MNI ASIA MARKETS ANALYSIS: Crude Up as Geo-Pol Risks Persist

HIGHLIGHTS

- Treasuries look to finish mixed Friday - well off early session lows as crude prices rebounded - as negotiations over safe transit through the Hormuz Straight gave way to threats of more attacks on Iran by the US.

- The Wall Street Journal reports that the US military is "moving a Marine expeditionary unit to the Middle East, as Iran steps up its attacks on the Strait of Hormuz..."

- WSJ's @NickTimiraos writes on X.com: "A federal judge threw out a pair of subpoenas the Justice Department issued to the Federal Reserve, handing a victory to the Fed and dealing a heavy blow U.S. Attorney Jeanine Pirro's criminal investigation into Chair Jerome Powell."

- Job openings bounced back more strongly than expected in the January JOLTS report to correct for what was at the time a surprisingly low December reading, better aligning with steadier Indeed job postings.

US TSYS

MNI US TSYS: Tsys Hug Lows/Stable as Crude Rebounds on Continued Geo-Pol Risk

- Treasuries look to finish mixed Friday, curves twisting steeper with the short end outperforming: 2s10s +3.535 at 54.934.

- Rates unwound early support as crude prices see-sawed off lows (WTI just over $98.0/bbl), Treasuries taking the risk metric in stride - holding off midday lows: TYM6 trades currently +1 at 111-14 vs. -11 low, with sights are on the next key support at 111-06+, the Jan 20 low. Clearance of this level would highlight an important medium-term bearish development.

- Treasuries helding moderate gains after flurry of data: GDP annualized QoQ lower than expected as are durable goods orders, other metrics largely in-line. Markets reacting positively to latest headline re: France & Italy talking to Iran re: safe passage through Hormuz Straight, this after India tanker made safe passage earlier.

- UofM sentiment better than expected while 1Y inflation expectations holds steady to prior (lower than estimate), 5-10Y inflation exp dips slightly. JOLTS job openings surge higher, quits level declines but slightly higher than expected. Layoffs retreated.

- Job openings jumped back to 6.946mln in Jan (sa, cons 6.75mln) to fully reverse the drop to 6.55mln in Dec (hardly revised from what was a surprisingly low 6.54mln originally) from 6.93mln in Nov.

- Late headline: The Wall Street Journal reports that the US military is "moving a Marine expeditionary unit to the Middle East, as Iran steps up its attacks on the Strait of Hormuz..."

- Look ahead to Monday's Data Calendar: Empire Mfg, IP/Cap-U, NAHD Housing Mkt Index.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.65% (+0.01), volume: $3.112T

- Broad General Collateral Rate (BGCR): 3.63% (+0.01), volume: $1.316T

- Tri-Party General Collateral Rate (TCR): 3.63% (+0.01), volume: $1.287T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.64% (+0.00), volume: $99B

- Daily Overnight Bank Funding Rate: 3.64% (+0.00), volume: $186B

FED Reverse Repo Operation

RRP usage inches up to $0.427B with 4 counterparties this afternoon vs. $0.137B Thursday. Compares to last year's highest excess liquidity measure: $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Heavy SOFR/Treasury options centered around downside puts Friday. Underlying futures running mixed after the bell, well off early session highs as crude prices rebound amid ongoing Middle-East tensions and threats of new strikes on Iran by Pre Trump. Nevertheless, projected rate cut pricing firms slightly vs. late Thursday lvls (*): Mar'26 at -.2bp, Apr'26 -1.2bp, Jun'26 at -5.9bp (-5.6bp), Jul'26 at -10.2bp (-9.2bp), Sep'26 at -13.7bp (-12.7bp). The first 25bp rate cut has all the way out to June 2027.

SOFR Options:

Block/screen over 130,000 2QM6 96.00 puts 6.0 vs. 96.61/0.18%

+10,000 SFRM6 95.75/96.00 put spds, 1.5 ref 96.375

+6,500 0QK6 96.56 straddles, 47.0-48.0 ref 96.565

over 12,000 SFRZ6 95.81/96.31 put spds ref 96.51

+10,000 SFRU6 99.00 calls, 1.5

4,000 SFRU6 95.87/96.37 put spds ref 96.455

4,000 SFRJ 96.43/96.50 put spds

20,000 SFRZ6 96.12/96.37 put spds ref 96.50

Block, 6,000 0QK6 97.00/97.25 call spds, 4.0 vs. 96.585/0.10%

2,000 SFRK6 96.18 puts, 3.0 ref 96.375

over 15,600 0QH6 96.50 puts, 2.5-4.0 ref 96.51 to -.525

2,500 SFRH6 96.31 puts, 0.5 ref 96.3125

over 9,400 SFRM6 96.43/96.56/96.62/96.81 broken call condors ref 96.37 to -.38

Block, 2,500 SFRJ6 96.43/96.50 put spds, 5.0 ref 96.365

2,000 0QJ6 96.62/96.75/96.87/97.00 call condors ref 96.555

over 9,000 SFRJ6 96.25/96.31/96.37 put flys ref 96.37

3,100 SFRU6 96.31/96.43 put spds ref 96.43

2,000 SFRZ6 96.75/97.00 call spds vs. 95.75/96.00 put spds ref 96.455

2,200 SFRU6 96.93/97.06 call spds ref 96.405

2,000 0QH6 96.37 puts ref 96.515

Treasury Options:

over -58,000 TYK6 108.5 puts, 15

10,800 TYK6 109.5 puts, 25

5,500 TYK6 109.5 puts, 25

6,000 TUM6 104/104.25/104.5/104.75 call condors

over 67,000 TYJ6 112 calls, 20-22 vs. 111-16 to -12.5/0.34%

10,000 TYJ6 114.5 calls, 2 ref 111-22.5 (expires in 2 weeks)

3,000 TYJ6 112.75/113.25 put spds

over +115,000 TYJ6 109.5/113.5 put over risk reversals, 5-6 net db for the put vs. 111-15.5/0.22%

Block, 10,000 TYJ6 111.5 puts, 29

15,000 TYJ6 111.25/111.75 put spds ref 111-17.5

2,500 FVK6 110/111 call spds ref 108-18.75

over 4,000 FVJ6 107.5 puts, 8 ref 108-18.5

over 5,200 TYJ6 113.5 calls, ref 111-15

over 17,900 FVJ6 109 calls, 14 last ref 108-15

5,600 wk2 TY 112 puts, 1 (exp today)

2,000 USJ6 109/112 put spds

over 3,700 FVJ6 109.25 calls, 10 last, ref 108-15.75

over 14,400 TYJ6 111 puts, 26-25 ref 111-13.5 to -15

3,700 TYJ6 111.5 puts, 39 ref 111-15

Block, 20,000 TYJ6 111.25/111.75 put spds, 12 ref 111-18

MNI BONDS: EGBs-GILTS CASH CLOSE: Bear Steepening Seals Another Poor Week

European government bonds sealed another weekly selloff as curves bear steepened Friday.

- Core EGBs and Gilts gained in early trade, with various factors allowing for a relief rally, including soft US macro data and a downtick in energy prices on a report that European countries were negotiating with Iran on opening the Strait of Hormuz to their ships.

- But the last 2 hours of the cash session saw a renewed selloff that brought Bunds and Gilts back to session lows, with periphery spreads widening from intra-day tights.

- Once again of course it was Mideast developments that weighed, with oil prices rebounding late after the Wall Street Journal reported that the US was moving more forces to the region, and Italy reportedly refuting the earlier Europe-Iran negotiations story.

- On the day, the both the UK and German curves lightly bear steepened, with Gilts once again underperforming. For the week there was substantial bear flattening in the UK curve (2Y yield +25bp, 10Y +19bp), while Germany's saw yields rise largely in parallel (2Y and 10Y both +12bp).

- Periphery/semi-core EGB spreads widened, though closed well off earlier wides. There's a potential Fitch ratings review of Italy after markets close Friday.

- Next week's calendar is packed, highlighted by the BOE and ECB decisions.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 2.425%, 5-Yr is up 1.4bps at 2.626%, 10-Yr is up 1.5bps at 2.972%, and 30-Yr is up 1.4bps at 3.532%.

- UK: The 2-Yr yield is up 3.7bps at 4.13%, 5-Yr is up 4.3bps at 4.341%, 10-Yr is up 4.9bps at 4.822%, and 30-Yr is up 4.5bps at 5.495%.

- Italian BTP spread up 2.3bps at 81.3bps / French OAT up 1.7bps at 69.1bps

MNI EGB OPTIONS: Colossal Call Structures In Sonia, Good Size In Bund To Close The Week

Friday's Europe rates/bond options flow included:

- DUJ6 106.20^, bought for 46 in 2.5k

- OEJ6 117/118cs 1x2, sold at 9 and 8 in 12k

- OEJ6 116.75/117.25cs 1x2, bought for 1.5 in 3k

- OEK6 116.5/117.5/118c ladder, bought for 21 and 22 in 6k

- RXK6 126.5/125.5ps, sold at 43.5 in 4k

- RXK6 127/128/129/130c condor, bought for 23.5 in 10k

- ERJ6 97.62/97.50ps trades 3.25 in 21k

- SFIM6 96.40/96.50/96.65/96.75c condor sold at 2.75 down to 2.5 in 65k

- SFIM6 96.40/96.50/96.80/96.90c condor sold at 3 down to 2.75 in 20k

- SFIZ6 96.35/96.50cs vs 96.25/96.10ps, trades 1.25 for the cs in 25k

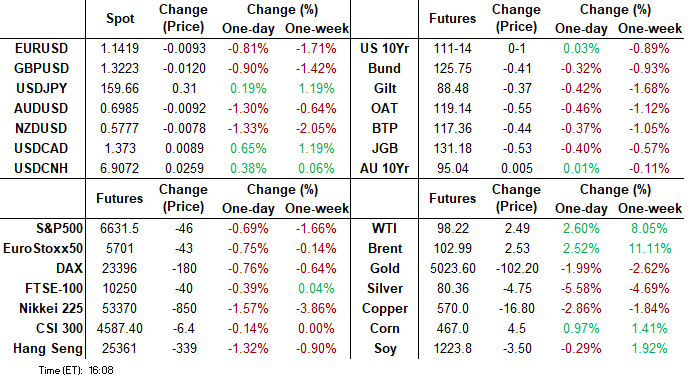

MNI FOREX: USD Index Extends Weekly Rally to 1.4%, Eyes Close Above 100.00

- Despite a volatile session for oil prices, Brent crude futures are ending the week up an impressive 10% this week currently trading above $102/bbl. Today’s firm bounce off the lows has kept the US dollar on the front foot, resulting in the USD index looking set to close ~1.4% in the green, and at the highest level since November last year.

- This has helped EURUSD return to 1.1430 as we approach the close, having firmly broken through an important support cluster between 1.15-1.1470, a notable bearish development for the pair. In similar vein, GBPUSD has made fresh session lows below 1.3250.

- Souring risk sentiment however demotes the likes of AUD and NZD to the bottom of the G10 leaderboard, with AUDUSD notably pressing back below the 0.7000 handle in late trade and extending its pullback from the week’s highs to over 2.5%.

- The Canadian dollar is also softer, and this move could have legs as the additional headwind from the much weaker-than-expected employment report amplifies the price action, and USDCAD is pressuring a significant close above 1.3725 resistance.

- USDJPY has remained on the front foot, printing fresh cycle highs on Friday above 159.50. Finance Minister Katayama’s comments overnight will be negatively impacting the risk/reward profile for longs up here, however, analysts have been flagging that with fundamentals driving the move, and the relatively orderly nature of the rally in recent sessions, this may dissuade the authorities from imminent action.

- Monday’s calendar will be highlighted by Canadian CPI, before the focus turns to several G10 central bank decisions, with the RBA kicking things off on Tuesday.

MNI FX OPTIONS: Expiries for Mar16 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.3bln), $1.1575(E802mln), $1.1600(E1.6bln)

- USD/JPY: Y156.00($1.3bln), Y160.00($796mln)

- EUR/JPY: Y176.50(E510mln)

- GBP/USD: $1.3425(Gbp952mln), $1.3500(Gbp1.1bln)

- AUD/USD: $0.7100(A$1.4bln)

- USD/CAD: C$1.3630-50($1.0bln)

- USD/CNY: Cny6.9250($600mln)

MNI US STOCKS: Stocks Retreating as Crude Prices Extending Highs

- Equities are quietly de-risking at the moment as crude prices have risen to session highs (WTI just over $98.6/bbl): Nasdaq -1%, SPX eminis -.55% while the DJIA slips 0.15% at the moment.

- Information Technology and Communication Services sector shares continue to lead declines, software & services shares weighing on the former with Adobe -5.5% after CEO Shantanu Narayen announced his resignation late Thursday (not to mention paying $150M fine for subscription complaints). Meanwhile, Salesforce, Broadcom and Palantir Technologies, all down 2-4%.

- Media and entertainment shares weighed on Communication Services: Meta -4.35% while TKO Group Holdings, Fox Corp and Live Nation Entertainment trade -2.65-4.15% lower.

- On the positive side, Utilities outperformed with Sempra, WEC Energy Group, Ameren Corp and Edison International +1.95-2.15%. Oil and gas shares are gaining as well with Diamondback Energy, APA and Exxon Mobil +1.5-2.8%.

MNI EQUITY TECHS: E-MINI S&P: (H6) Key Support Remains Exposed

- RES 4: 6983.75 High Feb 25

- RES 3: 6878.09 50-day EMA

- RES 2: 6839.26 20-day EMAl

- RES 1: 6769.50 High Mar 12

- PRICE: 6652.00 @ 1500 ET Mar 13

- SUP 1: 6640.00 Intraday low

- SUP 2: 6583.00 Low Nov 21 ‘25 and a key medium-term support

- SUP 3: 6534.52 1.382 proj of the Feb 25 - Mar 3 - 5 price swing

- SUP 4: 6503.25 1.500 proj of the Feb 25 - Mar 3 - 5 price swing

A sharp bounce in S&P E-Minis on Monday and the reversal from Tuesday’s high highlights the fact that recent gains were most likely corrective. This has allowed a recent oversold trend condition to unwind. A continuation lower would open 6583.00, the Nov 21 ‘25 low and the next key medium-term support. Clearance of this level would strengthen a bearish threat. Initial firm resistance is 6878.09, the 50-day EMA.

COMMODITIES

MNI AMERICAS OIL: US OIL: March 13 - Americas End of Day Oil Summary: Crude Rises

WTI reversed earlier losses and is near $100/bbl amid signs of an intensifying Iran war, and despite uncertainty around potential tanker traversals via the Strait of Hormuz. ULSD futures have also soared through $4/gal due to supply uncertainties with Gulf refineries under fire.

- US Baker Hughes oil rig count up 1 to 412.

- India is in active talks with Iran to allow at least 23 tankers through the Strait of Hormuz with the first crossings expected by the weekend, two Indian government officials told The Wall Street Journal. Two LPG tankers were reportedly granted passage.

- A Turkish-owned ship was allowed to pass through the Strait of Hormuz, Turkey’s transport minister said. It is not currently clear what vessel was allowed to pass through, and the report has not been verified by other outlets.

- The FT reported that Italy and France were in talks with Tehran seeking safe passage for their ships through the Strait of Hormuz. The Italian government later denied the report.

- The mixed messaging from the White House on the potential duration of the conflict remains in evidence. President Trump told Fox News that the US was going to be hitting Iran very hard over the next week.

- WTI Apr futures were up 2.9% at $98.71

- WTI May futures were up 2.4% at $96.63

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 16/03/2026 | 1215/0815 | ** | CMHC Housing Starts | |

| 16/03/2026 | 1230/0830 | *** | CPI | |

| 16/03/2026 | 1230/0830 | * | Household debt-to-income | |

| 16/03/2026 | 1230/0830 | ** | Empire State Manufacturing Survey | |

| 16/03/2026 | 1315/0915 | *** | Industrial Production | |

| 16/03/2026 | 1400/1000 | ** | NAHB Home Builder Index | |

| 16/03/2026 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 16/03/2026 | 1530/1130 | * | US Treasury Auction Result for 13 Week Bill | |

| 17/03/2026 | 0330/1430 | *** | RBA Rate Decision |