MNI ASIA MARKETS ANALYSIS: CPI Softer, Stocks Make New Highs

HIGHLIGHTS

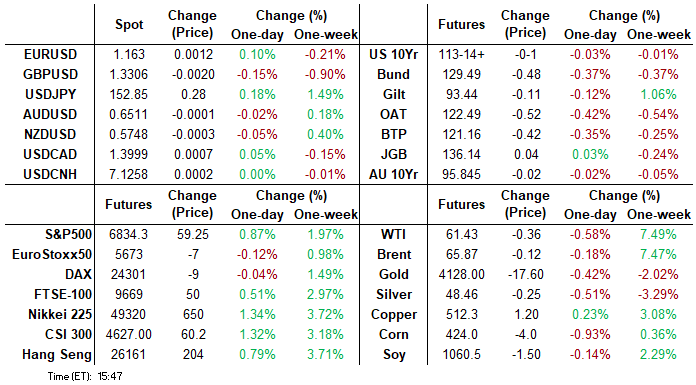

- Treasuries drift in mildly negative territory after the bell - well off this morning's post-CPI data highs - Core CPI was clearly softer than expected in September, rising a seasonally adjusted 0.23% M/M.

- WH suggests that the BLS may not release an October inflation report because it was unable to conduct the in-person surveys as normal during October due to the shutdown.

- The dollar index declined around 30 pips in the immediate aftermath, however, downside momentum quickly stalled. Overall, the DXY is unchanged on the session as we approach the weekend close.

- While the US Gov shutdown is likely to continue into next week, the focus is on Wednesday's FOMC policy annc

US TSYS

MNI US TSYS: Tsys Reject Post-CPI Rally, Mildly Lower, Focus on Next Week's FOMC

- Treasuries look to finish mildly weaker Friday - well off knee-jerk highs after the Sep CPI inflation data came out lower than expected. Core rose a seasonally adjusted 0.23% M/M (median unrounded expectation of 0.32) and with the miss translating into the non-seasonally adjusted Y/Y rate at 3.02% (cons 3.1) after two months at 3.1%.

- White House's Rapid Response account on X.com suggests that the BLS may not release an October inflation report because it was unable to conduct the in-person surveys as normal during October, on account of the shutdown.

- Tsys extended lower after S&P flash PMI (link) noted strong business activity growth (second-fastest of the year) although prices charged rose at their softest rate since April. Tsys held modestly weaker levels after lower than expected UofM sentiment, current conditions and expectations, while 5-10Y inflation exp rises slightly.

- Tsy Dec'25 10Y contract currently at 113-14.5 (-1) vs. 113-09.5 low, 10Y yld 3.9969% -.0040; curves mildly steeper: 2s10s +0.667 at 51.270, 5s30s +1.634 at 98.433. Moving average studies are in a bull-mode position and this set-up highlights a dominant uptrend. Sights are on 114-10, the Apr 7 high (cont) and the next key resistance. Firm support lies at 113-06+, the 20-day EMA.

- The dollar index declined around 30 pips in the immediate aftermath, however, downside momentum quickly stalled. Overall, the DXY is unchanged on the session.

- Stocks gapped to new record highs following Friday morning's lower than expected CPI inflation data, sentiment buoyed as the report underscored expectations of two 25bp rate cuts by year end.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.24% (+0.03), volume: $3.002T

- Broad General Collateral Rate (BGCR): 4.21% (+0.03), volume: $1.145T

- Tri-Party General Collateral Rate (TCR): 4.21% (+0.03), volume: $1.113T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.11% (+0.00), volume: $93B

- Daily Overnight Bank Funding Rate: 4.11% (+0.00), volume: $173B

FED Reverse Repo Operation

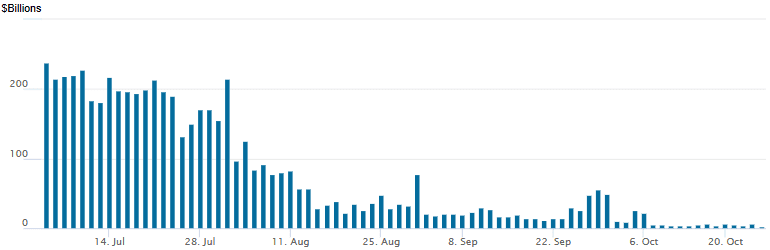

RRP usage retreats to $2.435B (lowest level since mid-March 2021) with 4 counterparties this afternoon from $6.941B Thursday. Compares to this year's high usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

SOFR/Treasury options flow remained mixed on decent volumes after lower than expected CPI inflation data for Sep at underscored projected rate cut pricing vs. late Thursday levels (*): Oct'25 at -24.2bp (-24.5bp), Dec'25 at -50.2bp (-47.4bp), Jan'26 at -63.7bp (-61.2bp), Mar'26 at -75.8bp (-73.9bp).

SOFR Options:

-5,000 SFRX5SFRZ5 96.25/96.37 put spd strip, 5.5 ref 96.37

+20,000 SFRZ5 96.25/96.43/96.62 call flys, 9.5

-10,000 SFRZ5 96.25/96.37/96.43/96.56 iron condors, 4.5 ref 96.38

Block, 5,000 SFRZ5 96.12/96.25 put spds, 1.25 ref 96.38

+20,000 SFRZ5 96.50/96.62 call spds, 1.25 ref 96.375

-1,500 SFRZ5 96.37 straddles, 11.5-11.0

3,000 2QF6 96.12/96.37/96.62 put flys ref 96.855

2,000 SFRZ5 96.25/96.37/96.50 call flys

+3,000 SFRH6 96.43/96.50/96.62 broken put trees, .25 vs. 96.595/0.20%

2,000 SFRZ5 96.25/96.37 call spds

+4,000 0QZ5 97.18 calls, 8.5 ref 97.02

-2,000 SFRX5 96.31 puts, 2.5

+2,000 2QX5 97.12/97.37 call spds, 2.5 ref 96.915

Treasury Options: Reminder, Nov options expire today

+14,000 TYH6 111.5/115.5 strangles

Block: +7,500 TYH6 116 calls. 28 w/ +20,000 TYH6 111 puts, 27

-20,000 FVZ5 110.75 calls, 6

10,000 TYZ5 115/115.5/116 call flys ref 113-16

+60,000 USZ5 107 puts, 1 - and looking for more

-4,000 TYZ5 113.5 straddles, 109

2,000 TYZ5 113.5/114.5/115 1x3x2 broken call flys

Block, 11,605 TYZ5 111.5 puts, 3 vs. 113-24/0.08%

-9,000 FVZ5 110.5/111.5 call spds, 8

-4,000 TYX 114 calls, 1

+2,500 TYX5 113.25/113.75 call spds, 15 ref 113-12.5

+3,000 TUX5 104.25 puts, 1 vs. 104-12/0.22%

+2,000 TYX5 113.75/114 call spds, 2 ref 113-12

+3,500 TYX5 112.75/113 put spds, 3 ref 113-11

+3,000 FVX5 109/109.5 put spds, 4 ref 109-20.75

1,600 TYZ5 111/112 put spds ref 113-11.5

2,000 TYX5 113.5/113.75 call spds, 5 ref 113-12.5

MNI FOREX: USD Weakness Short-Lived Following Soft US CPI

- Following the US CPI data, US yields were pressured lower, naturally weighing on the US dollar. Headline CPI came in on the lower side of expectations in September (headline 0.31% M/M vs 0.40% median expected, 0.38% prior), built largely on the miss in core categories.

- The dollar index declined around 30 pips in the immediate aftermath, however, downside momentum quickly stalled. Overall, the DXY is unchanged on the session as we approach the weekend close.

- The positive impulse for major US equity benchmarks has continued to underpin the outperformance for Cross/JPY on Friday, with USDJPY looking to extend its winning streak to six sessions, currently hovering just below 153.00. Japanese politics have been the key driver all week, as the market continues to assess PM Takaichi’s new cabinet and an imminent stimulus package said to be in the works.

- Despite Eurozone flash PMIs and the US data, EURUSD has remained in a 47pip range Friday. For Germany, in addition to the stronger growth signals, an uptick in output charge inflationary pressures added to the hawkish theme of the flash PMI report.

- US dollar declines were most notable for gold, where XAU/USD sharply recovered around 2% from pre-data levels to trade at levels close to $4,120, still roughly $260 off the recent record highs.

- Over the weekend, it is worth noting that daylight saving time shifts will occur across Europe. On Sunday, there are midterm elections in Argentina. Monday’s data calendar is highlighted by German IFO, while RBA Governor Bullock will speak.

MNI OPTIONS: Expiries for Oct27 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1520-35(E1.5bln), $1.1620-40(E1.6bln), $1.1650(E548mln), $1.1670-80(E1.4bln), $1.1700-10(E1.1bln)

- USD/JPY: Y152.00($531mln)

- AUD/USD: $0.6490(A$2.0bln)

- USD/CAD: C$1.4100($793mln)

MNI US STOCKS: Late Equities Roundup: Drifting Near Record Highs, Tech & Banks Lead

- Stocks gapped to new record highs following Friday morning's lower than expected CPI inflation data, sentiment buoyed as the report underscored expectations of two 25bp rate cuts by year end.

- Currently, the DJIA trades up 534.44 points (1.14%) at 47,268.3 vs. 47,326.73 record high, S&P E-Minis up 62.5 points (0.92%) at 6,837.5 vs. 6,841.25 record high, Nasdaq up 295.8 points (1.3%) at 23,237.64 vs. 23,256.37 record high.

- Information Technology and Financials sector shares continued to lead advances in late trade, Tech stocks outperforming for the second day running: IBM +8.17%, Advanced Micro Devices +6.98%, Micron Technology +4.87%, First Solar +4.47% and Seagate Technology +3.74%

- Financial sector shares followed: Coinbase Global +8.67%, Goldman Sachs +3.85%, Robinhood Markets +3.25%, Morgan Stanley +2.81%, PNC Financial Services +2.58% and Apollo Global Management +2.56%.

- A mix of Energy and Materials sector shares led declines in the second half: Baker Hughes -3.27%, APA -2.15%, Targa Resources -2.08%, ConocoPhillips -1.81% and Halliburton -1.75%; Newmont -4.72%, Packaging Corp of America -2.72%, Avery Dennison -1.66%, Amcor -1.03% and Linde -0.73%.

- The following kick off next week's heavy earnings announcement schedule: Keurig Dr Pepper, Whirlpool, Waste Management, Bed Bath & Beyond, Nucor, Brown & Brown, Welltower and Cadence Design Systems.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Fresh Cycle High

- RES 4: 6900.00 Round number resistance

- RES 3: 6890.00 1.764 proj of the Aug 1 - 15 - 20 price swing

- RES 2: 6850.87 1.618 proj of the Aug 1 - 15 - 20 price swing

- RES 1: 6841.25 Intraday high

- PRICE: 6838.75 @ 1427 ET Oct 24

- SUP 1: 6721.65 20-day EMA

- SUP 2: 6637.80 50-day EMA

- SUP 3: 6540.25 Low Oct 10 and a key short-term support

- SUP 4: 6506.50 Low Sep 5

The trend condition in S&P E-Minis remains bullish and the contract has traded higher today, breaching resistance at 6812.25, the Sep 9 high. This confirms a resumption of the primary uptrend and maintains the bullish price sequence of higher highs and higher lows. Sights are on 6850.87, a Fibonacci projection. Initial support to watch lies at 6721.62, the 20-day EMA. The 50–day EMA is at 6637.80.

COMMODITIES

MNI AMERICAS OIL: US Oil Summary at Close: WTI Up 7% on Week

WTI has relinquished earlier gains to be slightly lower on the day but maintains most of yesterday’s strong rise and is set for a weekly net increase of around 7% following US sanctions on Russia.

- WTI DEC 25 down 0.3% at 61.61$/bbl

- Baker Hughes rig count: oil: 420 (2) - down 60 rigs, or 12.5% on the year.

- Ukrainian President Volodymyr Zelensky urged Kyiv’s allied to introduce sanctions against all Russian oil companies, its shadow fleet, and the country’s oil terminals

- "Russia-US dialogue is vital for the world and must continue with the full understanding of Russia's positions and respect for its national interests." Kirill Dmitriev, President Putin's special envoy

- Baker Hughes’ broader 2025 outlook remains unchanged, with a projected high single-digit decline in global upstream spending, Reuters reported.

- WTI is still expected to average $52/b next year: Goldman Sachs.

- US sanctions could lead to Russian supply losses of several hundred thousand b/d: HSBC. It maintains a $65/b brent price from Q4.

MONDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 27/10/2025 | 0900/1000 | ** | M3 | |

| 27/10/2025 | 0900/1000 | *** | IFO Business Climate Index | |

| 27/10/2025 | 0900/1000 | ** | ECB Consumer Expectations Survey | |

| 27/10/2025 | 0915/1015 | ECB Elderson Keynote on Banking Governance | ||

| 27/10/2025 | 1100/1100 | ** | CBI Distributive Trades | |

| 27/10/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/10/2025 | 1230/0830 | ** | Durable Goods New Orders | |

| 27/10/2025 | 1430/1030 | ** | Dallas Fed manufacturing survey | |

| 27/10/2025 | 1530/1130 | * | US Treasury Auction Result for 26 Week Bill | |

| 27/10/2025 | 1530/1130 | * | US Treasury Auction Result for 2 Year Note | |

| 27/10/2025 | 1700/1300 | * | US Treasury Auction Result for 13 Week Bill | |

| 27/10/2025 | 1700/1300 | * | US Treasury Auction Result for 5 Year Note | |

| 28/10/2025 | 0001/0001 | * | BRC Monthly Shop Price Index |