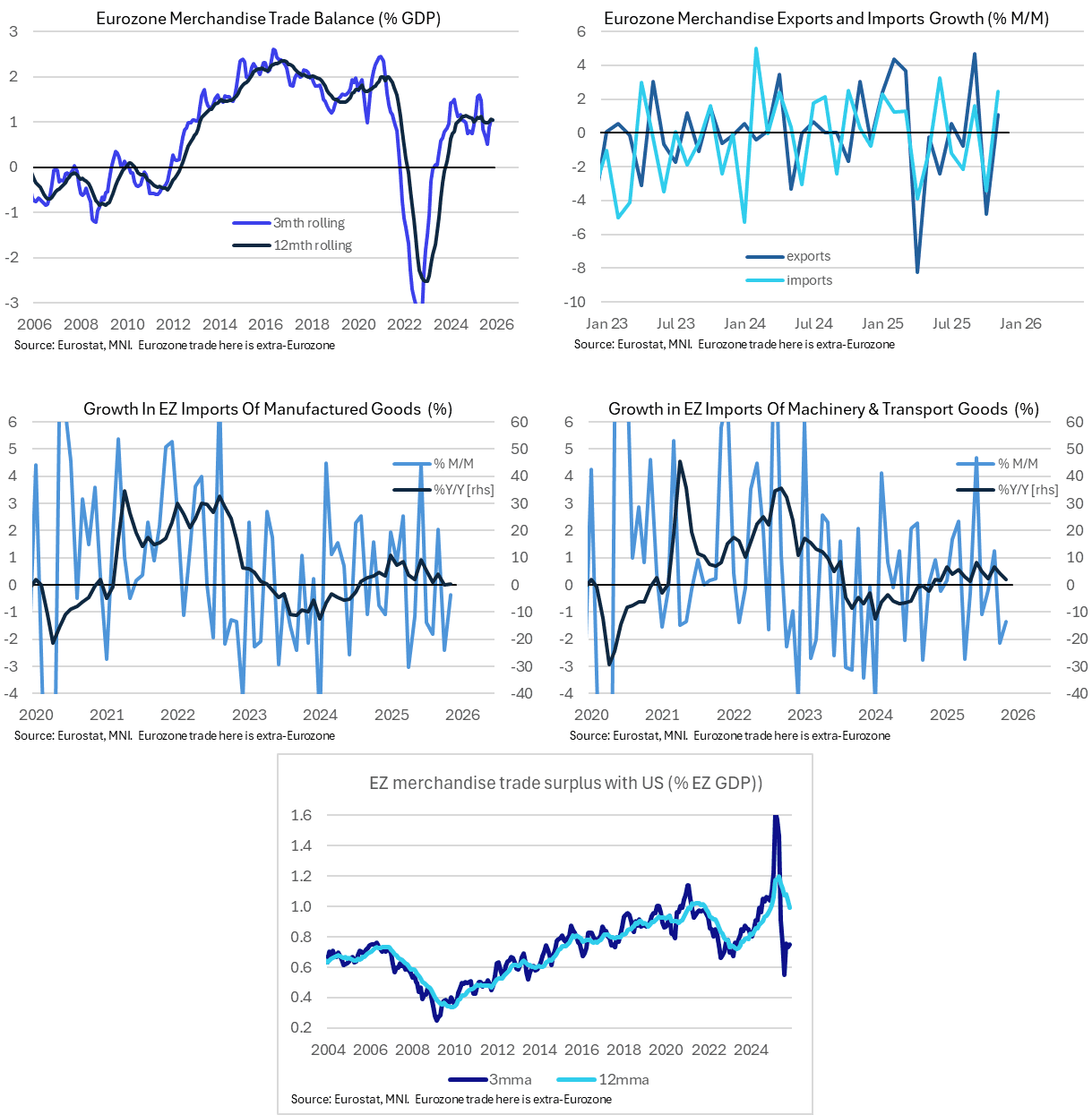

EUROZONE DATA: Merchandise Trade Has Been Resilient In The Face Of US Tariffs

- The Eurozone seasonally adjusted trade balance eased to E10.7bln in November, down from E13.7bln prior. Trade volumes partially rebounded on both the export (1.1% M/M vs -4.8% prior) and import (2.5% M/M vs -3.4% prior) side. Zooming out, this leaves the 3mth trade surplus at 1.1% of GDP, a six month high after 1.0% in October and 0.9% in September. On a rolling 12mth comparison, the surplus was also 1.1%, and has been broadly steady at this level since Q2 2024. Overall, this chimes with ECB rhetoric that the economy has shown relative resilience in the face of US tariffs.

- Eurozone extra-regional exports were down 1.1% Y/Y in November, though this has been offset by a 1.8% Y/Y rise in intraregional trade. The US has of course been the focus on the extra-regional export side, and the 19.7% Y/Y fall highlights the direct impact of President Trump’s tariff regime. US exports in the 12 months to November were worth 1.0% of Eurozone GDP, down from 1.2% at the start of this year amid the well-documented tariff front-running dynamic.

- Elsewhere, imports of manufactured goods and machinery and transport goods were once again negative in November. This left Y/Y rates just barely positive. As always, we recommend caution with interpretation here as the 150% M/M rise in the “miscellaneous” category will be distributed across product categories in subsequent revisions.

- Imports from China were up 4.5% Y/Y (vs 3.6% prior), We’ve written extensively in recent days that China’s exports remain highly competitive, with increased penetration a still key risk facing Eurozone manufacturers - and the broader inflation outlook.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

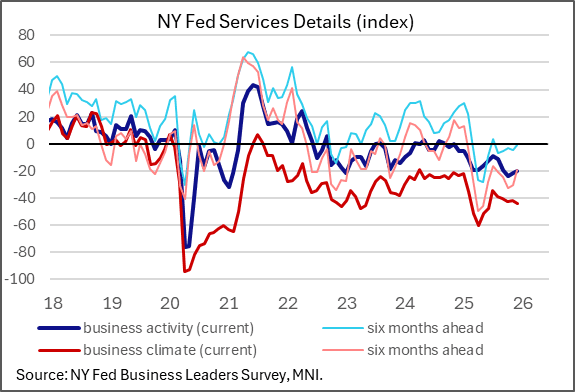

US DATA: NY Fed Services Activity Stays Weak At Year-End, With Prices A Concern

The New York Fed's monthly regional services firm (aka "Business Leaders") survey showed continued weak activity in December, with a notable pickup in price pressures. As the first of the monthly regional Fed services surveys, as with the prior day's Empire manufacturing report, it suggested little cause for cheer over economic developments at end-year.

- The general activity index ticked up to -20.0 from -21.7, but this is firmly negative and little changed over the last 4 months (the report describes the upshot as "activity continued to decline significantly"). Likewise, the business climate index at -44.2 (-42.2 prior) remained sub -40 for a 4th consecutive month, though the latest reading was narrowly a 6-month worst.

- Among the details: capex spending was steady at weak levels, employment fell for a 4th consecutive month amid weak wage growth, and supply availability continued to worsen. Confidence improved marginally (echoing the Empire Manufacturing survey), with the 6-month general outlook of -1.1 the 2nd best of the year (-4.6 prior).

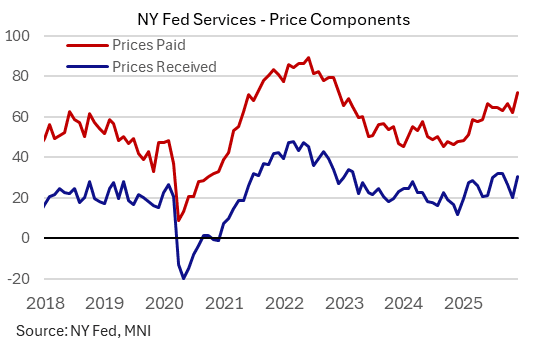

- The prices paid gauge however was an inflationary warning sign, jumping over 10 points to 72.1 for a post-2022 high. Expected prices paid edged down 1.7 points to 63.2 but remained above 60 for a 10th straight month.

OPTIONS: Expiries for Dec17 NY cut 1000ET (Source DTCC)

- EUR/USD: $1.1700(E1.3bln), $1.1750(E1.5bln), $1.1800(E1.6bln), $1.1850(E624mln)

- USD/JPY: Y154.75($594mln)

- AUD/USD: $0.6590(A$680mln), $0.6650-60(A$875mln)

EU: No Sign Of Agreement On Use Of Frozen Russian Assets Pre-EUCO

The chances of an agreement being reached within the EU on the use of frozen Russian assets held in the Union to fund 'reparations loans' for Ukraine in time for sign-off at the 18 Dec EUCO summit appear to have evaporated. On 15 Dec, Belgium once again rejected Commission overtures regarding legal and financial guarantees. EU ambassadors meet today to further discuss the plans.

- Politico reports as part of the concessions, "...Belgium could tap into as much as €210 billion if it faces legal claims or retaliation by Russia [...]. It also stated that no money should be given to Ukraine before EU countries provide financial guarantees covering at least 50 percent of the payout. In a further concession, the Commission instructed all EU countries to end their bilateral investment treaties with Russia to ensure Belgium isn’t left alone to deal with retaliation from Moscow."

- The article claims that Belgium continues to view the plans as not being watertight and risking leaving it alone if Russia comes to claim the funds.

- The Commission has raised an alternative plan: joint debt issuance to fund Kyiv from the end of Q126. Italy, Malta, Bulgaria and Czechia are all backing Belgium's call for this option to be examined.

- Germany has advocated more strongly for the frozen asset seizure option, but critics argue this is more to do with opposition to EU debt issuance in Berlin than believing it will be a workable plan. The 18-19 Dec EUCO risks becoming a bitter meeting if no agreement is possible.