MNI ASIA MARKETS ANALYSIS: Early Tariff Headline Risk Recedes

HIGHLIGHTS

- Treasuries gapped higher early Friday after Pres Trump's unexpected 25% tariff threat on Apple followed by 50% tariffs on EU this morning.

- Risk-off rate rally saw 10Y yield fall to 4.4456% low on the move while stocks gapped lower (SPX eminis tapped 5869.25 low). Both spent much of the session gradually unwinding the moves -

- Mollified to a degree after after Tsy Sec Bessent claimed that the "US is far along in trade talks with India and other Asian countries...most countries are negotiating in good faith except the EU," adding that the deals are "moving quickly".

US TSYS

MNI US TSYS: Unwinding Early Tariff-Tied Headline Risk

- Early Friday headline risk on tariffs again - spurred a fast risk-off reaction in markets after Pres Trump's unexpected 25% tariff threat on Apple followed by 50% tariffs on EU this morning.

- Treasuries gapped higher, Jun'25 10Y tapped 110-17.5 high (10Y yld 4.4456% low) while SPX emins traded down to 5756.5 from 5858.75 prior to the headlines. Both spent much of the session gradually unwinding the moves -

- Mollified to a degree after after Tsy Sec Bessent claimed that the "US is far along in trade talks with India and other Asian countries...most countries are negotiating in good faith except the EU," adding that the deals are "moving quickly".

- Heavy volumes on the day (TYM5 over 3.7M) tied to Jun'25/Sep'25 roll, Sep takes lead quarterly next Friday.

- The prevailing theme of dollar weakness in recent months played out again this week, prompting the Bloomberg dollar index to fall ~1.65% this week and print fresh yearly lows in the process.

- Extended weekend with Monday's Memorial Day holiday. Tuesday Data Calendar: Durables, Cap Goods, Consumer Confidence, split times for Tsy bills and 2Y Note auctions next Tuesday.

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.26% (+0.00), volume: $2.540T

- Broad General Collateral Rate (BGCR): 4.26% (+0.00), volume: $1.046T

- Tri-Party General Collateral Rate (TCR): 4.26% (+0.00), volume: $1.017T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $302B

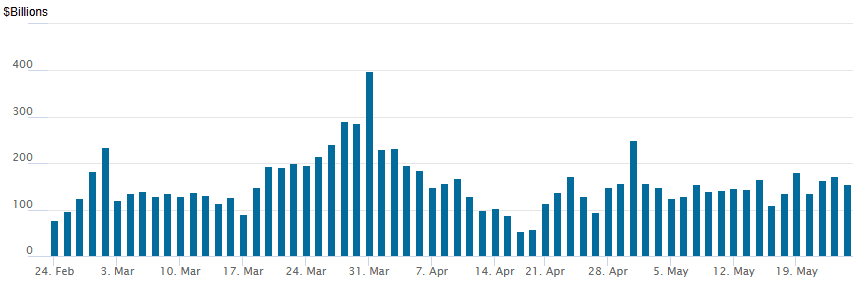

FED Reverse Repo Operation

RRP usage recedes to $154.841B this afternoon from $173.018B yesterday, total number of counterparties at 39. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Decent option volumes after underlying futures jumped on Pres Trump's unexpected 25% tariff threat on Apple followed by 50% tariffs on EU this morning. Better Treasury calls on net (Jun options expire today), SOFR options more mixed while underlying have unwound much of the initial move. Projected rate cut pricing retreated vs. morning levels (*) as follows: Jun'25 at -0.05 (-1.3bp), Jul'25 at -6.2bp (-7.5bp), Sep'25 at -17.8bp (-21.2bp), Oct'25 at -30.7bp (-35.5bp), Dec'25 at -47.6bp (-53.5bp).

SOFR Options:

Block, 5,000 SFRZ5 96.00 puts, 15.0 vs. 96.24/0.34%

-4,000 SFRZ5 96.25 straddles, 55.0 ref 96.20

-2,500 SFRU5 95.93 straddles 31.5-31.0

over 26,000 0QZ5 96.00 puts, 10.5 ref 96.75

2,500 0QN5 96.5/96.75/97.12 call flys ref 96.745

2,100 SFRU5 95.43/95.62 2x1 put spds ref 95.94

+3,000 SFRM6 95.37/95.75/96.12 put flys, 5.0 ref 96.635

4,000 SFRM5 95.68/95.75 put spds ref 95.6825

-5,000 SFRU5/SFRZ5 95.68/95.87 put spd spd 3.75/Dec over

-2,500 2QM5 96.62/96.68/97.12 call flys, 6.25 ref 96.70

+7,500 2QN5/2QQ5/2QU5 96.00/96.25/96.50 put fly strip, 12.5 total on 12 leg package

Block, 15,000 SFRM5 95.75/95.93 put spds, 17.75 ref 95.69

Block, 6,000 0QM5 97.00/97.18 call spds 2.0 ref 96.685

+5,000 SFRZ5 95.25/95.62/95.75/95.87 put condor, 3.0

+2,000 SFRH6 94.62/95.62 put spds, 4.25 ref 96.47

+5,000 SFRN5 95.56/95.62/95.75 2x3x1 put flys, 1.25 ref 95.935

+5,000 0QN5 96.50/96.75/97.12 broken call flys, 3.0 ref 96.645/0.05%

+2,000 2QN5 96.00 puts, 2.5

Treasury Options

over 11,000 TUM5 103/103.25/103.38/103.5 broken put condors ref 103-10.38

2,500 110.25 straddles, 18 ref 110-13.5

over 11,200 wk5 TY 109 puts, 3 ref 110-14.5, expire 5/30

2,000 FVU5 106.5/107.5 put spds ref 107-31.25

7,500 TYM5 110.5 calls, 6 ref 110-11.5

2,000 TYM5 110.5 straddles, 29 ref 110-15

over 9,600 TYM5 110.25 calls, 5 ref 110-06.5

+10,000 TYM5 111 calls, 2 ref 110-16.5

over 7,600 TYM5 110 puts, 9 ref 109-31

+12,000 TYM5 110.5 calls, 1 ref 110-01.5/0.05%

+3,500 TUM 103.25 puts. 0.5

3,000 TYM5 110.25/110.5 call spds 2.0 ref 110-02

MNI BONDS: EGBs-GILTS CASH CLOSE: Bunds Outperform On Trump Tariff Threat

European yields fell sharply Friday as EU-US trade tensions ratcheted up.

- After a fairly subdued start to the session, global core FI soared in a risk-off move after US President Trump first threatened to place 25% tariffs on Apple phone imports, before then "recommending a straight 50% Tariff on the European Union, starting on June 1".

- There was no word as to the outcome of a call between EU Trade Commissioner Sefcovic and US Trade Representative Greer which was to have taken place within an hour before the European cash close.

- Bunds outperformed Gilts in the aftermath of Trump's tariff pronouncement, with the UK seen relatively insulated given the recent US-UK trade agreement. Additionally, UK retail sales data surprised to the upside (for the 4th consecutive month).

- Periphery / semi-core EGB spreads widened modestly on the day, though off the widest levels of the session. There was some attention on Moody's review of Italy after hours Friday (current rating Baa3; Outlook Stable).

- On the week, both the German and UK curves steepened: the UK's twist steepened (2Y -2.2bp, 10Y +3.2bp), with Germany's bull steepening (2Y -9.1bp, 10Y -2.3bp).

- Monday is a market holiday in the UK, while the key data highlight the rest of the week is flash May inflation in multiple Eurozone countries.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 6.7bps at 1.764%, 5-Yr is down 7.5bps at 2.097%, 10-Yr is down 7.6bps at 2.567%, and 30-Yr is down 6.3bps at 3.088%.

- UK: The 2-Yr yield is down 4.8bps at 3.983%, 5-Yr is down 7.1bps at 4.13%, 10-Yr is down 7bps at 4.681%, and 30-Yr is down 7bps at 5.48%.

- Italian BTP spread up 0.8bps at 101.7bps / French OAT up 1.5bps at 69.5bps

MNI OPTIONS: Multiple Call Structures Purchased In Rates To End The Week

Friday's Europe rates/bond options flow included:

- ERM5 98.12/98.25cs, bought for half in 10k

- ERU5 98.25/98.375/98.625/98.75c condor, bought for 2 in 9.7k

- SFIQ5 96.10/96.25/96.40c fly, Bought for 2 in 5k

MNI FOREX: Bloomberg Dollar Index Extends Weekly Decline, Fresh 2025 Lows

- The prevailing theme of dollar weakness in recent months played out again this week, prompting the Bloomberg dollar index to fall ~1.65% this week and print fresh yearly lows in the process. Weakness Friday was in play across the Asian session, but then was exacerbated by renewed tariff related concerns.

- President Trump announced he would be recommending a 50% straight tariff on the EU, and while the Euro did initially come under moderate pressure, the statement appears to have further weighed on the greenback. This dynamic has been assisted by Treasury Secretary not necessarily categorising the USD as weak, bolstering the offered tone for dollar indices.

- Safe havens have performed well with the likes of USDJPY and USDCHF falling just shy of 1%. In late session trade, USDJPY has traded steadily in a 142.50-90 range, consolidating its near 4% sell-off from last week’s highs and a 2% decline this week. The immediate focus is on 142.36, the May 6 low, of which a breach would signal scope for a deeper retracement towards 139.89, the Apr 22 low and key support.

- However, it’s the antipodeans that have outperformed despite the risk-off tone for equities, with AUD and NZD rising 1.3% and 1.45% respectively on Friday. AUDUSD trend signals remain bullish. The recent consolidation phase appears to be a triangle formation - a bullish continuation signal. Attention is on key resistance at 0.6515, the May 7 high.

- Looking across Thursday and Friday, GBP stands out as one of the key outperformers, allowing cable to print above the 1.35 handle, a level not seen since February 2022. Technical breaks have emboldened the price action, following the breach of the bull trigger at 1.3444, the Apr 28 / 29 high. The next point on the chart is at 1.3550 - the Feb 24 ’22 high.

- Next week’s economic calendar is headlined by US PCE/GDP and the RBNZ May decision.

MNI FX OPTIONS: Expiries for May26 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1050(E1.0bln), $1.1300-10(E775mln)

- USD/JPY: Y143.00($663mln), Y144.00($1.1bln), Y150.00($1.8bln)

- NZD/USD: $0.5980(N$513mln)

- USD/CAD: C$1.4000-15($1.2bln)

MNI US STOCKS: Late Equities Roundup: Off Early Lows, Utilities, Staples Leading

- Stocks continued to drift in negative territory late Friday, off early session lows as markets apparently took Tsy Sec Bessent's comments on tariffs as placative. Currently, the DIA trades down down 86 points (-0.21%) at 41774.33, S&P E-Minis down 15.75 points (-0.27%) at 5841, Nasdaq down 91.5 points (-0.5%) at 18834.32.

- Tariff-tied headline risk spurred strong risk-off flows ahead of the NY open: Treasuries gapped higher while stocks sold off/extended lows after Pres Trump initially threatened Apple with a 25% tariff if iPhones weren't made in the US. Risk-off moves surged even more a few minutes later after Pres Trump stated he wants to impose 50% tariffs on the EU is in response to the Union's slow pace in talks.

- Stocks gradually moved off lows after Tsy Sec Bessent claimed that the "US is far along in trade talks with India and other Asian countries...most countries are negotiating in good faith except the EU," adding that the deals are "moving quickly".

- Information Technology and Consumer Discretionary sectors continued to underperform in late trade, the former weighed by Workday -11.75%, Super Micro Computer -3.78%, Microchip Technology -3.40%, Apple -2.64% and ON Semiconductor -2.34%.

- Concerns over tariffs weighed on outlooks as Deckers Outdoor dropped -19.53%, Ross Stores -10.87%, Lululemon Athletica -2.53% and Tapestry -2.42%.

- On the positive side, Utilities and Consumer Staples sectors continued to lead, the former buoyed by Constellation Energy +3.02%, AES Corp +2.96% and Vistra Corp +2.62%. Staples were supported by Philip Morris +1.71%, Colgate-Palmolive +1.61%, Kroger +1.37% and Kenvue +1.11%

MNI EQUITY TECHS: E-MINI S&P: (M5) Pullback Considered Corrective

- RES 4: 6080.75 High Feb 26

- RES 3: 6057.00 High Mar 3

- RES 2: 6000.00 Round number resistance

- RES 1: 5993.50 High May 20 and the bull trigger

- PRICE: 5826.00 @ 1425 ET May 23

- SUP 1: 5756.50/5715.60 Intraday low / 50-day EMA and key support

- SUP 2: 5596.00 Low May 7

- SUP 3: 5455.50 Low Apr 30

- SUP 4: 5355.25 Low Apr 24

A bullish trend condition in S&P E-Minis remains intact and the latest pullback is considered corrective - for now. Today’s sell-off has resulted in a print below the 20-day EMA, at 5775.85. A key support lies at 5715.60, the 50-day EMA. A clear break of this average is required to highlight a stronger reversal and signal scope for a deeper retracement. A resumption of gains would refocus attention on the bull trigger at 5993.50, the May 20 high.

MNI AMERICAS OIL: WTI crude Oil has moved back into positive territory

May 23 - Americas End-of-Day Oil Summary: WTI crude Oil has moved back into positive territory as markets try to digest the impact of numerous trade deal headlines in swift succession.

- The initial sell-off was sparked by the Trump Truth Social post calling for a 50% tariff on the EU starting June 1 – marking a major escalation in trade negotiations.

- The EU Commission said shortly after it would not comment on the situation until a call between the EU trade chief and U.S. trade representative was made. WSJ is reporting 11:30am ET for this.

- A recovery in oil began as U.S. Treasury Secretary spoke on Fox with comments such as he hoped the 50% tariff rate 'lights fire under the EU' to reach a deal.

- Iran is increasingly doubtful towards the prospect of reaching a nuclear deal with the US. Indirect talks between Iran and the US resumed for a fifth round in Rome but ended rather quickly.

- OPEC+ is expected to maintain its current pace of oil production increases through Q3, according to Capital Economics.

- WTI July futures were up 0.6% at $61.53

- WTI Aug futures were up 0.5% at $60.96

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 26/05/2025 | 0600/0800 | ** | PPI | |

| 26/05/2025 | 0700/0900 | ** | PPI | |

| 26/05/2025 | 1300/1500 | ECB's Lagarde On Europe's Role In A Fragmented World | ||

| 27/05/2025 | 2301/0001 | * | BRC Monthly Shop Price Index |