EQUITY TECHS: E-MINI S&P: (Z5) Corrective Cycle

- RES 4: 7000.00 Psychological round number

- RES 3: 6993.12 3.500 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 2: 6974.04 3.382 proj of the Aug 20 - 28 - Sep 2 price swing

- RES 1: 6953.75 High Oct 30 and the bull trigger

- PRICE: 6816.50 @ 14:39 GMT Nov 6

- SUP 1:6748.50 Low Nov 5

- SUP 2: 6706.92 50-day EMA

- SUP 3: 6690.75 Low Oct 22

- SUP 4: 6571.25 Low Oct 17

The trend condition in S&P E-Minis is unchanged, it remains bullish and short-term weakness appears corrective. Support at the 20-day EMA, at 6805.85, has been breached. A clear break of this average signals scope for a deeper retracement and exposes the 50-day EMA at 6706.92 - a key pivot support. The bull trigger has been defined at 6953.75, the Oct 30 high. Clearance of this hurdle would confirm a resumption of the uptrend.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Businesses Face Tough Decisions But Not Indicative of Recession - Bostic

Q: When does caution on a mass scale tip us into recession?

Bostic: "No one thinks that catastrophe is on the horizon. There was a lot of fear that emerged when the high levels of tariffs were first introduced. Today, businesses say the catastrophic outcomes have been taken off the table. There are still a bunch of tough ones, but not catastrophic to the level that would lead to something that would suggest there's going to be a recession. On the other hand, I would say there's always the possibility that disruptions, that concerns that can lead to extreme retrenchment like that. It could instead be saving a little more, going out to dinner one less time, or doing a driving rather than flying vacation. And we actually see that in the economy today, particularly at the lower end of the income and wealth distribution, that precautionary activity is taking place (consumers substituting labels, choosing products that can be rationed out more). We're seeing those sorts of changes, which is a sign that there is definitely stress among a set of families and the set of families for which that stress is, is happening, mainly because the price challenges, um, is migrating. But at the same time, there are still lots of families that have a lot of affluence, and they actually drive that second category."

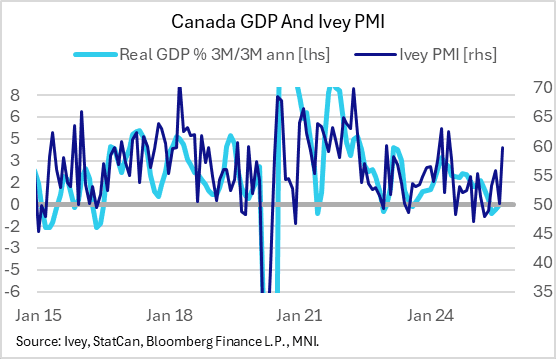

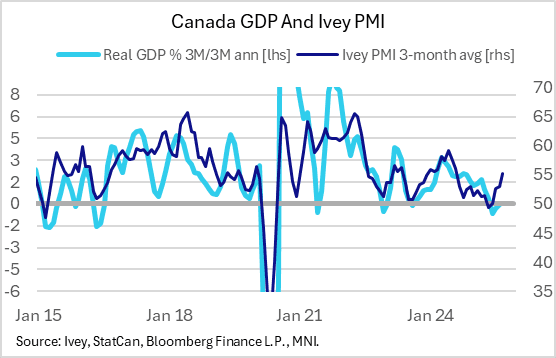

CANADA DATA: Ivey PMI Points To Pickup In GDP Momentum At End Of Q3

The Ivey Purchasing Managers Index soared to 59.8 in September from 50.1 in August, for easily the strongest reading since June 2024.

- The headline index represents responses to a single question ("Were your purchases last month in dollars higher, the same, or lower than the previous month?") and suggests solid growth in September.

- But meanwhile the other indices were mixed. The biggest standout was inventories jumping to 56.4 - the highest since October 2022 - after 49.5 in September. The employment sub-index rose to 50.2 from 46.0 (just a 2-month high), with supplier deliveries at a 3-month low 46.4 (47.0 prior; indicating slower deliveries). And the prices gauge moderated for a 3rd consecutive month, to a 9-month low 63.2 from 65.1 prior, suggesting some relief in trade war-related price pressures.

- With the monthly headline index being so volatile, we take more signal from the 3 month moving average which rose to a 13-month high 55.2.

- Historically would suggest a pickup in the quarterly rate of GDP (monthly industry GDP showed 0.2% growth in July, with the StatCan advance for August at 0.0%).

FED: Bostic Touts Atlanta Fed's Survey Network

Atlanta Fed’s Bostic (non-voter) in a moderated discussion, touting the bank’s surveys including its CFO survey and unstructured regional economic information network (in response to a question hinting at government shutdown data issues).

- "I feel like I got lucky that I got to be the Atlanta president because our bank, long before I got here, had decided that the federal statistics weren't enough for us to really understand what's going on in the economy. Basically all the federal statistics are backward looking. And we know through history there have been times when there have been big turns in the economy and people in our building were quite surprised by that. And so we decided that we need to supplement this federal statistics with information from other sources."

- "And so we have our survey center, and we do a bunch of surveys of businesses to try to get information about. For example, we survey CFOs and ask what's your hiring plan for the next 12 months? What's the likelihood you'll reduce prices in the next quarter to get some forward looking idea about what business, what actual decision makers are doing? And I will say in the survey side, we found that what people say they do, they actually wind up doing. And so it winds up being useful and predictive in ways that give me a sense of what the trajectory of the economy will be."

- "And then we have a third source, which is our regional economic information network. We basically pay a bunch of folks to have unstructured conversations with business leaders, 90 minutes to 2 hours. The unstructured nature is actually quite helpful because it creates space for new ideas to come up, things that we may not be seeing in the newspaper that can give us insights. And so over the course of an FOMC cycle, we'll talk to somewhere between 60 and 120 folks. And we try to do different size of businesses, different sectors, all that kind of stuff."

- Separately on AI: "For the last 18 months, maybe until about 3 or 4 months ago, it was like, yeah, we're dabbling in [AI]. We're going to try to find ways to try to understand it and see possibilities, but it's not anywhere that's critical. Today, everybody has it in some business process, and everyone is trying to think about ways they can get it to be even more productive or more useful in those processes. When I talk to CEOs, they see AI as more a labor complement than a labor replacer.