wednesday - a hammer formation - providing an early reversal signal. Immediate resistance is now at 148.27/28, and a continuation higher would open 149.14, the Sep 3 high. Notably, the pair shrugged off two hawkish dissents from BOJ board members, emphasising the renewed bearish pressure on the yen.

- Friday has provided a potentially pivotal moment for the UK and GBP. Overall, fiscal data shows that borrowing is overshooting the OBR's forecast YTD by GBP11.4bln providing a gloomy outlook as we approach the budget, and keeping sterling under pressure.

- GBPUSD has fallen 0.62% on Friday, and while the pair’s adjustment has been fairly in line with the broader dollar strength, a weekly close back below the 1.36 breakout point and below both the 20- and 50-day EMA’s is a bearish development. The next support to watch lies at 1.3433, a trendline support drawn from the Aug 1 low.

- For EURGBP, we have risen back above 0.8700, renewing the focus on the year’s highs at 0.8769.

- Weaker economic data in both New Zealand and Australia notably dampened sentiment for AUD and NZD, however, it’s worth noting this week that AUDNZD looks set to close at the highest level in 3 years, above 1.1250.

MNI US STOCKS: Late Equities Roundup: DJIA & Nasdaq Making New Record Highs Again

- Stocks are drifting higher late Friday, the DJIA and Nasdaq managing to make new highs while S&P eminis approximately 5 ticks off Thursday's high print at the moment.

- Currently, the DJIA trades up 139.41 points (0.3%) at 46280.21 vs. 46321.85 high, S&P E-Minis up 20.25 points (0.3%) at 6713.75 vs. 6719.25 high yesterday, Nasdaq up 109.3 points (0.5%) at 22581.41 vs. 22591.74 high.

- Information Technology sector shares continued to lead gainers in the second half, carry over support in chip stocks after Nvidia announced a $5B investment and AI infrastructure collaboration with Intel yesterday. Apple +3.37%, Fortinet +3.32%, Palantir Technologies +3.09%, Oracle +2.52% and Intuit +1.85%.

- Meanwhile, Consumer Discretionary and Utility sector shares also supported indexes: Eversource Energy +5.65%, Constellation Energy +1.80%, Evergy +1.42%, Tesla +2.08%, Starbucks Corp +1.34% and Marriott Int +1.17%.

- On the flipside, Energy and Health Care sector shares led decliners in the second half, oil and gas shares weighed on the former as crude prices waned (WTI -0.90 at 62.67): Targa Resources -3.34%, ONEOK -3.14%, Devon Energy -3.03% and Occidental Petroleum -2.58%.

- Lastly, Health Care sector was weighed down by pharmaceutical makers and service providers: Dexcom -10.02%, Humana -5.38%, Hologic -4.12% and Moderna -2.51%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bulls Remain In The Driver’s Seat

- RES 4: 6787.63 1.382 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6750.50 2.000 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6748.50 1.236 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6719.75 High Sep 18

- PRICE: 6713.75 @ 14:26 BST Sep 19

- SUP 1: 6589.32 20-day EMA

- SUP 2: 6536.50 Low Sep 8

- SUP 3: 6477.53 50-day EMA

- SUP 4: 6417.25 Low Aug 12

A bull cycle in S&P E-Minis remains intact and the contract traded to a fresh cycle high yesterday. Price has breached the 6700.00 handle and this signals scope for an extension towards 6748.50, a Fibonacci projection point. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend and positive market sentiment. Initial support to watch lies at 6589.32, the 20-day EMA.

COMMODITIES

MNI AMERICAS OIL: Americas End of Day Oil Summary: Crude Lower

WTI crude is slightly lower today amid oversupply concerns, while the EU’s 19th sanctions package was announced today in line with expectations. Heavier selling could retest $57.71, the May 30 low.

- The EU’s 19th sanctions package has been adopted by the EC with a focus on a faster phase out of Russian LNG, expanded sanctions on the shadow fleet and sanctions on refineries using Russian oil in third countries.

- Focus remains on US President Trump's calls for nations to stop buying Russian oil to help end the conflict in Ukraine. Trump said the conflict would end "if the price of oil comes down," as he continues to call for countries to stop buying Russian fuel, Bloomberg said

- Ukraine strikes on Russian energy infrastructure are supportive after strikes were reported at two refineries yesterday. Russian runs have fallen below 5mb/d and the lowest since April 2022, JPMorgan said.

- China appears unlikely to sustain another strong wave of crude stockpiling in the near term and growth looks set to plateau, Vortexa said.

- WTI Oct futures were down 1.4% at $62.68

- WTI Nov futures were down 1.3% at $62.40

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 22/09/2025 | 1230/0830 | * | Industrial Product and Raw Material Price Index | |

| 22/09/2025 | 1230/1330 | BOE Pill At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/1545 | ECB Lane At BIS-ECB-SUERF Workshop | ||

| 22/09/2025 | 1345/0945 | New York Fed's John Williams | ||

| 22/09/2025 | 1400/1600 | ** | Consumer Confidence Indicator (p) | |

| 22/09/2025 | 1400/1000 | St. Louis Fed's Alberto Musalem | ||

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 22/09/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 22/09/2025 | 1600/1200 | Cleveland Fed's Beth Hammack | ||

| 22/09/2025 | 1600/1200 | Richmond Fed's Tom Barkin | ||

| 22/09/2025 | 1715/1315 | BOC Sr Deputy speaks at LSE panel on supervision | ||

| 22/09/2025 | 1800/1900 | BOE Bailey Fireside Chat On Supervision | ||

| 22/09/2025 | 1945/1545 | BOC Deputy Kozicki speaks at BIS panel on central bank frameworks | ||

| 23/09/2025 | 2300/0900 | *** | Judo Bank Flash Australia PMI | |

| 23/09/2025 | - | Riksbank Meeting |