MNI ASIA MARKETS ANALYSIS: Doubts Grow Over December Fed Cut

MNI (NEW YORK) -

HIGHLIGHTS:

- Treasuries Weaken As Doubts Grow Over Next Fed Cut

- USD Slide Continues, Further De-linking FX with Rates & Equities

- Precious Metals Pull Back, Crude Edges Higher

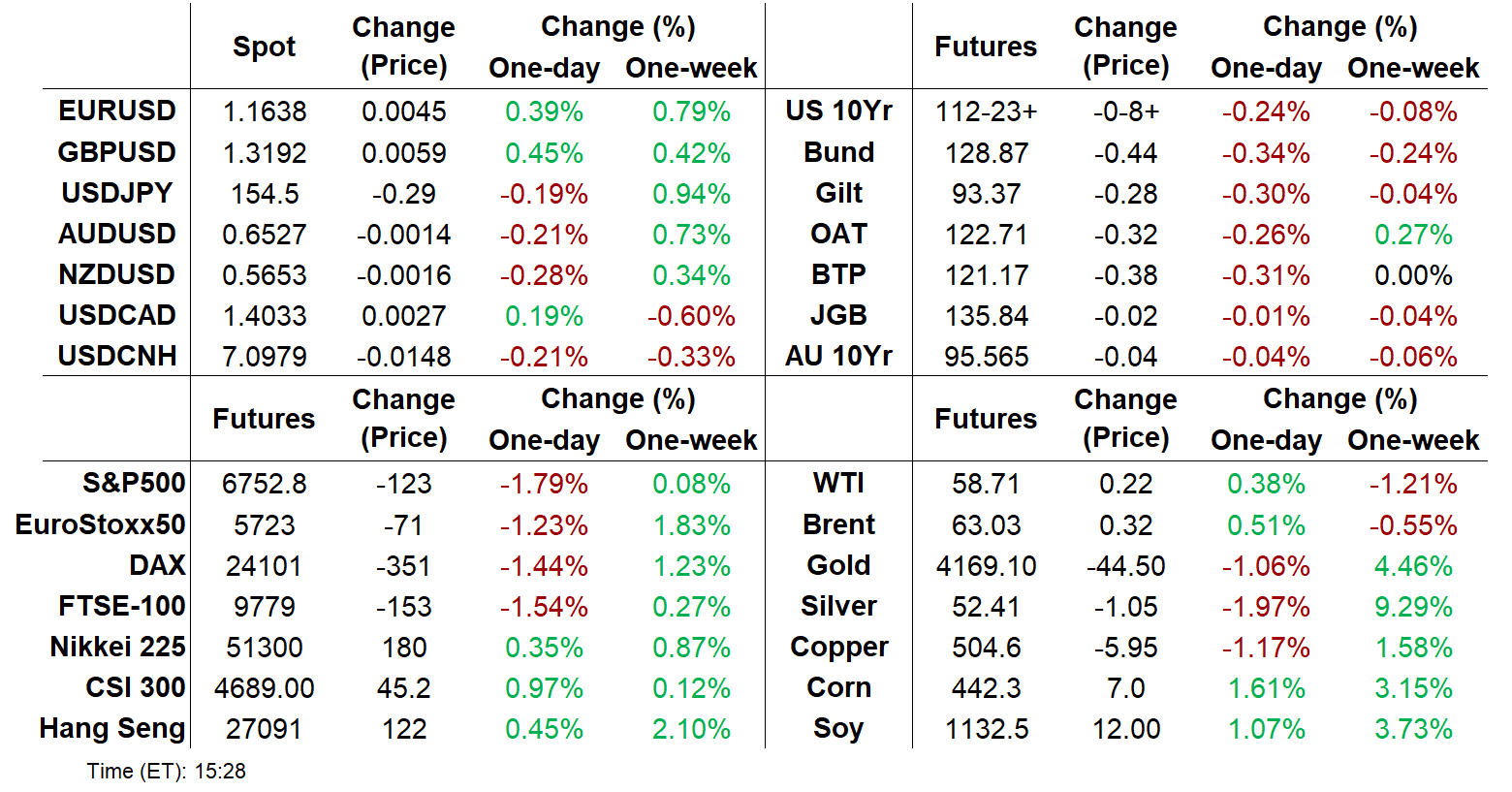

US TSYS: Treasuries Weaken As Doubts Grow Over Next Fed Cut

Renewed skepticism over prospects of a Fed cut in December and a weak long-end auction saw the Treasury curve bear steepen Thursday.

- 2025 FOMC voter and Boston Fed President Collins's commentary late Wednesday that she preferred a rate hold in December wasn't entirely a surprise given her previous statements, but combined with other hawkish views among current voters since the October meeting, there now looks to be an increasingly sizable and vocal minority calling for a hold.

- In keeping with this theme, Fed commentary Thursday skewed neutral-to-hawkish: SF's Daly and Minneapolis's Kashkari, who are two of the 19 FOMC members among the most likely to support a December rate cut, were non-committal on the prospect Thursday; meanwhile Cleveland's Hammack and St Louis's Musalem (also a 2025 voter) continued to portray a patient stance.

- Overall, prospects for a Dec cut were pared to 50/50 vs closer to 65% before Collins's appearance.

- But the curve leaned bear steeper on the day, in part because another weak 30Y Bond auction (4th tail in the last 5 sales) followed on from Wednesday's 10Y tail, pushing long-end yields to session highs. As we write, the 30Y yield is set for its joint-highest close since October 9.

- Latest cash levels: The 2-Yr yield is up 2.3bps at 3.5909%, 5-Yr is up 3.7bps at 3.7082%, 10-Yr is up 4.4bps at 4.1134%, and 30-Yr is up 4.1bps at 4.7054%. Dec 10-Yr futures (TY) down 8.5/32 at 112-23.5 (L: 112-22 / H: 113-01.5)

- The above largely overshadowed the lack of developments on the data front after Wednesday night's conclusion to the government shutdown. Indeed the likely lack of new CPI and up-to-date labor market reports before the December 10 FOMC decision implies that it will be even more difficult to shift hawks' inertia.

- There had been some anticipation that we would get a schedule Thursday for shutdown-postponed data releases from the BLS, but Yahoo Finance cited the Labor Department in saying an updated schedule would be out "in the coming days" while September's nonfarm payrolls report would likely be out next week.

- Even if we have to wait until Friday or later to get an update on data releases, we're still expected to get state-level weekly jobless claims data after the close (and analyst estimates of national-level claims). Friday's calendar is largely Fed-speak related (Schmid, Logan, and Bostic make appearances) with PPI and Retail Sales almost certain to be postponed.

US DATA: The Great U.S. Federal Data Re-Opening Of 2025: Data Primer

This note offers a succinct summary of major monthly economic release methodologies, supporting MNI's previously published guide to the potential rescheduling of data releases with the government now re-opened.

https://media.marketnews.com/Shutdown_Restart_Guide_Nov2025_data_cheat_sheet_b4bebe89ad.pdf

SOFR FIXES AND PRIOR SESSION REFERENCE RATES

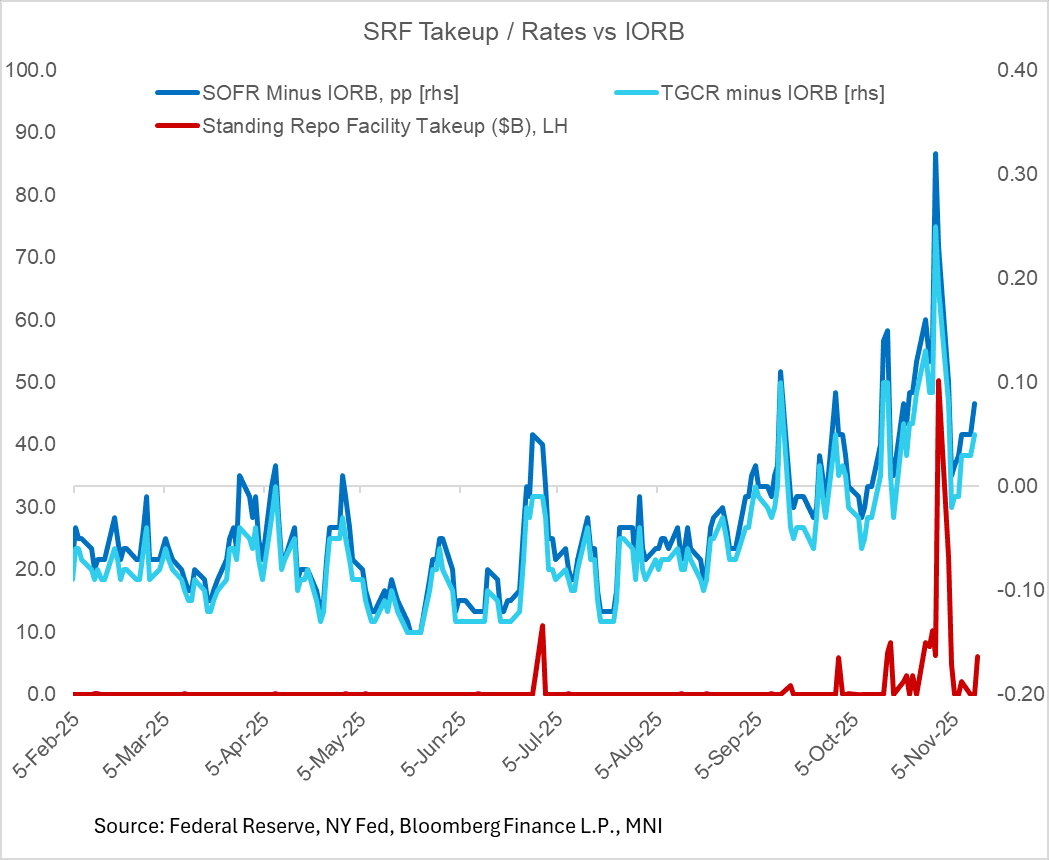

US TSYS/OVERNIGHT REPO: Secured Rates Remain Elevated, Little Relief Imminent

As anticipated, funding market rates remained firm Wednesday, in part due to Treasury bill settlements though overall suggestive of reserve conditions closer to "ample" than "abundant".

- SOFR picked up 3bp Wednesday (3.98%) with TGCR up 2bp (3.95%) with both remaining above the Fed's IORB rate (3.90%), while there was also continued takeup of the Fed's standing repo facility in this morning's operation ($3.9B, after $6.1B total Wednesday).

- After raising $14B in net cash Wednesday through bill settlements, Treasury raises $23B Thursday which is expected to keep rates underpinned.

- There might be some subsiding Friday, but Monday sees another $27B in coupon settlements before GSE cash is expected to come into market from next Tuesday to apply some downside pressure on rates (offsetting $14B in bill settlements on Tuesday).

- However, there was no change in effective Fed funds (3.87%).

REPO REFERENCE RATES (rate, change from prev. day, volume):

* Secured Overnight Financing Rate (SOFR): 3.98%, 0.03%, $3209B

* Broad General Collateral Rate (BGCR): 3.95%, 0.02%, $1263B

* Tri-Party General Collateral Rate (TGCR): 3.95%, 0.02%, $1231B

New York Fed EFFR for prior session (rate, chg from prev day):

* Daily Effective Fed Funds Rate: 3.87%, no change, volume: $77B

* Daily Overnight Bank Funding Rate: 3.87%, no change, volume: $156B

US 10YR FUTURE TECHS: (Z5) Fades Off Resistance

- RES 4: 114-02 High Oct 17 and the bull trigger

- RES 3: 113-29 High Oct 22

- RES 2: 113-18+ High Oct 28

- RES 1: 113-02+ High Nov 5, 7 & 12 and a key near-term resistance

- PRICE: 112-24+ @ 17:10 GMT Nov 13

- SUP 1: 112-09+ Low Nov 5 and the 100-dma

- SUP 2: 112-06 Low Sep 25 and a reversal trigger

- SUP 3: 112-03+ Trendline support drawn from the May 22 low

- SUP 4: 111-23 50.0% retracement of the May 22 - Oct 17 bull leg

Treasuries have faded off the weekly high, returning to midpoint of the week’s range. Resistance holds at 113-02. This level has been pierced, a clear move above it would be a bullish signal and shift focus to the next notable resistance at 113-18+ and above. This would also cancel a short-term bear theme. On the downside, a resumption of weakness would instead open 112-09+, the 100-DMA and 112-06, the Sep 25 low. Trendline support lies at 112-03+.

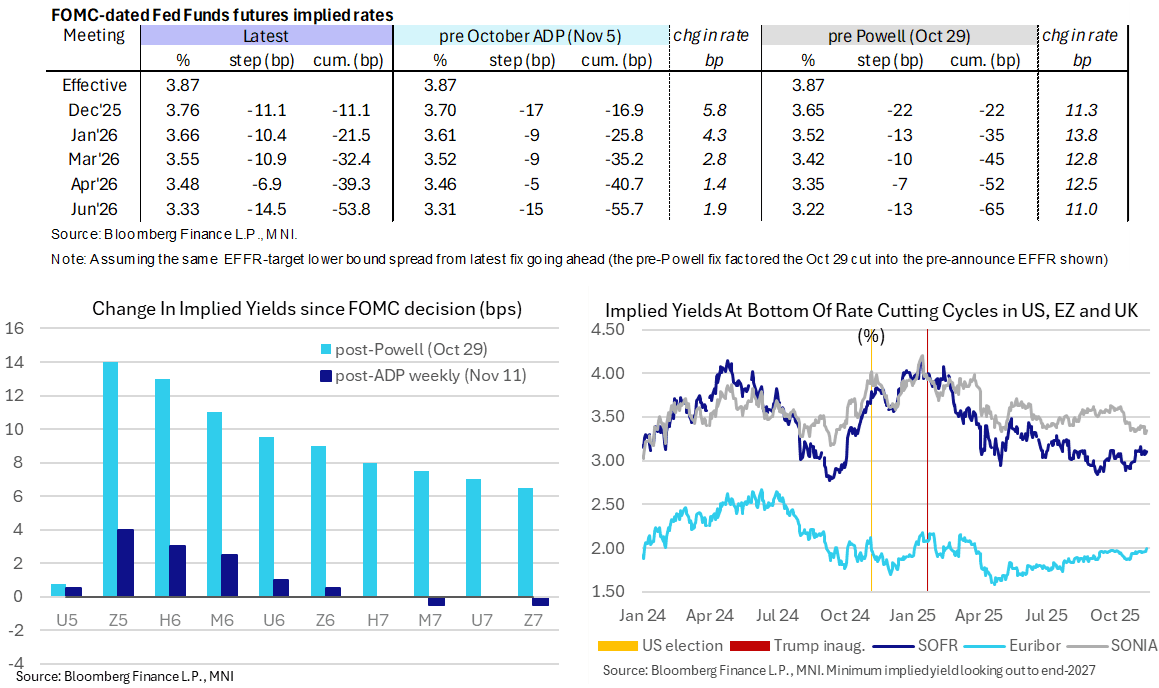

STIR: Heavy Front End Volumes Persist On Fed Dec Pause Prospects

- US rates have seen a sizeable hawkish shift today with greater interest in the December FOMC meeting being a 50/50 call between another 25bp cut or a hold.

- Moves extended a sell-off seen late yesterday, with the best headline culprit at the time being Collins (a ’25 voter) favoring holding rates steady in her first post-FOMC remarks despite having hinted at such prior to the meeting. A general positioning unwind with the government re-opened could also be at play.

- SFRZ5 has seen particularly strong volumes today, with 580k currently about 1.8x the recent average for the time of day. It sees the largest losses on the day, -0.04, for back to earlier lows seen early in the session as US desks filtered in before stabilizing.

- Fed Funds implied rates have continued their hawkish shift however, now pricing 11bp of cuts for next month’s meeting from an assumed 3.87% effective.

- Cumulative cuts: 11bp Dec, 21.5bp Jan, 32.5bp Mar, 39.5bp Apr and 54bp Jun.

- Reverting to SOFR futures, the terminal yield of 3.10% (SFRH7, +1.5bp) has actually softened slightly through US trading. It’s still +4.5bp from Tuesday’s close having digested the soft weekly ADP print but still off the multi-month high close of 3.16% from last Wednesday after more encouraging monthly ADP and especially ISM Services data.

- Still to come today, state-level jobless claims data at ~1700ET in lieu of today's national-level release that wasn't able to be published at 0830ET coming so soon after the government re-opened.

US Options Roundup - 13 Nov 2025

Thursday's U.S. rates/bond options flow included:

- TY Week 2 112.25p, sold at '01 in 15k (weekly)

- TYZ5 113/112.75/112.50/112p condor, bought for 1 in 25k

- SFRZ5 96.37c, traded 1.5 in 20k.

- SFRZ5 96.37/96.43cs, traded 0.5 in 5k.

- SFRZ5 96.31c, traded 2.5 in 2k.

- SFRZ5 96.31/96.37cs 1x2, traded flat in 5k.

- SFRZ5 96.12/96.31RR, traded flat in 5k.

- SFRZ5 96.18/96.25/96.31/96.37c condor, traded 1.5 & 1.75 in 2.5k.

- SFRZ5 96.18/96.25/96.31/96.43c condor, traded 1.25 in 2.5k.

- SFRZ5 9618/96.06ps, traded for 5.75 in 4k.

- SFRZ5 96.18p, traded 6.75 in 3k.

- SFRZ5 95.93p, traded 0.25 in 3k.

- SFRZ5 96.12/96.00ps 2x3, sold at 4.75 in 6k

- SFRZ5 96.31c sold at 2.5 in 10k and earlier 2.75 in 10k (20k Total)

- SFRZ5 96.37/96.50cs vs 96.12p, bought the put for 10k.

- SFRZ5 96.56/96.37/96.18p fly, sold on screen at 6 in 6.5k

- SFRH6 96.00/97.00^^, sold at 4.25 in 4k.

- SFRF6 96.50/96.62/96.87c fly traded 2 in 11k.

- SFRH6 96.12/96.06ps 1x2, traded flat in 8k.

- SFRH6 96.18/96.12/96.06p ladder, traded 0.5 in 4k.

- SFRH6 96.43/96.37/96.31p ladder, traded 1.25 in 2k.

- SFRZ6 99.00/100.00/101.00c fly, traded 1.5 in 5k.

- 0QZ5 97.00/96.68ps 1x2, traded flat in 4k.

- 0QZ5 96.62/97.18 with 2QZ5 96.50/97.06 strangle strip, sold at 8.5 in 4k

- 2QH6 96.75 straddle, bought for 39 in 5k total

BONDS: EGBs-GILTS CASH CLOSE: Bear Steeper As US Government Re-Opens

European curves bear steepened Thursday.

- After a modest uptick in early trade, US Treasuries led a global rise in yields following Federal Reserve commentary late Wednesday that cast doubt on a December rate cut, as well as confirmation that the federal government would re-open Thursday.

- That US-led weakness, which started in the late European morning, continued in orderly fashion throughout the rest of the cash session.

- Both the UK and German curves bear steepened on the day, failing to benefit from any kind of safe-haven bid as equities pulled back - with Bunds underperforming Gilts at the long end.

- Periphery/semi-core EGB spreads traded mixed but overall instruments were flat to Bunds.

- UK Q3 preliminary GDP came in slightly softer-than-expected (0.1% Q/Q vs 0.2% cons, 0.3%% prior) but the data was "noisy" and it had little apparent impact on BOE cut pricing.

- Eurozone August industrial production was likewise softer than expected with typical noise in the data (Ireland-related).

- Friday data includes some Eurozone data (second reading of Q3 GDP along with prelim Q3 employment), as well as final October inflation readings (France, Spain). There's also commentary scheduled from ECB's Lane, Ecriva, and Vujcic.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 3bps at 2.028%, 5-Yr is up 4.6bps at 2.293%, 10-Yr is up 4.5bps at 2.688%, and 30-Yr is up 5.2bps at 3.28%.

- UK: The 2-Yr yield is up 3.6bps at 3.764%, 5-Yr is up 3.4bps at 3.901%, 10-Yr is up 3.9bps at 4.437%, and 30-Yr is up 4bps at 5.231%.

- Italian BTP spread up 0.3bps at 73.1bps / French OAT down 0.5bps at 73.1bps

EUROPE OPTIONS: Call Structure Activity Remains Predominant In European Rates

Thursday's Europe rates/bond options flow included:

- ERH6 97.75/9800ps, bought for 6 in 10k

- ERM6 98.06/98.18/98.43/98.56c condor, bought for 2.75 in 4k

- ERM6 98.25/98.50cs, bought for 2.5 in 3k

- 0RM6 98.00/98.25cs, bought for 6 in 20k

- SFIM6 96.70/96.85/96.90/97.05 thin body call condor paper paid 2.75 on 6K

- SFIM6 96.55/96.70 call spread vs. 96.50/96.30 put spread paper paid 1.0 on 4K.

- SFIM6 96.85/97.00cs, bought for 3 in 5k

FOREX: USD Slide Continues, Further De-linking FX with Rates & Equities

- As the US government reopened, the USD fell against broader G10, prompting a new November low for the USD Index. In further evidence that the currency and rates markets are diverging, the USD found very little solace in either the strength and show above 4.11% in the US 10y yield, or the persistent trimming of Fed rate cut pricing for the December FOMC, which now stands at less than 50%.

- The USD is slipping as markets seem to be adopting a pro-growth phase after the end of the government shutdown, which was estimated to be costing as much as $15bln per day - however the test for the USD's ability to sustain itself at lower levels will be tested by the incoming data. This covers not only the official agency releases, but the private sector data also, including next week's ADP weekly jobless estimate.

- That said, a negative session for equities paints a less positive picture. Underperformance in megacap tech names (NVIDIA dropped near 3.5%) undermined headline index performance, which dragged AUD, NZD and other growth proxy currencies off highs, while favouring haven FX including JPY and CHF.

- Meanwhile, Gold saw renewed gains early Thursday, putting prices at the highest since the October 21 pullback. While prices have faded, a positive close today would be the 7th consecutive higher daily close. Only partial pricing for a Dec Fed cut opens up potential for a dovish turn in rates should incoming data surprise to the downside, which should prove positive for gold prices.

- Focus Friday shifts to the potential publication of advisories and schedules for the still-missing US economic releases. With the government still in the process of reopening, we expect September NFP to be released imminently, and in it's full format, however the October release that follows may be lacking key data on the unemployment rate - a message affirmed by White House Advisor Kevin Hassett today.

- Chinese retail sales and industrial production data are due Friday, with speeches also due from ECB's Escriva, Vujcic, Elderson & Lane, while Fed's Schmid, Logan & Bostic (who announced his retirement this week) round things off in the US.

FX OPTIONS: Larger FX Option Pipeline

- EUR/USD: Nov17 $1.2100(E1.4bln); Nov19 $1.1800(E1.5bln)

COMMODITIES: Precious Metals Pull Back, Crude Edges Higher

- Crude has reversed some of yesterday’s steep declines driven by oversupply concerns after OPEC shifted their balance for Q3 to a surplus. The IEA revised up its forecast for a surplus in the oil markets in its latest monthly report.

- WTI Dec 25 is up by 0.4% at $58.7/bbl.

- From a technical perspective, yesterday’s sell-off in WTI futures strengthens a bearish theme. A continuation lower would pave the way for a move towards key support and the bear trigger at $55.96, the Oct 20 low.

- Resistance to watch is $62.59, the Oct 24 high.

- Meanwhile, precious metals have fallen to session lows in recent trade, with spot gold currently down by 0.7% at $4,166/oz and silver 1.3% lower at $52.5/oz.

- Despite the move lower in gold, the fact that a December Fed cut is only partially priced leaves potential for a dovish turn in rates should incoming US data surprise to the downside, which should prove positive for gold prices.

- The downleg in gold since Oct 20 appears to have been a correction and the move down has allowed an overbought condition to unwind. Previous gains this week suggest that correction is over, with key support at the 50-day EMA, at $3,920.6, intact.

- Initial resistance is $4,264.7, a Fibonacci retracement.

- For silver, trend signals remain bullish, with price still near key resistance and the bull trigger at $54.480, the Oct 17 high.

- Initial support is at the 20-day EMA at $49.207.

| Date | GMT/Local | Impact | Country | Event |

| 14/11/2025 | 0001/0001 | KPMG/REC Report on Jobs | ||

| 14/11/2025 | 0200/1000 | *** | Fixed-Asset Investment | |

| 14/11/2025 | 0200/1000 | *** | Retail Sales | |

| 14/11/2025 | 0200/1000 | *** | Industrial Output | |

| 14/11/2025 | 0200/1000 | ** | Surveyed Unemployment Rate M/M | |

| 14/11/2025 | 0700/0800 | ** | Unemployment | |

| 14/11/2025 | 0745/0845 | *** | HICP (f) | |

| 14/11/2025 | 0800/0900 | *** | HICP (f) | |

| 14/11/2025 | 0900/1000 | Foreign Trade | ||

| 14/11/2025 | 1000/1100 | * | Trade Balance | |

| 14/11/2025 | 1000/1100 | *** | EZ GDP 2nd (Flash) | |

| 14/11/2025 | 1030/1130 | ECB Elderson Keynote at ECB Banking Supervision Forum | ||

| 14/11/2025 | 1330/0830 | ** | Monthly Survey of Manufacturing | |

| 14/11/2025 | 1330/0830 | ** | Wholesale Trade | |

| 14/11/2025 | 1330/0830 | *** | Retail Sales | |

| 14/11/2025 | 1330/0830 | *** | PPI | |

| 14/11/2025 | 1330/1430 | ECB Elderson Remarks at COP30 Finance Day | ||

| 14/11/2025 | 1500/1000 | * | Business Inventories | |

| 14/11/2025 | 1500/1600 | ECB Lane Panel at Workshop on International Macroeconomics and Finance | ||

| 14/11/2025 | 1530/1030 | ** | Natural Gas Stocks | |

| 14/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 14/11/2025 | 1930/1430 | Dallas Fed's Lorie Logan | ||

| 14/11/2025 | 2020/1520 | Atlanta Fed's Raphael Bostic |