MNI ASIA MARKETS ANALYSIS: Crude Surge on Russia Oil Sanctions

HIGHLIGHTS

- Treasuries look to finish moderately weaker/near lows in a reaction to near 6% surge in crude prices after the US sanctioned Russia oil giants Rosneft and Lukoil overnight.

- Stocks hold moderately higher late Thursday, near late session highs but still off the prior session's early highs. Trade muted on day 23 of the US Govt shutdown while markets await Friday's delayed September CPI report.

- Ahead of the US CPI report, UK retail sales and Eurozone flash PMIs are expected. RBA Governor Bullock is also due to speak Friday.

US TSYS

MNI US TSYS: Tsy Yields Up With Surge in Crude, Sanctions on Russia Oil Giants

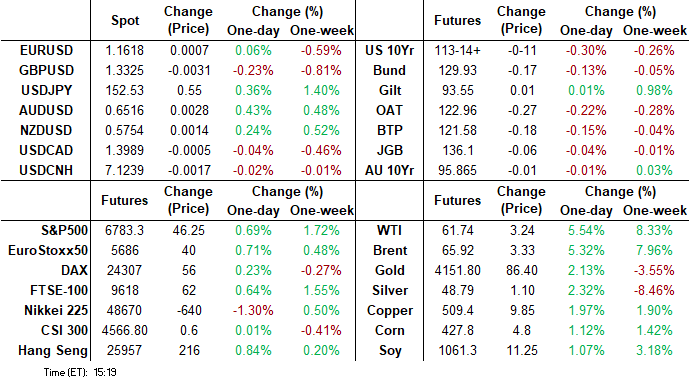

- Treasuries look to finish weaker-near late session lows, coinciding with a surge in crude oil (WTI +3.25 at 61.75), after the US sanctioned Russia oil giants Rosneft and Lukoil overnight.

- China and India are most affected by the new measures, with importers suspending purchases in the near-term. Late headlines annc Pres Trump expects to meet with Pres Xinext Thursday

- The Russian Foreign Ministry have issued its first comments following the announcement of US sanctions on oil giants Rosneft and Lukoil. Ministry spox says the sanctions are "counterproductive from the perspective of finding peace in Ukraine...If the US follows the example of previous US administrations, then it will be a failure".

- Currently, TYZ5 contract trades -11 at 113-14.5 vs. -13.5 low, 10Y yield at 3.9951% +.0458. Firm support lies at 113-06, the 20-day EMA. Moving average studies remain in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance.

- Look ahead to Friday's data: The median unrounded headline CPI estimate ticks up from 0.40 to 0.41% M/M and core ticks up from 0.30 to 0.32% but the broad story is unsurprisingly still the same.

- Equity earnings after the close include: Ford Motor Co, Newmont, Norfolk Southern, Western Union, Deckers Outdoor, Intel and Baker Hughes.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.21% (-0.02), volume: $2.956T

- Broad General Collateral Rate (BGCR): 4.18% (-0.03), volume: $1.152T

- Tri-Party General Collateral Rate (TCR): 4.18% (-0.03), volume: $1.123T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.11% (+0.00), volume: $91B

- Daily Overnight Bank Funding Rate: 4.11% (+0.00), volume: $180B

FED Reverse Repo Operation

RRP usage rebounds to $6.941B with 15 counterparties this afternoon from $4.005B Wednesday. Compares to $3,516B on Tuesday, Oct 13 (lowest level since early April 2021) & this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Overall SOFR/Treasury options flow mixed with some larger SOFR spreads focused on puts. Underlying futures lower - back to early Monday levels. Projected rate cut pricing retreats from late Wednesday levels (*): Oct'25 at -24.5bp (-24.7bp), Dec'25 at -47.4bp (-49.1bp), Jan'26 at -61.2bp (-64.2bp), Mar'26 at -73.9bp (-78.2bp).

SOFR Options:

Block, 7,000 0QZ5 96.93/97.06 put spds, 6.5 ref 97.065

+16,000 SFRH6 96.31/96.37 put spds, 1.5 vs. 96.64/0.06%

+5,000 SFRU6 97.50/98.00 call spds, 7.5 ref 96.62

6,000 SFRM6 96.62 puts ref 96.85

+5,000 0QH6 96.00/96.50 put spds, 3.0

+27,000 SFRM6 96.68/96.87 2x1 put spds, 4.0 ref 96.875 to -.885

10,000 SFRH6 96.75/96.87/97.00/97.12 call condors ref 96.62

1,500 0QM6 97.75/98.27/99.00 2x3x1 call flys ref 97.04

+6,250 SFRZ5 96.37/96.50/96.62 1x3x2 call flys, 0.5 ref 96.365

-2,000 SFRZ5 96.43/96.50/96.56 call flys, .25 ref 96.37

+over 3,700 0QX5 96.87 puts, 2 ref 97.07

1,250 SFRZ5 96.12/96.18 put spds ref 96.37

Treasury Options: Reminder, Nov options expire tomorrow

3,250 TYZ5 114 calls, 28 ref 113-15 vs 1,300 TYZ5 113 puts

4,194 TYZ5 111.5/116.5

2,000 TYZ5 113.5/114.5 strangles, 104 ref 113-18.5

+6,000 TYX5 113/TYZ5 114.5 1x2 call spds, 3 net/Dec bought over

-5,000 wk5 FV 108.75/109.25 put strip, 3.5

5,500 TYX5 113/113.25 put spds

over 6,600 TYX5 114 calls

+3,000 TUZ5 104.25 puts, 5.5

2,000 TUX5 104.12 puts, 0.5 ref 104-13.75

+2,500 TYX5 114 calls, 4

+5,000 TUF6 103.87/104.12/104.25/104.38 broken put condors, 0.5 vs. 104-17/0.04%

MNI EGB OPTIONS: Sonia Takes Centre Stage, Still Upside-Leaning

Thursday's Europe rates/bond options flow included:

- SFIZ5 96.20/96.25/96.30/96.35c condor, bought for 1.25 in 5k

- SFIH6 97.00/97.50cs, bought for 1 in 7.5k

- SFIH6 96.15/96.25/96.40/96.50c condor, bought for 2.75 in 2.5k

- SFIH6 96.65/96.80cs, bought for 2.25 in 10k

- SFIH6 96.50/96.85cs 1x2, bought for 4.75 in 7.5k

- SFIH6 96.45/96.65cs vs 96.30p, bought the cs for 3 in 5k

- 0NZ5 96.90/97.10/97.20 broken c fly, bought for 2 in 5k

MNI FOREX: USDJPY Rises with US Yields, NOK Boosted by Oil Price Surge

- US yields rose across the board on Thursday, assisted by the near 6% surge for crude futures on the back of sanctions on Russian oil producers. This dynamic has weighed on the Japanese yen specifically, allowing USDJPY to further extend its bounce to 152.80 session highs. Rallying equities following the US open has also provided a cross/JPY tailwind.

- Overall, the USD index is just 0.15% higher on Thursday, likely a result of market participants awaiting the US CPI report scheduled on Friday.

- Markets were leaning against GBP through the London close, helping pressure GBPUSD to new daily lows and, importantly, EURGBP through yesterday's post-inflation high. There's been no specific newsflow or headlines behind the GBP underperformance so far Thursday, however the currency is the second worst performer in G10.

- With EURGBP through 0.8713, markets are narrowing in on 0.8725 and 0.8751, the next key upside levels (marking the Oct 10 & 17 and Sep 25 high respectively).

- The Australian dollar tops the G10 leaderboard, with AUDJPY (+0.92%) a notable beneficiary of today’s dynamics. For AUDUSD, spot has risen back above 0.6500 and remains in consolidation mode. Attention is on the Oct 14 reversal pattern - a hammer candle. It signals the end of the bear cycle that started Sep 17. Note that moving average studies continue to highlight a dominant medium-term uptrend.

- NOK is off the session's strongest levels, but also continues to outperform the G10 basket amid today's solid rally in crude oil benchmarks. USDNOK is down 0.4%, testing support at 9.9754 (50% retracement of the September 17 to October 14 upswing). A breach would expose clustered support around the 9.9000 level.

- Ahead of the US CPI report, UK retail sales and Eurozone flash PMIs are expected. RBA Governor Bullock is also due to speak Friday.

MNI Political Risk – Argentina Midterm Election Preview

Argentina holds Congressional elections on Sunday, 26 October in a race that has garnered more international media and financial market attention than would usually be the case for a partial midterm election. Half the seats in the Chamber of Deputies and one-third of the Senate are up for election, with the outcome set to have a significant impact on President Javier Milei's ability to pass his policy programme through the legislature.

Full PDF Publication: https://mni.marketnews.com/4nfpo2l

MNI FX OPTIONS: Expiries for Oct24 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1460(E560mln), $1.1500-20(E1.3bln), $1.1635-50(E1.1bln)

- USD/JPY: Y150.00($2.0bln), Y151.00-20($1.4bln), Y152.00($583mln), Y152.50($596mln), Y153.80-00($574mln)

- AUD/USD: $0.6450(A$1.6bln)

MNI US STOCKS: Late Equities Roundup: Nearly Recovering Midweek Loses

- Stocks hold moderately higher late Thursday, near late session highs but still off the prior session's early highs. Trade muted on day 23 of the US Govt shutdown while markets await Friday's delayed September CPI report. Currently, the DJIA trades up 169.68 points (0.36%) at 46760.1, S&P E-Mini Future up 42 points (0.62%) at 6779.25, Nasdaq up 223.2 points (1%) at 22963.75.

- Energy and Information Technology sector shares led advances in late trade, the former buoyed by oil and gas stocks after the US sanctioned Russia oil giants Rosneft and Lukoil that helped crude prices rally (WTI +3.36 at 61.86): APA +6.82%, Valero Energy +6.57%, Marathon Petroleum +3.88%, Diamondback Energy +3.82% and Halliburton +3.38%.

- Semiconductor and hardware makers continued to support the Tech sector in late trade: Monolithic Power Systems +5.53%, Lam Research +4.69%, Teradyne +4.52%, KLA +3.89%, Applied Materials +3.67% and Micron +3.11%.

- Consumer Discretionary sector shares led declines with a couple notable outliers with Molina Healthcare -20.56% post earning citing rising costs, while Super Micro Computer -8.44% on weaker than expected sales.

- Autos and travel related stocks made up the balance of underperforming shares: Expedia Group -4.32%, O'Reilly Automotive -3.37%, AutoZone -3.18%, Booking Holdings -1.80% and Hilton Worldwide Holdings -1.76%.

- Earnings after the close include: Ford Motor Co, Newmont, Norfolk Southern, Western Union, Deckers Outdoor, Intel and Baker Hughes.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Trading Above Support

- RES 4: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 3: 6831.38 2.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6819.25 1.500 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6812.25 High Sep 9 and the bull trigger

- PRICE: 6746.00 @ 14:37 BST Oct 23

- SUP 1: 6621.99 50-day EMA

- SUP 2: 6540.25 Low Oct 10 and a key short-term support

- SUP 3: 6506.50 Low Sep 5

- SUP 4: 6427.00 Low Sep 2

The trend condition in S&P E-Minis remains bullish and the contract is trading above the 50-day EMA. The average, currently at 6632.20, has been pierced but remains intact - for now. Note that the Oct 10 low of 6540.25 marks the key short-term support. Clearance of this level would undermine a bull theme. Moving average studies remain in a bull-mode position, highlighting a dominant uptrend. The bull trigger is 6812.25, the Oct 9 high.

COMMODITIES

MNI AMERICAS OIL: US OIL: October 23 - Americas End of Day Oil Summary: Crude Surges

WTI crude futures have surged to a two-week high after the US sanctioned Lukoil and Rosneft. India is likely to make cuts in Russian crude imports, while China oil majors are showing reluctance in buying Russian crude as a result of the sanctions, according to Reuters.

- Both prompt and longer-term time spreads have rallied with Dec25-Dec26 returning into backwardation.

- Following the UK, US restrictions will be imposed against Lukoil and state-run Rosneft, two of the largest producers, aimed at reducing revenues for Russia’s war.

- Indian refiners have said that the US measures against Rosneft and Lukoil will make it extremely difficult for them to continue using Russian crude.

- India’s top refiner Reliance said it will “recalibrate” Russian oil imports in line with government guidelines following Trumps targeted measures towards Rosneft and Lukoil.

- US sanctions against Russia’s Rosneft and Lukoil are “the most material move to date by the United States to shutter the Russian war ATM,” according to RBC cited by Bloomberg.

- US sanctions on Rosneft and Lukoil are expected to trigger a short-term drop in exports and support oil prices as traders rebuild supply chains, according to Kpler.

- China oil majors are showing reluctance towards Russian barrels on Thursday as Western sanctions mount, Reuters reports.

- WTI Dec futures were up 5.7% at $61.79

- WTI Jan futures were up 4.9% at $61.18

MNI: New Russian Oil Sanctions: Overview and Implications

Executive Summary: The U.S. has initiated new sanctions on leading Russian crude exporters Rosneft and Lukoil.

- China and India are most affected by the new measures, with importers suspending purchases in the near-term

- In the longer-term, India’s imports are expected to be more impacted than Russia-China flows.

- Download Full Report Here

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 24/10/2025 | 0600/0800 | ** | PPI | |

| 24/10/2025 | 0600/0700 | *** | Retail Sales | |

| 24/10/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 24/10/2025 | 0700/0900 | ** | PPI | |

| 24/10/2025 | 0715/0915 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0715/0915 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0730/0930 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0730/0930 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Services PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Manufacturing PMI (p) | |

| 24/10/2025 | 0800/1000 | ** | S&P Global Composite PMI (p) | |

| 24/10/2025 | 0800/1000 | ECB Cipollone Fireside Chat on International Finance | ||

| 24/10/2025 | 0830/0930 | *** | S&P Global Manufacturing PMI flash | |

| 24/10/2025 | 0830/0930 | *** | S&P Global Services PMI flash | |

| 24/10/2025 | 0830/0930 | *** | S&P Global Composite PMI flash | |

| 24/10/2025 | 1200/0800 | ** | Brazil Preliminary CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1230/0830 | *** | CPI | |

| 24/10/2025 | 1300/1500 | ** | BNB Business Confidence | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Manufacturing Index (Flash) | |

| 24/10/2025 | 1345/0945 | *** | S&P Global Services Index (flash) | |

| 24/10/2025 | 1400/1000 | *** | New Home Sales | |

| 24/10/2025 | 1400/1000 | *** | U. Mich. Survey of Consumers | |

| 24/10/2025 | 1400/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 24/10/2025 | 1400/1000 | *** | New Home Sales | |

| 24/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 24/10/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |