MNI ASIA MARKETS ANALYSIS: BOE on Hold, Tsy Yields Declining

HIGHLIGHTS

- Treasuries trade sideways since marking session highs in late Thursday trade - early support after Revelio Labs' estimate of October nonfarm payrolls growth came in at -9.1k vs +33.0k prior.

- Federal Reserve Bank of Cleveland President Beth Hammack said Thursday interest rates should stay where they are to ensure inflation returns to goal, adding monetary policy is "only barely restrictive, if that.

- Early focus was the BOE decision: the MPC held rates by a 5-4 vote. That saw an initial hawkish move in Gilts (there had been around 33% market-implied prob of a cut).

US TSYS

MNI US TSYS: Yields Retreat, Alternative Employment Data Lagging

- Treasuries are trading sideways since climbing to session highs late Thursday morning, markets turning towards alternative employment data due to the ongoing US Govt shutdown.

- Revelio Labs' estimate of October nonfarm payrolls growth came in at -9.1k vs +33.0k prior (rev from +60.1k) and August's actual figure reported by the BLS of +22k (Revelio estimates Aug at +14.5k). That is the first negative M/M reading for the Revelio series since May.

- Fed speak: Chicago Fed's Goolsbee (2025 FOMC voter) says his bank's October labor estimates (4.36% unemployment rate) are consistent with labor market "stability". "To me, most of the labor market indicators that we're getting show a lot of stability in the market....I still think there's mild cooling."

- Federal Reserve Bank of Cleveland President Beth Hammack said Thursday interest rates should stay where they are to ensure inflation returns to goal, adding monetary policy is "only barely restrictive, if that. At this point, I don’t think there is more that monetary policy can do without risking a fall off the wire,"

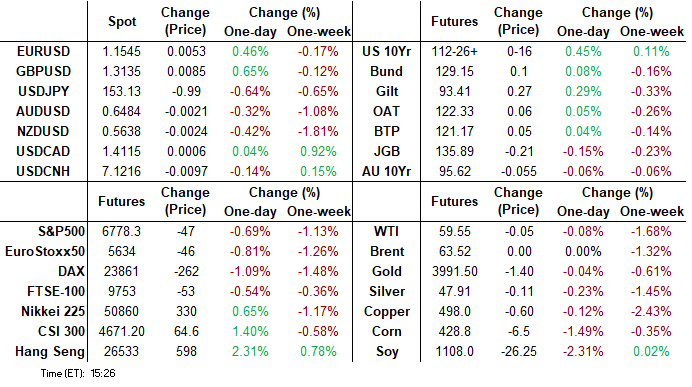

- Currently, the Dec'25 10Y contract trades +15.5 at 112-26 vs. 112-30 high. Initial key near-term resistance is seen at 113-02, the Nov 5 high. The week's steepening in 2s10s stalled (-.022 at 52.528) while 5s30s continued to gain (+2.461 at 99.703).

- Projected rate cut pricing gaining vs. morning levels (*): Dec'25 at -17.2bp (-16.6bp), Jan'26 at -26.1bp (-24.6bp), Mar'26 at -35bp (-33.2bp), Apr'26 at -40.6bp (-38.9bp).

- Due to the ongoing US Govt shutdown, the employment report for October produced by the Bureau of Labor Statistics is suspended. Fed speakers, University of Michigan Sentiment / Expectations and Consumer Credit expected.

REFERENCE RATES

US TSYS: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 3.91% (-0.09), volume: $3.145T

- Broad General Collateral Rate (BGCR): 3.88% (-0.10), volume: $1.195T

- Tri-Party General Collateral Rate (TCR): 3.88% (-0.10), volume: $1.171T

- (rate, volume levels reflect prior session)

STIR: FRBNY EFFR for prior session:

- Daily Effective Fed Funds Rate: 3.87% (+0.00), volume: $94B

- Daily Overnight Bank Funding Rate: 3.87% (+0.00), volume: $166B

FED Reverse Repo Operation

RRP usage slips to $10.754B with 14 counterparties this afternoon - from $12.700B Wednesday. Compares to $2.435B on October 24 (lowest level since mid-March 2021) and the year's highest usage of $460.731B on June 30.

US SOFR/TREASURY OPTION SUMMARY

Active SOFR/Treasury option session, two-way on the former as low delta put interest flowed then ebbed, heavy Jan'26 10Y call buying as Dec'26 option positions expire in two weeks. Underlying drifting near midday highs. Projected rate cut pricing gaining vs. morning levels (*): Dec'25 at -17.2bp (-16.6bp), Jan'26 at -26.1bp (-24.6bp), Mar'26 at -35bp (-33.2bp), Apr'26 at -40.6bp (-38.9bp).

SOFR Options:

4,000 SFRZ5 96.25 straddles, 14.25 ref 96.255

Update, over +15,000 SFRZ5 96.18/96.25/96.31/96.37 call condors, 2.0 ref 96.24

+5,000 0QG6 97.00/97.25 call spds 3.25 over 96.50 put vs. 96.905/0.33%

+10,000 SFRZ5 96.25/96.31 put spds, 3.0 ref 96.255

-10,000 0QU6 98.00 calls, 5.0

+4,000 SFRZ5 96.31/96.43 call spds, 2.75 vs. 96.265

Block, 10,000 0QZ5 96.00/96.37 put spds, cab ref 96.89

+2,500 SFRH6 96.12 puts, 2.0 vs 96.44/0.15%

+2,000 0QM6 96.87 straddles, 51.5 ref 96.89

+7,000 SFRZ5 96.62 calls, 0.75 vs. 96.275/0.05%

Block 5,000 SFRH6 96.62/96.81 call spds, 3.25 ref 96.42

4,200 SFRZ5 96.37/96.43 call spds ref 96.245

4,000 SFRH6 96.31/96.37 put spds ref 96.415

+1,500 0QF6 97.12/97.25 call spds 2.5 vs. 96.885/0.10%

over +10,500 SFRX5 96.18 puts, 1.0 ref 96.24/0.20%

4,500 0QZ5 96.25/96.56 2x1 put spds, 1.0 ref 96.855

+3,000 SFRU6 96.25 puts, 5

-8,000 SFRZ5 96.37 calls, 1.75

Block/screen appr 10,000 SFRZ5 96.18/96.25/96.31/96.37 call condors ref 96.24

3,000 SFRZ5 96.18/96.25 call spds, 3.5 ref 96.235

Treasury Options:

5,000 TYZ5 113.5/114 2x3 call spds, 6 net ref 112-27

-10,000 TYF6 111.5/114.5 strangles, 38

5,000 TUF6 104/104.75 strangles

-25,000 TYZ5 113.5 calls, 11

5,000 TUF6 104/104.75 strangles

Block, 40,000 FVF6 110 calls, 19.5 vs. 109-09/0.32%

+100,000 TYF6 113.5 calls, 30-32 vs. 112-18/0.32%, total volume > 158k

8,200 TYZ5 115 calls, 1 ref 112-19

appr 13,000 FVZ6 109.5/110.5 2x3 call spds vs. FVF6 108.25 puts

2,200 TYZ5 113.25/114 1x2 call spds

2,000 TYZ5 112.5/113.5 call spds

-8,900 TYF6 111 puts, 18 ref 112-12.5/0.24%

over -5,000 TYZ5 112.75 calls, 23 ref 112-16

over +20,000 wk4 TY 113.5/114 call spds, 5 vs. 112-17 to -17.5/0.10%

+10,000 wk4 TY 114/TYZ5 115 call spds, 6 net vs. 112-19/0.10%

-12,000 wk1 FV 109.25 calls, 1.5-2 vs. 109-03/0.05%

+10,000 wk4 TY/TYZ5 114 call spds, 3 net

-4,000 TYZ5 112.5/113.5/114.5 call flys, 13 vs 112-13/0.14%

+35,000 TYF6 113.5 calls, 27 ref 112-13.5/0.29%

+15,100 TYZ5 113/113.75 call spds vs. 111.75 put, 2.0 net Db ref 112-13.5

+1,900 TYZ5 113.5/115.25 1x2 call spds, 5 ref 112-17

+2,000 TYZ5 115 calls, 2.0 vs 112-21/0.05%

+1,650 FVZ5 108/108.25/108.5 put flys, 1.5 ref 109-01.5

2,000 TYZ5 112.5/114 strangles, 33 ref 112-12.5

MNI BONDS: EGBs-GILTS CASH CLOSE: Bull Flatter With BOE December Cut Teed Up

European yields pulled back Thursday in a bull flattening move.

- The session's focus was the BOE decision: the MPC held rates by a 5-4 vote. That saw an initial hawkish move in Gilts (there had been around 33% market-implied prob of a cut), but they subsequently rallied as the communications suggested it was more likely than not that Gov Bailey would vote for a December cut (he voted for a hold this time).

- For yet another session though the afternoon was dominated by US developments. Treasuries rallied amid soft US labour market data (job cuts / payroll gains/ unemployment rate via various "alternative" indicators) and fading chances of a conclusion to the federal government shutdown as the weekend approaches. Gilts and Bunds gained in sympathy.

- Global equities slumped too after edging higher early: periphery/semi-core EGB spreads edged higher as the session went on, reflecting the downward move in equities, ultimately closing wider.

- The German and UK curves both bull flattened, with Gilts outperforming.

- Friday's data slate is highlighted by German and French trade, with central bank speakers including BOE's Pill and ECB's Nagel, Villeroy and Elderson.

Closing Yields / 10-Yr EGB Spreads To Germany

- Germany: The 2-Yr yield is down 1.7bps at 1.987%, 5-Yr is down 2.3bps at 2.247%, 10-Yr is down 2.3bps at 2.65%, and 30-Yr is down 2.1bps at 3.238%.

- UK: The 2-Yr yield is down 1.8bps at 3.786%, 5-Yr is down 3.3bps at 3.897%, 10-Yr is down 3bps at 4.433%, and 30-Yr is down 3.1bps at 5.218%.

- Italian BTP spread up 1.1bps at 76.2bps / French OAT up 0.9bps at 79.4bps

MNI OPTIONS: Mixed Trade Pre/Post BOE

Thursday's Europe rates/bond options flow included:

- DUF6 107.10/107.00/106.90p ladder, bought for 1.75 in 2.5k

- DUH6 107.50c, bought for 6 in 3k

- SFIX5 96.30/96.35/96.40/96.45c condor, bought for 0.5 in 4k (post-BOE decision)

- SFIZ5 96.00/96.10/96.20/96.30c condor, sold at 4.75 in 2k

- SFIZ5 96.20/96.25/96.30c fly, bought for 1.25 and 1.5 in 7k (post-BOE decision)

- SFIH6 96.50/96.60cs, sold at 3 in 22.5k total (post-BOE decision)

MNI FOREX: Cross/JPY Slumps as US Yields & Equities Decline on Limited Weak US Data

- Both US yields and equities have fallen sharply on Thursday, reflective of the poor alternative US jobs data released (Revelio, Challenger, Chicago Fed), painting a relatively bleak picture of the US economy in the absence of the tier one figures.

- The dollar index is tracking 0.45% in the red today as the broader dollar rally that has been playing out following the FOMC is showing signs of fatigue. The DXY reaching its initial objective at the August highs (~100.25) may have also contributed to the reversal lower on Thursday.

- These dynamics have significantly boosted the Japanese Yen, a clear outperformer in the G10 FX space, while the likes of AUD and NZD have been particular laggards. AUDJPY and NZDJPY are currently down 1.4% on the session, echoing the two percent losses for the Nasdaq as we approach the APAC crossover. USDJPY has also slipped below 153.00 to new weekly lows.

- AUDJPY has not closed below its 50-day EMA since August 22, and therefore a close below 98.50 will be closely eyed. For NZDUSD (-0.60%), the pair has extended the break of trendline support (drawn from the April lows) to print fresh cycle lows below 0.5630.

- Although CAD losses are of a smaller magnitude, USDCAD notably rose back to an important level on the chart, the top of the bull channel, drawn from the July 23 low. While the resistance has held again, the pair is now on a 6-session winning streak. This week’s extension for USDCAD highlights a clear reversal of the corrective bear leg between Oct 14 - 29. 1.4167 is the next level of note, the 50.0% retracement of the Feb 3 - Jun 16 bear leg.

- An dovish hold from the Bank of England did little to move the needle for GBP, with potential positioning dynamics contributing to sterling outperformance today. Note that the cable downtrend was in oversold territory and a recovery would allow this condition to unwind. Initial resistance is at 1.3142, the Aug 1 low.

- Canada jobs data highlights the G10 calendar on Friday. Currently a -5k change in employment is expected, with the unemployment rate seen remaining steady at 7.1%.

MNI FX OPTIONS: Expiries for Nov07 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1500(E1.1bln), $1.1700(E1.0bln)

- USD/JPY: Y153.00($1.1bln), Y153.85($725mln)

- AUD/USD: $0.6500(A$1.1bln)

- USD/CAD: C$1.3900($2.3bln)

MNI US STOCKS: Late Equities Roundup: Off Lows, Energy, Utilities Health Care Gain

- Stocks remain weaker late Thursday - but are drifting off lows after the tech-heavy Nasdaq made new 1-wk lows in the first half. Trading desks cited soft employment data for the waning risk sentiment on the day.

- Revelio Labs' estimate of October nonfarm payrolls growth came in at -9.1k vs +33.0k prior (rev from +60.1k) and August's actual figure reported by the BLS of +22k (Revelio estimates Aug at +14.5k). That is the first negative M/M reading for the Revelio series since May.

- Currently, the DJIA trades down 240.53 points (-0.51%) at 47068, S&P E-Minis down 44.25 points (-0.65%) at 6779.75, Nasdaq down 266.2 points (-1.1%) at 23229.82.

- Consumer Discretionary, Communication Services and Tech sector shares continued to lead declines in late trade: DoorDash -15.92%, Paycom Software -12.24%, Tapestry -8.95%, PTC -8.49%, Robinhood Markets -8.13%, Fortinet -6.07%, Axon Enterprise -6.01%, Advanced Micro Devices -6.00% and Palantir Technologies -5.23%.

- On the positive side, Energy, Utilities and Health Care sector shares continued to lead advances:

- Texas Pacific Land +10.98%, APA +7.16%, Marathon Petroleum +5.14% and Targa Resources +4.90%

- Air Products and Chemicals +9.85%, Amcor+2.66% and Newmont +2.14%

- STERIS +7.05%, Moderna +3.23%, ResMed +1.60% and Regeneron Pharmaceuticals +1.45%.

- Expected earnings after the close include: Airbnb, Akamai Tech, Microchip Technology, Trade Desk Inc, Expedia Group Inc, Sweetgreen Inc, Take-Two Interactive Software, Block Inc, Wynn Resorts Ltd, Celanese Corp, Sandisk Corp, EOG Resources Inc and DraftKings Inc.

MNI EQUITY TECHS: E-MINI S&P: (Z5) Corrective Cycle

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6953.75 High Oct 30 and the bull trigger

- PRICE: 6816.50 @ 14:39 GMT Nov 6

- SUP 1:6748.50 Low Nov 5

- SUP 2: 6706.92 50-day EMA

- SUP 3: 6690.75 Low Oct 22

- SUP 4: 6571.25 Low Oct 17

The trend condition in S&P E-Minis is unchanged, it remains bullish and short-term weakness appears corrective. Support at the 20-day EMA, at 6805.85, has been breached. A clear break of this average signals scope for a deeper retracement and exposes the 50-day EMA at 6706.92 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

MNI COMMODITIES: WTI Edges Lower, Precious Metals Tick Up

- Crude has drifted lower today, reversing earlier slight gains amid product market strength, as oversupply concerns continue to weigh.

- WTI Dec 25 is down by 0.4% at $59.4/bbl.

- The oil market is estimated to see a surplus of 1.74mb/d this quarter, up from 400kb/d in Q3, with China restocking to slow sharply, according to ANZ, cited by Bloomberg.

- Despite the move in WTI futures today, a short-term corrective bull cycle remains in play. Initial resistance is seen at $62.59, the Oct 24 high.

- On the downside, first key support and the bear trigger is unchanged at $55.96, the Oct 20 low.

- Meanwhile, spot gold briefly rose back above the $4,000/oz level earlier today, before paring gains, with price currently just 0.2% higher at $3,986.

- From a technical perspective, the recent fresh cycle low in gold highlights an extension of the bear cycle that started Oct 20. The 20-day EMA has been breached, signalling scope for a test of the 50-day EMA, at $3,876.1, a key pivot support.

- On the upside, initial resistance is at $4,161.4, the Oct 22 high.

- Similarly, silver has pared earlier gains, with price currently 0.3% higher at $48.2/oz.

- Trend signals for silver are unchanged and remain bullish, with initial resistance at $49.456, the Oct 23 high. Support to watch lies at the 50-day EMA, at $46.241.

FRIDAY DATA CALENDAR

| Date | GMT/Local | Impact | Country | Event |

| 07/11/2025 | 0700/0800 | ** | Trade Balance | |

| 07/11/2025 | 0745/0845 | * | Foreign Trade | |

| 07/11/2025 | 0800/0300 | New York Fed's John Williams | ||

| 07/11/2025 | 1110/1110 | BOE Saporta At ECB Money Market Conference | ||

| 07/11/2025 | 1200/0700 | Fed Vice Chair Philip Jefferson | ||

| 07/11/2025 | 1200/1200 | BOE Market Participants Survey | ||

| 07/11/2025 | - | *** | Trade | |

| 07/11/2025 | - | BOE MPG Agenda Published | ||

| 07/11/2025 | 1330/0830 | *** | Labour Force Survey | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/0830 | *** | Employment Report | |

| 07/11/2025 | 1330/1430 | ECB Elderson At Bundesbank Event | ||

| 07/11/2025 | 1500/1000 | ** | University of Michigan Surveys of Consumers Inflation Expectation | |

| 07/11/2025 | 1500/1000 | *** | U. Mich. Survey of Consumers | |

| 07/11/2025 | 1515/1515 | BOE Pill At National Agency Briefing | ||

| 07/11/2025 | 1600/1100 | ** | NY Fed Survey of Consumer Expectations | |

| 07/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 07/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 07/11/2025 | 1800/1300 | ** | Baker Hughes Rig Count Overview - Weekly | |

| 07/11/2025 | 2000/1500 | * | Consumer Credit | |

| 07/11/2025 | 2000/1500 | Fed Governor Stephen Miran |