MNI ASIA MARKETS ANALYSIS: Fed Delivers Expected 25Bp Cut

HIGHLIGHTS

- Treasuries look to finish broadly lower, well off the initial knee-jerk rate-cut reaction highs as markets digest a less than rosy/cautious messaging from the Fed amid meaningful downside risks.

- Chairman Powell: "it's not a bad economy ... t's challenging to know what what to do ... there are no risk free paths. Now it's not incredibly obvious what to do."

- Mixed messages within the summary of economic projections questioned the overall dovish narrative and subsequently the US dollar aggressively reversed higher alongside US treasury yields.

US TSYS

MNI US TSYS: Markets Whipsaw after Fed Delivers 25Bp Cut

- US Treasuries look to finish near late session lows, completely reversing the initial rate cut move rally - to weaker across the board after the bell with Dec'25 10Y futures just through early session low of 113-08 t0 113-02 (-15.5), 10Y yield +.0439 4.0718%.

- Treasury futures had extended highs after the FOMC annc 25bp rate cut, Fed Gov Miran the sole dissenter in favor of a 50bp cut. Tsy Dec'25 10Y futures climbing +8 to 113-25.

- Still digesting mixed messaging, Chairman Powell: "it's not a bad economy ... it's challenging to know what what to do ... there are no risk free paths. Now it's not incredibly obvious what to do."

- Meanwhile "downside risks to employment have risen," the Fed said in its post-meeting policy statement. "Job gains have slowed, and the unemployment rate has edged up but remains low. Inflation has moved up and remains somewhat elevated."

- However, a confident sounding Chair Powell on the US economy as a whole and the mixed messages within the summary of economic projections questioned the overall dovish narrative and subsequently the US dollar aggressively reversed higher alongside US treasury yields.

- Focus turns to Thursday's weekly claims Leading Index and Net TIC Flows.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.39% (-0.12), volume: $2.857T

- Broad General Collateral Rate (BGCR): 4.36% (-0.14), volume: $1.139T

- Tri-Party General Collateral Rate (TCR): 4.36% (-0.14), volume: $1.115T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $98B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $191B

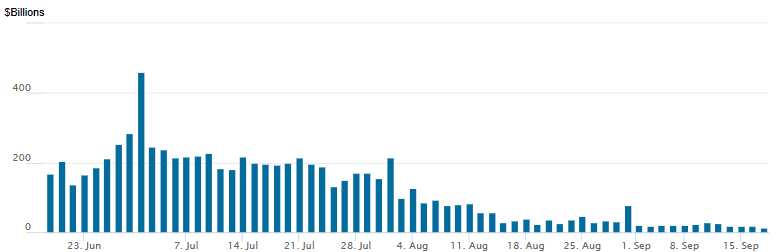

FED Reverse Repo Operation

RRP usage retreats to new lowest levels since early April 2021 this afternoon: $13.963B with 14 counterparties vs. $18.817B Tuesday. Today's drop compares to $16.954B on Monday. This year's high usage of $460.731B occurred on June 30.

US SOFR/TREASURY OPTION SUMMARY

Heavier SOFR & Treasury option flow leaning hawkish prior to underlying futures near lows after reversing the initial rate-cut knee-jerk reaction, projected rate cut pricing cools slightly vs. early morning levels (*): Oct'25 at -22bp (-46.4bp), Dec'25 at -45bp (-69.1bp), Jan'26 at -57.7bp (-82.9bp).

SOFR Options

+12,000 SFRX5 95.62/95.75 call spds, 1.0 vs. 96.325/0.05%

+2,500 SFRH6 96.37 puts, 8.0 ref 96.60

+20,000 SFRV5 96.50 calls, 2.25 vs. 96.345/0.20%

Block/screen -100,000 0QZ5 97.00/97.25 call spds, 10.0

+2,500 SFRZ5 96.00/96.18/96.50/96.75 call condors 12.5

+10,000 2QZ5 96.75 puts, 7.0 ref 97.005

+5,000 SFRH6 96.00/96.25 put spds 2.5 over 0QH6 96.50/96.75 put spds

3,000 0QZ5 97.25/2QZ5 97.18 call spds

+10,000 SFRZ5 95.81/95.93/96.06 put flys, 0.75

+2,000 SFRV5 96.37/96.50/96.62 call flys, 2.25

Block, 5,000 2QX5 97.12/97.37/97.50 broken call flys, 4.75 net/splits

+3,500 SFRF6 96.00/96.31/96.50 broken put flys, 2.75

+4,000 SFRX5 96.00/96.06/96.12/96.18 put condors, 1.0

2,000 SFRZ5 96.43/96.56 1x2 call spds ref 96.36

1,800 0QX5 97.37/97.62/97.75 broken call flys ref 97.105

over 6,300 SFRX5 96.18 puts ref 96.36

3,500 SFRF6 96.00/96.3196.50 broken put flys ref 96.615

-4,200 0QV5 96.81 straddles, 31.0 ref 97.105

+3,000 SFRZ5 95.93/96.06/96.18 put flys, 1.5

+3,000 SFRZ5 95.93/96.06/96.18 2x3x1 put flys, 0.5 ref 96.355

+5,000 SFRZ5 96.75/97.00 call spds, 1.25 ref 96.355

+5,000 SFRZ5 96.25 puts, 6.5

-3,500 0QV5 96.93 puts, 3.5

Treasury Options:

3,000 TUX5 105 calls ref 104-12.88

+30,000 Wed/wkly FV 110/110.25 call spds ref 109-27.25

over +15,000 FVV5 109.5 puts, 7-8.5

over 6,000 FVV5 108.75/111.25 strangles ref 109-27.75

-2,000 wk1 TY 113.25 puts, 25 vs 113-18.5/0.40%

+2,000 TYV5 112.5 puts, 5 vs. 113-16.5/0.10%

+5,000 TYV5 113 puts, 11

3,000 wk3 US 119 calls, 9

over 6,000 TYV5 112.5 puts, 5 last ref 113-19.5

+2,000 wk3 FV 109.5 puts, 3.5

+3,500 TYV5 114.25 calls, 9

+4,000 TYX5 112.5 puts, 21

+2,000 TYV5 114/114.5 call spds 7 vs. 113-16/0.16%

over 6,500 wk3 TY 113 puts, 4 ref 113-19 to -19.5 (exp 9/19)

MNI EGB OPTIONS: Call Structures Bought In Sonia And Euribor Wednesdays

Wednesday's Europe rates/bond options flow included:

- ERH6 98.00/98.0625cs x1 vs 98.4375/97.875^^ x0.5, bought the cs for 1 in 8k total

- ERM6 98.375/98.25/97.9375p ladder, sold in ~4.58k, just over 5k Total on the day

- SFIZ5 96.15/96.20/96.25/96.30c condor, bought for 0.75 in 10k Total

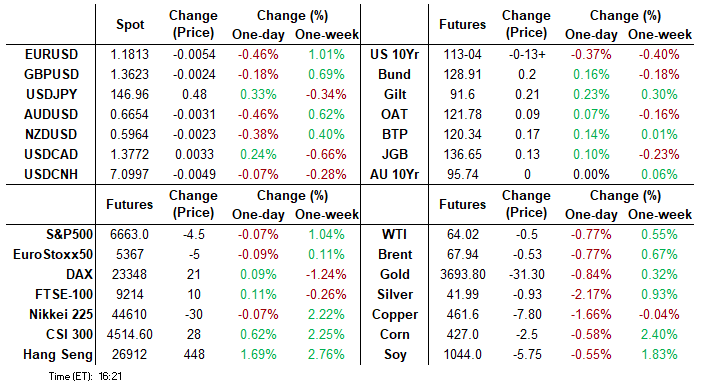

MNI FOREX: Sharp Reversal Higher for US Dollar After DXY Prints Cycle Lows

- The initial reaction to the Fed’s 25bp rate cut and dovish adjustments to the statement was a sharp selloff for the US dollar. This marked a continuation of the recent theme of greenback weakness and prompted the USD index to briefly break to the lowest point since February 2022. Most notably, this propelled EURUSD to a high of 1.1919.

- However, a confident sounding Chair Powell on the US economy as a whole and the mixed messages within the summary of economic projections questioned the overall dovish narrative and subsequently the US dollar aggressively reversed higher alongside US treasury yields.

- The USD index rallied around 0.8%, with the likes of EURUSD and USDJPY reversing nearer to 1%.

- For USDJPY in particular, the false break below the bear trigger of 146.21 places a significant focus on today’s daily close and whether bearish momentum can be sustained for the pair. Markets will be aware of the risks surrounding the LDP leadership and Friday’s BOJ meeting.

- EURUSD rose to a high of 1.1919, within four pips of the 2.00 proj of the Feb 28 - Mar 18 - 247 price swing. Separately, GBPUSD traded as high as 1.3726 before trading back to 1.3650 as we approach the APAC crossover and tomorrow’s BOE meeting. Cycle highs for cable reside at 1.3789, the July 1 and key resistance.

- New Zealand GDP and Australian employment data kick off the Thursday calendar, before the focus turns to Norges bank and BOE decisions.

MNI US STOCKS: Late Equities Roundup: DJIA Off New Record High

- Stocks remain mixed late Wednesday - the DJIA still in positive territory, but well off initial post-FOMC rate cut highs (a new record in fact) as accounts took profits amid a less than rosy/cautious messaging from the Fed following the 25bp rate cut.

- Currently, the DJIA trades up 266.13 points (0.58%) at 46013.35 (record high of 46261.95), S&P E-Minis down 1.25 points (-0.02%) at 6665.75, Nasdaq down 53.7 points (-0.2%) at 22276.93.

- Information Technology and Consumer Discretionary sector shares underperformed in late trade: tech stocks remain under pressure after reports China authorities have banned the sale of Nvidia chips to top technology firms: Broadcom -3.95%, NVIDIA -3.15%, Oracle -2.99%, Palantir Technologies -2.67% and Intel -2.53%

- Mohawk Industries -5.01%, Ralph Lauren -3.49%, Hilton Worldwide -3.05% and Marriott International -2.33% weighed on the Consumer Discretionary sector.

- On the positive side, Financial and Consumer Staples shares led gainers in late trade, banks and services stocks buoyed the former: W R Berkley +2.14%, Citizens Financial Group +2.03%, US Bancorp +2.03% and American Express +1.89%

- Meanwhile, retail sellers held modest gains: Dollar Tree +2.44%, Philip Morris Int +2.18%, Procter & Gamble +1.50% and Walmart +1.49%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Bulls Remain In The Driver’s Seat

- RES 4: 6750.50 2.000 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 3: 6748.50 1.236 proj of the Aug 1 - 15 - 20 price swing

- RES 2: 6712.33 1.764 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6700.00 Round number resistance

- PRICE: 6662.50 @ 1520 ET Sep 17

- SUP 1: 6559.62 20-day EMA

- SUP 2: 6506.50 Low Sep 5

- SUP 3: 6452.53 50-day EMA

- SUP 4: 6417.25 Low Aug 12

A bull cycle in S&P E-Minis remains intact and the contract is trading closer to its recent highs. A fresh cycle high yesterday reinforces current bullish conditions. The move higher confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on the 6700.00 handle next and 6712.33, a Fibonacci projection. On the downside, initial support to watch is 6569.89, the 20-day EMA.

MNI COMMODITIES: Crude Falls, Precious Metals Lose Ground Post Fed

- WTI has fallen today following a large crude stock draw, with a further decline following the Fed’s announcement of a 25bp cut to rates.

- However, crude is still holding onto most of the week’s gains, supported by Russian supply risks amid Ukrainian attacks on energy infrastructure and potential sanctions.

- WTI Oct 25 is down by 0.8% at $64.0/bbl.

- The Fed signalled two more cuts this year, with the median projection of fed funds rate at end-2025 at 3.6%.

- The trend condition in WTI futures remains bearish, with sights on initial resistance at $61.29, the Aug 13 low and the bear trigger, followed by $57.71, the May 30 low. On the upside, initial resistance to watch is $66.03, the Sep 2 high.

- Meanwhile, spot gold has fallen during Fed Chair Powell’s press conference, after some short-lived volatility around the Fed decision, which saw the yellow metal briefly reach a fresh record high at $3,707.6/oz.

- The yellow metal is currently down by 1.0% $3,652/oz.

- Gold remains in a clear bull cycle, with the next objective at $3,705.2, a Fibonacci projection, which was briefly pierced earlier. On the downside, initial firm support lies at $3,558.8, the 20-day EMA.

- Elsewhere, silver has notably underperformed today, with the precious metal currently down by 3.0% at $41.3/oz and extending losses post the Fed decision.

- Trend signals in silver remain bullish and the latest pullback is considered corrective. Sights are on $42.974 next, a Fibonacci projection. Support to watch is $40.721, the 20-day EMA.

THURSDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 18/09/2025 | 0710/0910 | ECB Lagarde Video Message at Women Leadership Summit | ||

| 18/09/2025 | 0800/1000 | *** | Norges Bank Rate Decision | |

| 18/09/2025 | 0800/1000 | ** | EZ Current Account | |

| 18/09/2025 | 0800/1000 | ECB de Guindos at MNI Connect Event | ||

| 18/09/2025 | 0900/1100 | ** | EZ Construction Output | |

| 18/09/2025 | 0945/1145 | ECB Schnabel Chairs Panel at ECB Research Conference | ||

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1100/1200 | *** | Bank Of England Interest Rate | |

| 18/09/2025 | 1230/0830 | *** | Jobless Claims | |

| 18/09/2025 | 1230/0830 | ** | WASDE Weekly Import/Export | |

| 18/09/2025 | 1230/0830 | ** | Philadelphia Fed Manufacturing Index | |

| 18/09/2025 | 1430/1030 | ** | Natural Gas Stocks | |

| 18/09/2025 | 1530/1130 | * | US Bill 08 Week Treasury Auction Result | |

| 18/09/2025 | 1530/1130 | ** | US Bill 04 Week Treasury Auction Result | |

| 18/09/2025 | 1700/1300 | ** | US Treasury Auction Result for TIPS 10 Year Note | |

| 18/09/2025 | 1915/1515 | BOC speech on payments ecosystem from director Ron Morrow. | ||

| 18/09/2025 | 2000/1600 | ** | TICS | |

| 19/09/2025 | 2301/0001 | ** | Gfk Monthly Consumer Confidence | |

| 19/09/2025 | 2330/0830 | *** | CPI | |

| 19/09/2025 | 0200/1100 | *** | BOJ Policy Rate Announcement |