MNI ASIA MARKETS ANALYSIS: Bonds Bounce, House Passes Megabill

HIGHLIGHTS

- The House of Representatives has passed the GOP tax and spending bill in a 215-214 vote, with two Republicans voting 'no'.

- S&P Global US flash PMIs for May were comfortably stronger than expected for both manufacturing and services, as they better reflected the de-escalation in US-China trade policies on May 12.

- Fed Chair Powell is scheduled to deliver Semi-Annual Monetary Policy testimony before the House Financial Services Committee on Tuesday June 24 at 1000ET.

MNI US TSYS: At/Near Late Session Highs, Curves Mixed After Bond Bounce

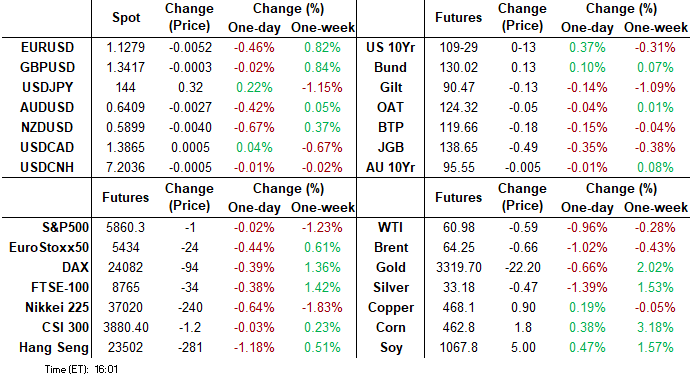

- Unwinding early weakness, Treasuries futures look to finish at/near session highs - trading sideways since midday. Rates opened weaker after the House has passed revised tax/spending bill. Jun'25 10Y futures currently trade +13.5 at 109-29.5, 109-26 high. Key near-term resistance has been defined at 110-21+, the May 16 high. A move above this level is required to signal a potential reversal.

- The revised bill sharpens language on Biden-era Inflation Reduction Act clean energy credits. While it doesn’t rescind the credits entirely, it cuts them off sooner and makes then more difficult to attain. It also softens the rollback of credits for advanced nuclear reactors – a win for the nuclear sector.

- Intermediate to long end Treasury futures remain under pressure after slightly lower than expected weekly claims, Continuing Claims higher than expected though prior is down-revised. Rates remained under pressure after S&P flash PMIs come out higher than expected.

- Manufacturing: 52.3 (cons 49.9, 20 responses) in the May prelim after 50.2 in April – highest since Feb and before that Jun 2022. Services: 52.3 (cons 51.0, 16 responses) in the May prelim after 50.8 in April – highest since March.

- That said, there were no obvious headline or block driver as Treasury futures extend session highs around midday, curves turned mixed, off steeper levels as bonds rebound: 2s10s -3.235 at 54.466, 5s30s +1.942 at 94.934.

- Cross asset: BBG UD$ index off highs (BBDXY +1.86 at 1220.70 vs. 1222.36)., Gold declines to 3293.15, Stocks mixed, SPX eminis little firmer at 5874.0 (+12.75).

REFERENCE RATES (PRIOR SESSION)

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.26% (-0.01), volume: $2.517T

- Broad General Collateral Rate (BGCR): 4.26% (+0.00), volume: $1.043T

- Tri-Party General Collateral Rate (TCR): 4.26% (+0.00), volume: $1.013T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 4.33% (+0.00), volume: $118B

- Daily Overnight Bank Funding Rate: 4.33% (+0.00), volume: $300B

FED Reverse Repo Operation

RRP usage inches up to $173.018B this afternoon from $162.082B yesterday, total number of counterparties at 37. Usage had fallen to $54.772B last Wednesday, April 16 -- lowest level since April 2021. Conversely, usage had surged to the highest level since December 31, 2024 on Monday, March 31: $399.167B.

US SOFR/TREASURY OPTION SUMMARY

Option desks reported lighter SOFR & Treasury option flow Thursday, SOFR still leaning towards low delta puts as underlying futures trade steady to mildly weaker out to SFRZ5. Projected rate cut pricing holds steady to mildly weaker vs. morning levels (*) as follows: Jun'25 steady at -1.3bp, Jul'25 at -7bp (-7.5bp), Sep'25 at -20.2bp (-21.5bp), Oct'25 at -33.5bp (-35.5bp), Dec'25 at -50.3bp (-52.5bp).

SOFR Options:

Block, 10,000 0QN5 96.18 puts, 4.0 vs. 8,000 0QN5 96.37 puts, 8.5

+2,500 SFRZ5 95.62 puts, 3.0 vs. 96.195/0.12%

+2,500 2QM5 96.00/96.25 put spds, 1.5 ref 96.565

-4,000 SFRU5 95.25/95.75 put spds, 5.0 ref 95.90

+2,500 SFRZ5 95.62/96.00 put spds 0.5 over SFRV5 96.00 puts ref 96.175

+25,000 SFRZ5 95.68 puts, 4.0 - position build appr 150,000 (total open interest 286,204)

+5,000 SFRN5 95.56/95.62/95.75 2x3x1 put flys, 1.25 ref 95.92

-2,500 SFRM5 95.75/95.87/96.00 put flys, 3

+2,000 0QN5 96.00/96.25/96.50 put flys, 5.0 ref 96.60

+2,000 0QQ5 96.00/96.25/96.50 put flys, 4.5 ref 96.59

Treasury Options:

1,000 TYN5 109.5 straddles, 146

2,500 FVN5 108.5 calls, 13.5

2,000 TYM5 109/109.25 put spds ref 109-16

-2,000 TYM5 109.5/110 put spds, 18 vs. 109-20.5/0.10%

1,100 USN5 106/108 put spds ref 110-13

+2,000 TYN5 108 puts, 20 vs TYU5 109-20/0.22%

+2,000 FVM5 107.75 calls, 2.5

+4,800 TYN5 106.5/108.5 put spds, 23 ref 109-16.5/0.21%

-2,500 TYQ5 108/112 call over risk reversals, 18 vs. 109-17.5/0.53%

MNI BONDS: EGBs-GILTS CASH CLOSE: Countervailing Factors See Twist Steepening

Long-end European bonds remained under pressure Thursday, though yields closed near session lows.

- After gapping higher at the open, yields traded mixed across the curve through the rest of the day. Short-end instruments rallied consistently, with long-end (particularly 30Y) Gilts and Bunds seeing the weakest levels in early afternoon before staging a partial recovery.

- Multiple factors were at play. The short end benefited from dovish ECB repricing after weak flash eurozone Services PMIs.

- Eurozone and UK curves twist steepened however, with longer-dated global yields remaining underpinned by US fiscal concerns as expansive fiscal legislation moved closer to fruition in Washington.

- The twist steepening held by session's cash close in both Germany and the UK, though yields finished near the lows and futures continued to rally after the close.

- The ECB's April meeting accounts noted that "it was argued that the optimal monetary policy response depended on the outcome of tariff negotiations".

- Periphery/semi-core EGB spreads mostly widened in a mixed day for risk assets.

- Friday's calendar highlight is UK retail sales, while we also get German GDP data and French consumer confidence, as well as ana appearance by ECB's Lane.

Closing Yields / 10-Yr EGB Spreads To Germany:

- Germany: The 2-Yr yield is down 4bps at 1.831%, 5-Yr is down 2.1bps at 2.172%, 10-Yr is down 0.3bps at 2.643%, and 30-Yr is up 1.5bps at 3.151%.

- UK: The 2-Yr yield is down 5.2bps at 4.031%, 5-Yr is down 4bps at 4.201%, 10-Yr is down 0.6bps at 4.751%, and 30-Yr is up 3.2bps at 5.55%.

- Italian BTP spread up 1.3bps at 100.9bps / French OAT up 1.3bps at 68bps

MNI OPTIONS: Outright Euribor Call Buying Stands Out Thursday

Thursday's Europe rates/bond options flow included:

- RXM5 130.00/129.50 put spread sold at 22.5 in 10k - hearing unwind ahead of Friday expiry

- ERM5 98.06 calls bought for 0.75 in 10k

- ERM5 98/98.25 call spread vs 97.87/97.62 put spread, sells call spread at 0.75 in 5k

- ERQ5 98.1875/98.3125/98.4375 call fly bought for 2.25 in 4k

- SFIU5 96.10/96.25cs, bought for 3.75 in 4k

- SFIZ5 96.75/97.25 call spread paper paid 3 on 4K

MNI FOREX: USD Trades with Constructive Tone, JPY Volatility Stands Out

- The US Dollar has traded on a firmer footing Thursday, with the USD index currently up around 0.55% as we approach the APAC crossover. This theme has been underpinned by a more stable session for treasuries, where yields have had a strong reversal lower from the week’s highest levels. Nominal 30Y yields are down 9-10bp from highs, having rejected the 2023 peak around 5.15% for now.

- The most notable moves in G10 FX were once again dominated by the volatile Japanese yen, which remains sensitive to both domestic headlines and the prevailing sentiment surrounding US assets. USDJPY received an early session boost to 144.40 on headlines related to the meeting between US Tsy Secretary Bessent and Japan FinMin Kato where they discussed a shared belief that exchange rates should be market determined.

- However, this sentiment was quickly faded, and subsequent headlines from BOJ’s Noguchi on not intervening in JGB bond markets and the initial twist steepening of the treasury curve prompted an impressive USDJPY selloff to session lows of 142.81. In another impressive swing, the subsequent flattening of the US curve and late comments on no secret talks on fx policy from Miran extended a relief recovery back towards session highs.

- Separately, EUR weakness has stood out following weaker-than-expected German and Eurozone flash services PMIs. Price action has been uninspiring, however, EURUSD is down 0.5% on Thursday, with spot gravitating towards the 1.1265 mark, but still up over a big figure on the week. Single currency weakness also stands out against sterling, as EURGBP has also fallen around half a percent to trade below 0.8400 and close in on last week’s pullback lows located at 0.8394. GBPUSD has broadly respected a 1.3400-50 range, outperforming the likes of AUD and NZD which have adjusted lower in tandem with the broader greenback strength.

- New Zealand retail sales and Japan national CPI data are due in Friday’s APAC session. This will be followed by UK and Canadian retail sales, with US new home sales highlighting the US docket.

MNI OPTIONS: Expiries for May23 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1145-50(E1.1bln), $1.1180-85(E1.1bln), $1.1225-30(E746mln), $1.1295-00(E1.7bln), $1.1330-50(E1.3bln), $1.1400(E1.1bln), $1.1495-05(E1.9bln)

- USD/JPY: Y143.00($1.4bln), Y143.20-40($788mln), Y143.50($598mln), Y144.00($2.1bln), Y144.35-50($1.1bln), Y145.00($2.2bln)

- EUR/JPY: Y160.90-00(E570mln)

- AUD/USD: $0.6375(A$684mln)

- USD/CAD: C$1.4000-15($1.3bln)

Table of Contents

US STOCKS: Late Equities Roundup: Looking Past Long-Term Deficit Cares for Now

- Stocks continued to make modest gains late Thursday, despite concerns over a burgeoning deficit as Pres Trump's tax/spending bill heads to the Senate after passing the House early this morning.

- Currently, the DJIA trades up 163.27 points (0.39%) at 42023.82, S&P E-Minis up 21 points (0.36%) at 5882.75, Nasdaq up 145.5 points (0.8%) at 19018.16.

- Communication Services and Information Technology sectors continued to outperform in lat etrade, interactive media and entertainment shares gained for the second consecutive session with Alphabet +2.53%, Walt Disney +0.89%, Match Group +0.78% and Meta Platforms +0.51%.

- The Tech sector was supported by chip makers and software developers: Palantir Technologies +3.69%, Seagate Technology +3.42%, Palo Alto Networks +2.63% and Crowdstrike Holdings +2.55%.

- On the flipside, Energy and Health Care sectors underperformed in the second half, wires cited passage of the tax/spending bill triggered heavy selling in clean energy companies: Enphase Energy -18.44%, NextEra Energy -7.18%, AES Corp -4.10% and CMS Energy -1.70%.

- Meanwhile, the Health Care sector was weighed down by Humana -4.92%, Medtronic -3.61% and Centene -2.82%.

MNI EQUITY TECHS: E-MINI S&P: (M5) Corrective Pullback

- RES 4: 6080.75 High Feb 26

- RES 3: 6057.00 High Mar 3

- RES 2: 6000.00 Round number resistance

- RES 1: 5993.50 High May 20

- PRICE: 5888.25 @ 1525 ET May 22

- SUP 1: 5837.25/5709.84 High Mar 25 / 50-day EMA

- SUP 2: 5455.50 Low Apr 30

- SUP 3: 5355.25 Low Apr 24

- SUP 4: 5127.25 Low Apr 21 and a key support

A bullish trend condition in S&P E-Minis remains intact and the latest pullback is considered corrective. An important resistance at 5837.25, the Mar 25 high and a bull trigger, has recently been cleared. This has strengthened the current bullish theme, and paves the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5709.84, the 50-day EMA. A clear break of it would highlight a potential reversal.

Table of Contents

COMMODITIES: Crude Falls, Precious Metals Pull Back

- Oil has fallen further today, with pressure from concerns over US demand and expectations of another large output hike from OPEC+ from June.

- WTI Jul 25 is down by 0.6% at $61.2/bbl.

- A majority of traders and analysts surveyed by Bloomberg see OPEC+ agreeing on another large 411k b/d supply increase for July in its June 1 meeting.

- For WTI futures, a continuation lower would refocus attention on $54.33, the Apr 9 low and bear trigger. On the upside, key resistance to watch is $62.75, the 50-day EMA.

- Meanwhile, spot gold has fallen by 0.6% today to $3,295/oz, with the yellow metal pulling back from earlier session highs at $3,345, close to initial resistance.

- Medium-term trend signals remain bullish - moving average studies are in a bull-mode position highlighting a dominant uptrend.

- A continuation above initial resistance at $3,347.5, the May 9 high, would open $3,435.6 next, the May 7 high. Key support and the bear trigger has been defined at $3,121.0, the May 15 low.

- Similarly, silver has pulled back today, with the precious metal falling by 0.9% to $33.1/oz, having reached its highest level since April 03 earlier in the session.

- A bullish theme in silver remains intact. Initial resistance at $33.686, the Apr 25 high, has been pierced, and a clear break of it would confirm a resumption of the uptrend.

- Key short-term support has been defined at $31.651, the May 15 low.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 23/05/2025 | 0600/0800 | ** | Unemployment | |

| 23/05/2025 | 0600/0700 | *** | Retail Sales | |

| 23/05/2025 | 0600/0800 | *** | GDP (f) | |

| 23/05/2025 | 0645/0845 | ** | Consumer Sentiment | |

| 23/05/2025 | 0830/1030 | ECB's Lane Inflation Lecture in Florence | ||

| 23/05/2025 | 1230/0830 | * | Quarterly financial statistics for enterprises | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1230/0830 | ** | Retail Trade | |

| 23/05/2025 | 1335/0935 | Kansas City Fed's Jeff Schmid | ||

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1400/1000 | *** | New Home Sales | |

| 23/05/2025 | 1600/1800 | ECB's Schnabel Speech on Financial Education and Monpol | ||

| 23/05/2025 | 1600/1200 | Fed Governor Lisa Cook | ||

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 23/05/2025 | 1700/1300 | ** | Baker Hughes Rig Count Overview - Weekly |