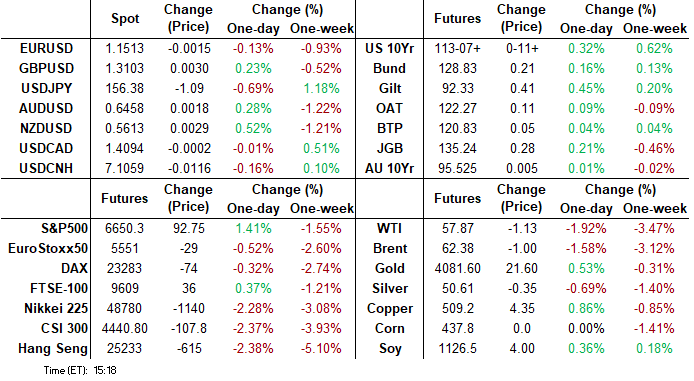

MNI ASIA MARKETS ANALYSIS: Dovish Williams on Near Term Cut

HIGHLIGHTS

- Treasury futures extended early Friday highs after NY Fed Pres Williams said he still sees the potential for a "near term rate cut".

- Treasuries held moderate gains after the S&P Global PMIs data with business activity gaining for the second consecutive month.

- Technology shares rebounded late Friday after headlines that the WH is "internally floating" sales of high-end Nvidia H200 chips to China - currently embargoed by the Trump admin to make it more difficult to further develop AI.

- The FX session has been characterised by the Japanese yen rising on Friday, halting an impressive run of weakness that has seen it fall around 6% against the dollar since the Japanese election.

US TSYS

MNI US TSYS: Dovish Fed Williams Comments Raise Chances of Dec Cut

- Treasuries look to finish stronger Friday - upper half of the range but off early knee jerk highs after NY Fed Pres Williams dovish comment he still sees potential for near term rate cut. Projected rate cut pricing: current levels vs. early morning (*): Dec'25 at -17bp (-9.3bp), Jan'26 at -26.1bp (-23.6bp), Mar'26 at -34.5bp (-35.1bp), Apr'26 at -44.1bp (-44.1bp).

- "I view monetary policy as being modestly restrictive, although somewhat less so than before our recent actions. Therefore, I still see room for a further adjustment in the near term to the target range for the federal funds rate to move the stance of policy closer to the range of neutral, thereby maintaining the balance between the achievement of our two goals," Williams Said.

- Treasuries held moderate gains after the S&P Global PMIs data were on balance stronger than expected in the flash November release, led by services increasing slightly whilst manufacturing fell a little more than expected. Overall activity saw the largest rise in new business seen so far this year whilst selling prices reaccelerated on the back of one of the fastest rates of input cost inflation in the past three years.

- Currently, TYZ5 trades +12 at 113-08 vs. -14 high, a bullish development and suggests scope for a climb towards 113-18+, the Oct 28 high. Note that the move high also cancels a recent short-term bearish theme. Key support to watch is 112-06, the Sep 25 low. Trendline support, drawn from the May 22 low, lies at 112-08.

- Stocks are extending highs late Friday - apparently reacting to headlines that the the WH is "internally floating" sales of high-end Nvidia H200 chips to China - that are currently embargoed by the Trump admin to make it more difficult to further develop AI.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.91% (+0.00), volume: $3.170T

- Broad General Collateral Rate (BGCR): 3.86% (-0.01), volume: $1.276T

- Tri-Party General Collateral Rate (TCR): 3.86% (-0.01), volume: $1.253T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.88% (+0.00), volume: $75B

- Daily Overnight Bank Funding Rate: 3.88% (+0.00), volume: $179B

FED Reverse Repo Operation

RRP usage slips to $2.503B with 12 counterparties this afternoon from $6.520B Thursday. Compares to Tuesday's $0.905B - lowest level since mid-March 2021; this years highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Heavy SOFR & Treasury option volumes leaning towards upside calls - looking to hedge rate cut risk in early 2026. Underlying futures firm after the bell - off this morning's knee-jerk lows. Projected rate cut pricing gathered momentum after NY Fed Williams dovish comment, current levels vs. early morning (*): Dec'25 at -17bp (-9.3bp), Jan'26 at -26.1bp (-23.6bp), Mar'26 at -34.5bp (-35.1bp), Apr'26 at -44.1bp (-44.1bp).

SOFR Options:

+18,000 SFRZ5 96.18/96.25/96.31 put flys, 1.0 ref 96.235

-3,000 SFRH6 96.50 straddles, 28.5 ref 96.465

+7,500 SFRZ5 96.12 puts, 1.25 vs. 96.245/0.18%

+5,000 SFRZ5 96.12/96.25 call spds, 8.5

Blocks, total 13,000 SFRZ5 96.37/96.37 call spds, .25

-4,000 SFRZ5 96.06/96.18/96.31 put flys, 1.75

10,000 SFRZ5 96.12/96.25 2x1 risk reversals, 1.5-1.75 (-2x puts)

+10,000 SFRZ5 96.31/96.37 call spds, 0.75 ref 96.245

+5,000 SFRF6 96.37/96.50/96.62 call flys, 2.25 ref 96.465

+4,000 SFRZ5 96.25/96.31 call spds, 3.25

Block, 4,000 SFRZ5 96.25/96.31 put spds 3.0

4,000 SFRZ5 95.93/96.06/96.18 put flys

Block/screen, 15,000 SFRH6 96.12/96.37/96.50/96.62 put condors, 0.75

over 30,000 SFRZ5 96.18/96.25/96.31 call flys

Block, 5,000 SFRM6 96.50/97.00/97.50 call flys, 11.0 vs. 96.715/0.16%

4,000 0QF6 96.87/97.00/97.12/97.25 call condors ref 97.005

6,000 SFRZ5 96.43/96.50 call spds ref 96.195

4,500 SFRZ5 96.37/96.43/96.50 call flys ref 96.1775

2,000 SFRZ5 97.00/97.25 call spds ref 96.96

Treasury Options:

Block, 10,000 TUF6 104.37/104.5 strangles, 21.5

+10,000 TYF6 113 straddles, 127-128 ref 113-05.5

-15,000 TYH6 115 calls, 36 vs. 113-06.5/0.30%

+20,000 TYF5 112/112.5 put spds, 10

over 4,000 TYG6 113/113.5 strangles 149 ref 113-09

over 7,500 Fri wk1 TY 113.25 calls ref 113-00

over 15,600 Mon wkly TY 113.25 calls ref 113-00 to 112-30.5

5,000 TYH6 109/110.5 put spds ref 113-04.5

3,900 TYH6 116.5 calls ref 113-03.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Bull Steepening Week Ends With Bull Flattening

European curves bull flattened to end the week.

- Bunds and Gilts hit session highs in morning trade, as equities continued to lose ground overnight, fueling a safe haven bid.

- Adding to the bullish impetus for Gilts was soft UK services PMI data, though retail sales and public sector borrowing data had little impact.

- Gains faded toward the cash close, however, with equities finding a footing and oil prices ticking higher.

- For the week, the UK curve bull steepened partly on the back of softer-than-expected data (2Y yield -7.0bp, 10Y -2.8bp), with the German curve doing likewise but to a much lesser extent (2Y -2.2bp, 10Y -1.7bp).

- Periphery/semi-core EGB spreads were little changed on the day.

- Attention after hours will be on Moody's potential reviews of Italy and the UK, and Scope on Spain.

- Focus for next week will be on the UK Budget (MNI Preview here), while we also get country-level flash November inflation data from Germany, France, Italy and Spain.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 0.5bps at 2.014%, 5-Yr is down 0.9bps at 2.286%, 10-Yr is down 1.3bps at 2.703%, and 30-Yr is down 1bps at 3.339%.

- UK: The 2-Yr yield is down 1.7bps at 3.776%, 5-Yr is down 2.9bps at 3.961%, 10-Yr is down 4bps at 4.546%, and 30-Yr is down 5.8bps at 5.365%.

- Italian BTP spread down 0.1bps at 75.6bps / Spanish down 0.3bps at 50.6bps

MNI OPTIONS: Large Upside Carries Through End-Week

Friday's Europe rates/bond options flow included:

- DUF6 107.30/107.40cs, bought for 1.25 in 16k Total

- RXG6 128.00/127.00/126.00/124.00 broken p condor, bought for 14 in 2k.

- ERZ6 98.50 calls bought for 5.5 in 20k

- SFIM6 96.80/97.00cs, bought for 4 in 11.5k

MNI FOREX: Dovish Williams Stabilises Risk, USD Index Consolidates Weekly Advance

- The FX session has been characterised by the Japanese yen rising on Friday, halting an impressive run of weakness that has seen it fall around 6% against the dollar since the Japanese election.

- Today’s USDJPY weakness may have initially been driven by the pair finally succumbing to the broader risk sentiment, with like profit taking dynamics assisting the correction ahead of the weekend. Spot currently resides at 156.50, roughly 130 pips from Thursday’s cycle high at 157.89.

- Given the consistent verbal jawboning in recent weeks, we would expect similar FX rhetoric from MOF officials to continue given the rapid extension lower for the Yen this week. BOJ Governor Ueda’s speech on Dec 1 will be crucial for determining the probability of a rate hike in December.

- Elsewhere, the USD index remains at elevated levels, consolidating close to today’s recovery highs of 100.40. A break above 100.48 (May 29 high) would be a broader bullish development for the dollar. Fed’s Williams appeared to put the top in as he placed a dovish lens over the last monetary policy meeting of the year, however, greenback resilience has been a constant theme this week, with the DXY rising 1%.

- Amid the greenback strength, there has been mixed performance across G10, with the Euro relatively underperforming, while the late bounce for stocks has buoyed the likes of AUD, NZD and GBP.

- For GBPUSD, spot has rallied back to 1.31, leaving the pair around 90 pips above the cycle lows ahead of next week’s UK budget. Sterling still spears vulnerable, with bearish technical conditions intact. Below 1.30, market participants will look to 1.2945 (50.0% retracement of the Jan 13 - Jul 1 bull leg), before the more notable lows from April, at 1.2709.

MNI OPTIONS: Expiries for Nov24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1520(E630mln), $1.1550(E565mln)

- USD/JPY: Y155.00($1.1bln)

- AUD/USD: $0.6535(A$1.7bln)

MNI US STOCKS: Late Equities Roundup: Extending Late Session Highs, Tech Redemption?

- Stocks are extending highs late Friday - apparently reacting to headlines that the the WH is "internally floating" sales of high-end Nvidia H200 chips to China - that are currently embargoed by the Trump admin to make it more difficult to further develop AI.

- Sentiment had already improved earlier after dovish comments from NY Fed Pres Williams: still sees potential for a "near term rate cut" as the DJIA and SPX eminis off this week's 5 week lows, the Nasdaq off 10 week lows. Currently, the DJIA trades up 763.7 points (1.67%) at 46520.16, S&P E-Minis up 108.25 points (1.65%) at 6666.25, Nasdaq up 399.9 points (1.8%) at 22480.24.

- Materials, Health Care and Communication Services sector shares continued to lead advances late Friday: Align Technology +7.41%, Cooper Cos +6.64%, Dow +6.18%, International Paper +5.79%, Interpublic Group +4.89% and Omnicom Group +4.74%.

- However, Technology shares climbed off session lows on the chip sales headline - lending to the lat esession rally: Gartner +6.78%, HP Inc +6.72%, Intuit +5.87%, Zebra Technologies +5.82%, Cognizant Technology +5.79%, Accenture +5.37% and ON Semiconductor +5.24%.

- Meanwhile, Utilities and Energy sector shares underperformed, partially tied to weaker oil prices in late trade (WTI -1.08 at 57.83): Vistra Corp -2.80%, Constellation Energy -2.04%, NextEra Energy -1.60% and Halliburton -0.27%.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Pierces Key Support

- RES 4: 6953.75 High Oct 30 and bull trigger

- RES 3: 6900.50 High Nov 12

- RES 2: 6747.78/6791.25 20-day EMA / High Nov 20

- RES 1: 6655.50 Low Nov 7

- PRICE: 6580.25 @ 14:30 GMT Nov 21

- SUP 1: 6540.25/6525.00 Low Oct 10 and a key support / Intraday low

- SUP 2: 6500.00 Round number support

- SUP 3: 6476.62 23.6% retracement of the Apr 7 - Oct 30 uptrend

- SUP 4: 6427.00 Low Sep 2

S&P E-Minis remain in a short-term bear-mode condition and a steep sell-off yesterday reinforces current conditions. The breach of 6655.70, the Nov 7 low cancels recent bullish signals and signals scope for an extension of the corrective cycle. Sights are on 6540.25 (pierced), the Oct 10 low and a key support. A break would open 6476.62, a Fibonacci retracement point. Initial firm resistance to watch is 6747.78, the 20-day EMA.

COMMODITIES

MNI AMERICAS OIL: US OIL: November 21 - Americas End of Day Oil Summary: Crude Lower

WTI crude is down on the day and set for a 3.5% loss on the week over talk of a potential 28-point peace plan the US is trying to push forward on. Some of the losses were moderated after Bloomberg headlines that Ukraine and European allies reject key parts of US plan.

- The US push for a Russia-Ukraine peace deal is offsetting uncertainty over any supply disruptions caused by the start of the sanctions on Russian producers Rosneft and Lukoil.

- Zelenskiy said [regarding the 28-point peace plan] “this is one of the most difficult moments in our history. Ukraine faces a crucial decision: lose its dignity or risk losing a key partner." Says he will not betray Ukraine's national interest.

- Trump also said he would not pull off Russia oil sanctions. There was no anticipation a reversal was ever in play at this point.

- WTI Jan futures were down 1.6% at $58.06

- WTI Feb futures were down 1.5% at $57.81

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 24/11/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 24/11/2025 | 1100/1200 | ECB Cipollone Presentation at Cassa Depositi e Prestiti | ||

| 24/11/2025 | 1245/1345 | ECB Elderson Keynote on Climate & Supervision | ||

| 24/11/2025 | 1330/0830 | * | Quarterly financial statistics for enterprises | |

| 24/11/2025 | 1400/1500 | ** | BNB Business Confidence | |

| 24/11/2025 | 1445/1545 | ECB Lagarde Keynote on AI & Education | ||

| 24/11/2025 | 1530/1030 | ** | Dallas Fed manufacturing survey | |

| 24/11/2025 | 1630/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 24/11/2025 | 1630/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 24/11/2025 | 1800/1300 | * | US Treasury Auction Result for 2 Year Note |