EUROZONE DATA: May Manufacturing PMI: Mixed Export Orders Across Countries

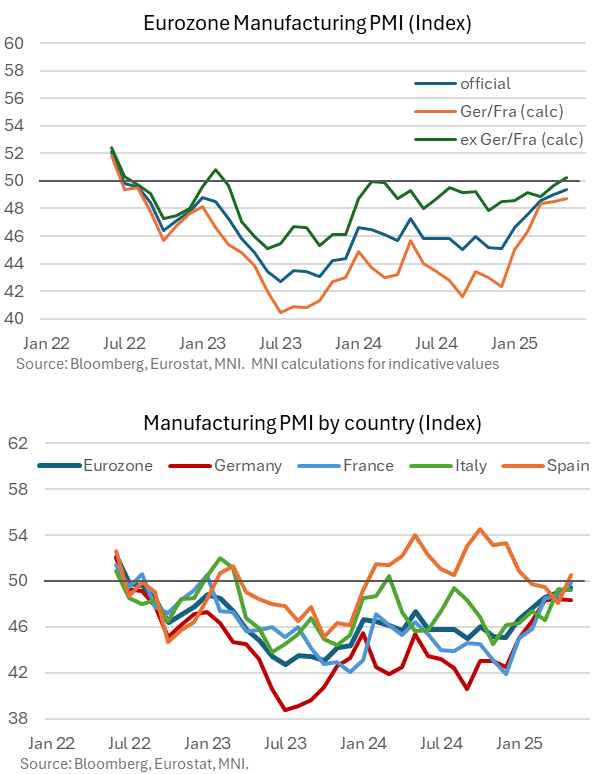

The Eurozone May manufacturing PMI confirmed flash estimates at 49.4 (vs 49.0 prior), with an upward revision in France offset by a downward revision in Germany. The stronger-than-expected Spanish data was also countered by a slightly softer-than-expected Italian reading. The Eurozone index has improved consistently through this year, despite the imposition of and associated uncertainty from US tariffs. It's reasonable to assume that ECB rate cuts are having a positive impact here.

- We estimate the Germany/France combined manufacturing PMI at 48.7 (vs 48.5 prior), while the ex-Germany/France reading was 50.3 (vs 49.6 prior), the first expansionary reading since March 2023.

On export orders: "Sales made to customers in export markets came close to stabilising, with the respective HCOB index posting a 38-month high that was only just below the neutral 50.0 level".

- Germany: "After returning to growth for the first time since early 2022 in April, international sales rose at a slightly accelerated rate in May, albeit one that was still only modest overall. A number of surveyed businesses reported stronger demand across Europe, while there were also several mentions of increased sales to the US, linked in part to customers stockpiling ahead potential tariff increases".

- France: "New export sales exerted a slightly sharper drag on total new work during May, although the drop in overseas demand was mild".

- Italy: "Despite the backdrop of tariff uncertainty, export sales increased in the latest survey period. Although the uptick was only marginal, it was the first recorded in over two years. Panellists linked the rebound to a rise in orders from European customers".

- Spain: "New export orders fell to a much lesser degree. Several panellists noted a relative improvement in European and US demand, albeit still characterised by some hesitation in committing to new work amid the uncertain tariff outlook".

On prices: "Input costs decreased for a second month in a row during May. Furthermore, the rate of decrease was the quickest in 14 months. There was evidence of companies passing on cost savings to their clients as output charges were discounted for the first time since February".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

USDCAD TECHS: Hits Bear Trigger, New Cycle Low

- RES 4: 1.4415 High Apr 1

- RES 3: 1.4296 High Apr 7

- RES 2: 1.4087 50-day EMA

- RES 1: 1.3906/3935 High Apr 17 / 20-day EMA

- PRICE: 1.3793 @ 17:00 BST May 2

- SUP 1: 1.3760 Low Apr 21 and the bear trigger

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 2024

- SUP 4: 1.3643 Low Oct 9 ‘24

The trend set-up in USDCAD deteriorated further Friday, with prices slipping through the bear trigger to narrow the gap with next support. The fresh cycle low reinforces the bear cycle and signals scope for a continuation near-term. Potential is seen for a move towards 1.3744, a Fibonacci retracement. Moving average studies are in a bear mode position, highlighting a dominant downtrend. First resistance to watch is 1.3943, the 20-day EMA.

AUDUSD TECHS: Consolidation Phase

- RES 4: 0.6550 61.8% retracement of the Sep 30 ‘24 - Apr 9 bear leg

- RES 3: 0.6528 High Nov 29 ‘24

- RES 2: 0.6471 High Dec 9 ‘24

- RES 1: 0.6470 High May 2

- PRICE: 0.6445 @ 16:59 BST May 2

- SUP 1: 0.6344/6316 Low Apr 24 / 50-day EMA

- SUP 2: 0.6181 Low Apr 11

- SUP 3: 0.6116 Low Apr 10

- SUP 4: 0.5915 Low Apr 9 and key support

AUDUSD remains inside a consolidation phase, having traded either side of the 0.6400 level for 10 consecutive sessions. The underlying trend remains bullish and the pair is trading close to recent highs. Price has recently breached a key resistance at 0.6409, the Dec 9 ‘24 high. This breach reinforces bullish conditions and signals scope for a continuation higher near-term. Sights are on 0.6471 next, the Dec 9 2024 high. Initial key support to monitor is 0.6316, the 50-day EMA. A clear break of this EMA would be a concern for bulls.

US TSYS: Rates Retreat, Sentiment Improved Though Trade Risk Remains

- Treasuries look to finish near late Friday session lows after trading firmer on the open, higher than expected Nonfarm payrolls at 177k (sa, cons 138k) of which private contributed 167k (sa, cons 125k) triggered the early reversal.

- However, two-month revisions of -58k offset the 39k beat for nonfarm payrolls, with a similar story for private (a 42k surprise vs -48k two-month revision).

- Stocks are back near four week highs - pre-"Liberation Day" levels as hopes of some trade deal being made improved sentiment.

- The Wall Street Journal reports that "Beijing is considering ways to address the Trump administration’s gripes over China’s role in the fentanyl trade... potentially offering an off-ramp from hostilities to allow for trade talks to start." The Journal notes that "discussions remain fluid" and China "would like to see some softening of stance from President Trump".

- Currently, the Jun'25 10Y contract trades -20 at 111-07.5 vs 111-02 low -- initial technical support (50-dma) followed by 110-16.5/109-08 (Low Apr 22 / 11 and the bear trigger). Curves bear flattened, 2s10s -3.480 at 48.002, 5s30s -4.911 at 86.807.