AMERICAS OIL: US OIL: March 13 - Americas End of Day Oil Summary: Crude Rises

US OIL: March 13 - Americas End of Day Oil Summary: Crude Rises

WTI reversed earlier losses and is near $100/bbl amid signs of an intensifying Iran war, and despite uncertainty around potential tanker traversals via the Strait of Hormuz. ULSD futures have also soared through $4/gal due to supply uncertainties with Gulf refineries under fire.

- US Baker Hughes oil rig count up 1 to 412.

- India is in active talks with Iran to allow at least 23 tankers through the Strait of Hormuz with the first crossings expected by the weekend, two Indian government officials told The Wall Street Journal. Two LPG tankers were reportedly granted passage.

- A Turkish-owned ship was allowed to pass through the Strait of Hormuz, Turkey’s transport minister said. It is not currently clear what vessel was allowed to pass through, and the report has not been verified by other outlets.

- The FT reported that Italy and France were in talks with Tehran seeking safe passage for their ships through the Strait of Hormuz. The Italian government later denied the report.

- The mixed messaging from the White House on the potential duration of the conflict remains in evidence. President Trump told Fox News that the US was going to be hitting Iran very hard over the next week.

- The Wall Street Journal reports that the US military is "moving a Marine expeditionary unit to the Middle East, as Iran steps up its attacks on the Strait of Hormuz..."

- The US has issued its second authorization for buyers to take Russian oil cargoes already at sea and loaded before March 12, widening a temporary waiver given last week to India.

- Adnoc cut the volume of crude for onshore partners by about a fifth for March, though flows will still go to a port outside the Strait of Hormuz, Bloomberg said.

- Saudi Arabia has cut oil production by 2m b/d to around 8m b/d after reducing output from two major offshore fields amid the Iran war, two sources told Reuters.

- Iraq’s Kirkuk crude flows to Turkey’s Ceyhan port restarted on March 13, according to Reuters.

- Cracks are higher after another refinery strike in the Middle East and with Sinopec set to cut refinery runs by >10% for March. Cracks have also been supported by a rising geopolitical risk premium later in the session.

- WTI Apr futures were up 2.9% at $98.71

- WTI May futures were up 2.4% at $96.63

- RBOB Apr futures were up 2.6% at $3.04

- ULSD Apr futures were up 2.8%at $4.01

- US gasoline crack up 1$/bbl at 29.22$/bbl

- US ULSD crack up 2.4$/bbl at 69.79/bbl

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

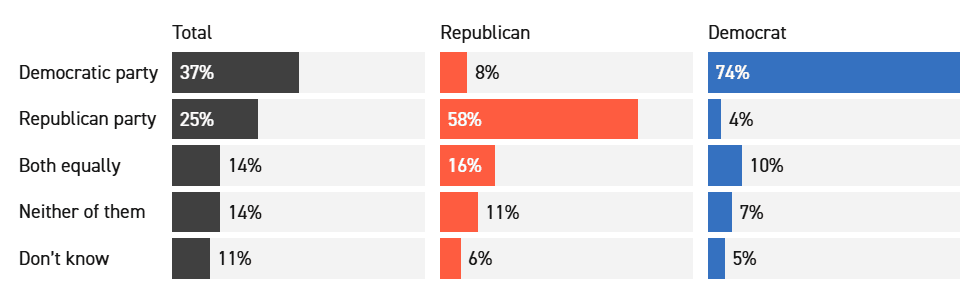

US: Voters Increasingly Back Democrats On Reducing Energy Costs

A new Politico survey has found that, “Slightly more Americans think Democrats, not Republicans, are the party most committed to reducing energy prices.” The outlet describes the results as, “yet another sign of potential trouble for President Donald Trump and the GOP on the issue of affordability.”

- Politico notes, “While far short of a majority, the edge for Democrats on the question is striking given the decades that surges in fuel costs have tormented nearly every Democratic president since Jimmy Carter, giving Republicans a message to hammer at election time. As recently as late 2024, polls showed most voters trusting Trump over Kamala Harris to shepherd the economy.”

- The report adds, “The results revealed a schism between Trump hardliners — self-identified “MAGA Trump” — and those who support the president but don’t consider themselves part of the Make America Great Again base. Sixty-nine percent of “MAGA Trump” voters said Republicans cared more than Democrats about reducing energy costs, compared with 34 percent of non-MAGA Trump voters.”

Figure 1: “Percentage of respondents, split by their intended midterm party vote, and which party they think wants to protect households from rising energy costs”

Source: Politico

FOREX: JPY Extends Post-Election Surge Despite Payrolls Volatility

- Higher-than-expected headline figures within the January US employment report sparked some recovery strength on Wednesday. However, intricacies within the report and the overarching bearish dollar narrative quickly sapped the initial greenback enthusiasm. The net impact is a slightly lower dollar index on the session, although this has been dragged by particularly strong performance for both the Japanese yen and the Australian dollar.

- The Japanese yen extended its post-election rebound in APAC trade, prompting USDJPY to fall to a 152.80 low. The pair recovered ahead of the US data, and had an aggressive spike to 154.65 following the release, however, the rally was extremely short-lived with a vicious reversal taking the pair back below 153 in rapid fashion.

- After a few hours of steadier trade between 153.20-80, spot has now edged back below 153.00 as has made fresh session lows below 152.80 as we approach the APAC crossover, further narrowing the gap to 152.10 support, the Jan 27 low.

- AUD outperformance has been linked to a stable session for equities and the positive performance for precious metals. Furthermore, a hawkish leaning RBA Hauser has underpinned the bullish AUD narrative, prompting AUDUSD to close in on the 2023 highs at 0.7158. Aussie strength has been very notable in the crosses, with the likes of EURAUD and GBPAUD extending their 2026 selloffs to around 5.5%, and AUDCHF showing nascent signs of a technical breakout, rising 1.15% today.

- In similar vein, the more stable session for the Euro and sterling have prompted solid corrections for EURJPY and GBPJPY, with the latter extending significantly below its 50-day EMA and the January lows to reach a session low of 208.45.

- UK GDP and US jobless claims highlight a lighter calendar on Thursday, before he focus turns to Friday’s release of US CPI.

US TSYS/SUPPLY: Review 10Y Auction: Tail

- Treasury futures moving lower (TYH6 -5.5 at 112-11) after the $42B 10Y note auction (91282CPZ8) tails: drawing 4.177% high yield vs. 4.162% WI; 2.39x bid-to-cover vs. 2.55x prior.

- Peripheral stats: indirect take-up retreats 64.54% vs. 69.65% prior; direct bidder take-up 22.08% from 24.51% prior; primary dealer take-up rises to 13.38% vs. 5.85% prior.

- The next 10Y auction is tentatively scheduled for March 11.