EU TRANSPORTATION: Lufthansa; buy out remaining of ITA (Corriere) (x2)

(LHAGR: Baa3/BBB-/BBB-)

Reminder the LHAGR 3.5% 29s is NOT a retail bond. It is well tight on RV; new IAG 30s is also IG and a firmer name, gives +22bps for the 1yr extension.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

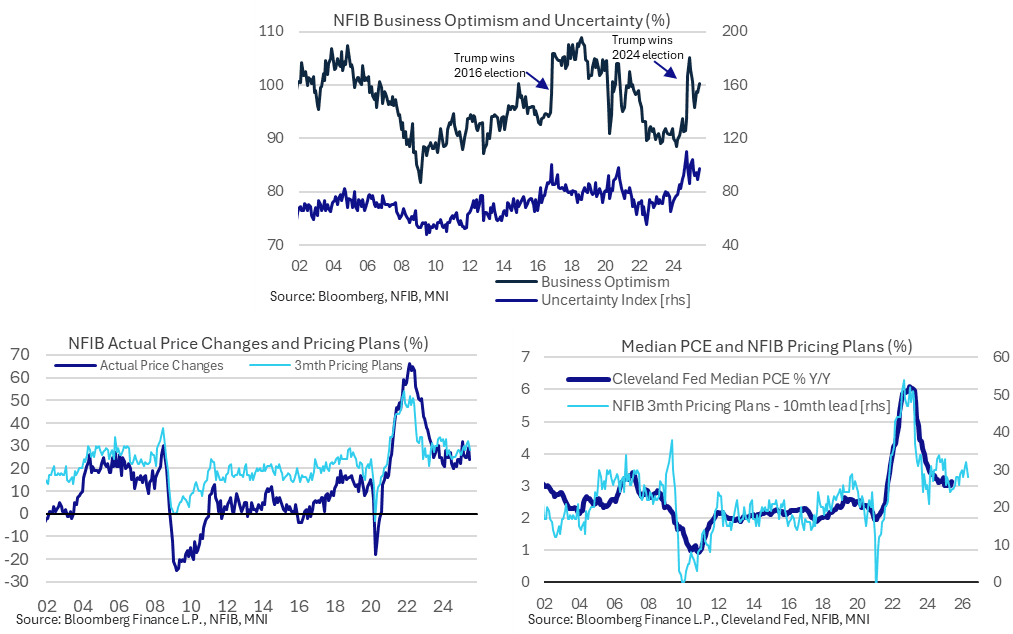

US DATA: NFIB Small Business Price Plans Cool

The NFIB small business index was stronger than expected in July despite weakness in the already published jobs details. Notably despite this slightly firmer backdrop, price plans cooled rather than accelerating further.

- The NFIB small business index was higher than expected in July as it increased to 100.3 (cons 98.9) after 98.6 in June for a five-month high.

- The 100.3 compares with the April low of 95.8 on the announcement of reciprocal tariffs, a high of 105.1 in December fully reflecting US election results and an average of 93 in 2024. The series has a very long-term 52-year average of 98.

- Impressively, seeing as the already published jobs report had shown multiple points of weakness in July, six of the ten components for this broader index improved.

- A net 36% of owners expect better business conditions, +14pps from a month earlier and the most this year. A net 16% said now is a good time to expand their business, the largest share since January.

- Ahead of today’s US CPI report for July, price plans remain relatively elevated but contained, and with some moderation compared to May and June levels.

- Specifically, a net 24% increased prices over the past three months vs 29% in June and a recent high of 32% back in February. This is in line with the 23% average seen in 2024 but remains above pre-pandemic averages of ~12%.

- A net 28% expects to increase prices over the next three months vs a recent high of 32% in June. It’s in line with the 28% averaged in 2024 but remains above the 22% averaged pre-pandemic.

- As such, it’s still pointing to some stabilization in inflation at above-target rates but the pace hasn’t accelerated further as might have been seen if small firms were planning to increasingly pass on tariff cost increases.

FOREX: GBP Crosses Contained By Technical Parameters; Focus On US CPI

Sterling has been relatively insulated from the light upside pressure in Gilt yields over the last ~60 minutes, with important technical parameters containing intraday ranges in several GBP/XXX crosses. This morning’s labour market report has set the tone for GBP today. The data was on balance stronger-than-expected, but there remain signs that overall conditions are still easing.

- EURGBP is down 0.3% today, troughing at 0.8621 and importantly leaving the 50-day EMA at 0.8612 untested. A clear break of this average would strengthen a bear threat, and expose the June 30 low at 0.8540.

- Yesterday’s highs of 1.3477 have contained upside in GBPUSD today, with cable currently up 0.2%. Short-term momentum is nonetheless pointed higher, with the Jul 24 high of 1.3589 the next notable upside level. Focus remains sharply on this afternoon’s US CPI report. We see more sensitivity to a downside surprise in July CPI, particularly in core goods components seen sensitive to tariffs. If realised, this could provide fresh upside impetus for cable.

- In the crosses, the psychological 200.0 handle has once again provided strong resistance in GBPJPY. The current trend set-up remains bullish however, with the cross currently on course for a sixth consecutive positive session and moving average studies operating in a bull-mode setup.

US TSYS: Little Changed Ahead Of CPI Report

- Treasuries are near unchanged across the curve ahead of the July CPI report (MNI CPI Preview).

- Cash yields are 0-0.5bp lower on the day across the curve, with 2Y yields at 2.768% hovering around a 38.2% retrace of the slide from 3.95% to 3.655% on the July payrolls report from Aug 1.

- TYU5 trades at 111-25 (-03+) on another thin session for overnight volumes nearing a cumulative 200k. The overnight low of 111-23 takes it a little further away from resistance at 112-15+ (Aug 5 high) whilst support isn’t seen until 110-19+ (Jul 24 low).

- Data: CPI Jul (0830ET), Real av earnings Jul (0830ET), Federal budget bal Jul (1400ET)

- Fedspeak: Barkin (1000ET), Schmid (1030ET) - see STIR bullet

- Bill issuance: US Tsy to sell $85B 6-W bills (1130ET)

- Politics: White House Press Secretary Leavitt Briefing (1300ET). A limited public schedule for President Trump but with post-CPI remarks watched after his extraordinary termination of BLS’s McEntarfer after this month’s weak payrolls report.