BONDS: EGBs-GILTS CASH CLOSE: Bear Steepening Seals Another Poor Week

Mar-13 17:15

European government bonds sealed another weekly selloff as curves bear steepened Friday.

- Core EGBs and Gilts gained in early trade, with various factors allowing for a relief rally, including soft US macro data and a downtick in energy prices on a report that European countries were negotiating with Iran on opening the Strait of Hormuz to their ships.

- But the last 2 hours of the cash session saw a renewed selloff that brought Bunds and Gilts back to session lows, with periphery spreads widening from intra-day tights.

- Once again of course it was Mideast developments that weighed, with oil prices rebounding late after the Wall Street Journal reported that the US was moving more forces to the region, and Italy reportedly refuting the earlier Europe-Iran negotiations story.

- On the day, the both the UK and German curves lightly bear steepened, with Gilts once again underperforming. For the week there was substantial bear flattening in the UK curve (2Y yield +25bp, 10Y +19bp), while Germany's saw yields rise largely in parallel (2Y and 10Y both +12bp).

- Periphery/semi-core EGB spreads widened, though closed well off earlier wides. There's a potential Fitch ratings review of Italy after markets close Friday.

- Next week's calendar is packed, highlighted by the BOE and ECB decisions.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is up 0.7bps at 2.425%, 5-Yr is up 1.4bps at 2.626%, 10-Yr is up 1.5bps at 2.972%, and 30-Yr is up 1.4bps at 3.532%.

- UK: The 2-Yr yield is up 3.7bps at 4.13%, 5-Yr is up 4.3bps at 4.341%, 10-Yr is up 4.9bps at 4.822%, and 30-Yr is up 4.5bps at 5.495%.

- Italian BTP spread up 2.3bps at 81.3bps / French OAT up 1.7bps at 69.1bps

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US STOCKS: Midday Equities Roundup: Off Lows After Volatile First Half

Feb-11 17:11

- After a volatile first half, stocks are see-sawing lower at midday Wednesday, Financials and Communication Services sector shares leading declines.

- While clarity of this morning's delayed employment data was debated, higher than expected job gains for January helped stocks rally on the open. Indexes gapped lower soon after however, sentiment shifted as Bitcoin fell over -4% to 66,021.

- Prices moderated ahead midday, however, the DJIA trading down 16.19 points (-0.03%) at 50035.76, S&P E-Mini Futures up 1.75 points (0.03%) at 6947.25, Nasdaq down 77.5 points (-0.3%) at 22980.96.

- As noted Financials and Communication Services sector shares led declines in the first half, the former tied to Bitcoin weakness: Robinhood Markets -12.20%, Assurant -8.04%, Coinbase Global -6.74% and FactSet Research Systems -5.81%. Omnicom Group -5.37%, Trade Desk Inc -3.09%, Match Group -3.08% and Netflix -2.70% weighed on the Communications sector.

- Meanwhile, Industrials, Materials and Energy sector shares outperformed, the latter as crude prices gained (WTI +1.26 at 65.22).

- Generac Holdings +16.97%, Comfort Systems USA +6.29%, Eaton Corp +5.21%

- Smurfit Westrock +10.12%, DuPont de Nemours +3.88%, LyondellBasell Industries +3.41%

- EOG Resources +3.59%, Devon Energy +3.38%, Exxon Mobil +3.29%.

US 10YR FUTURE TECHS: (H6) Bull Cycle Intact

Feb-11 17:05

- RES 4: 113-04 76.4% retracement of the Nov 25 - Jan 20 bear leg

- RES 3: 112-31 High Dec 18 and key short-term resistance

- RES 2: 112-25 61.8% retracement of the Nov 25 - Jan 20 bear leg

- RES 1: 112-20 Intraday high

- PRICE: 112-12 @ 16:51 GMT Feb 11

- SUP 1: 112-00 20-day EMA

- SUP 2: 111-26 Low Feb 9

- SUP 3: 111-13+ Low Feb 3

- SUP 4: 111-09 Low Jan 20 and the bear trigger

Treasuries are holding on to their latest gains, despite an intraday dip on the back of the stronger-than-expected NFP data. This week’s rally has strengthened the short-term bullish condition. A continuation higher here would pave the way for a move towards 112-25 next, the 61.8% retracement of the Nov 25 - Jan 20 bear leg. Clearance of this price point would open 112-31, the Dec 18 high. Initial support to watch lies at 112-00, the 20-day EMA. A break of this level would highlight a potential reversal.

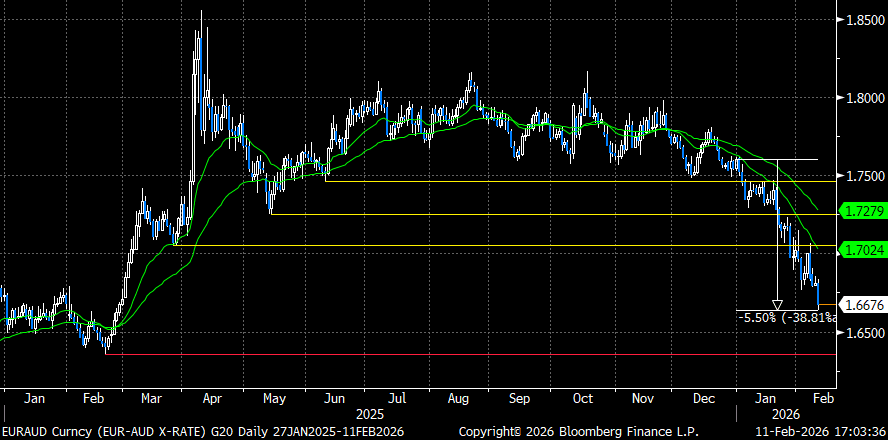

FOREX: EURAUD Extends 2026 Decline to 5.5%

Feb-11 17:03

- Divergent currency performance across the G10 has been notable on Wednesday, with conviction on the short-term direction for the dollar potentially clouded by the intricacies within the US employment report and immediate focus turning straight to Friday’s CPI print.

- Amid this dynamic, we pointed out that AUDCHF has had a notable 1% rally today and may be showing nascent signs of a technical breakout. Similar price action has weighed on EURAUD (-0.83%) today, which has allowed this year’s selloff to extend to 5.5% at today’s 1.6635 low.

- Momentum has steadily built on the break of significant horizontal chart levels, with the latest breach of 1.7050 weighing significantly. Furthermore, the 20-day EMA has acted as perfect resistance across this year, highlighting that AUD dips remain shallow and very well supported.

- All the action today has been underpinned by an aggressive stance from RBA’s Hauser, who despite citing caution and the need to prolong a policy pause in early Jan, has now aligned himself with Governor Bullock’s most recent rhetoric, stating the RBA will take all necessary measures to bring inflation under control.

- Westpac’s one month target for the cross is around 1.64, closely aligning with last year’s 1.6358 lows. They believe further material EUR/USD upside will likely encounter vocal resistance from the dovish ECB wing, while resilient metals prices and the prospect of higher super fund FX hedge ratios are additional factors weighing on EURAUD.