GERMANY: Light Downside In Bund Futures As Bundestag Approves Defence Package

Bund futures took a small leg lower on confirmation that the Bundestag has approved a defence procurement package worth E50bln. Bunds currently -15 ticks at 127.41, with yesterdays 127.33 low untested today.

This wasn't a surprise though, the FT reported this morning that "Germany’s parliament is set to agree to more than €50bn in military purchases on Wednesday, rounding off a bumper year as the EU’s largest nation ploughs ahead with a vast rearmament."

"Members of the Bundestag’s budget committee, which has the power to block or approve all significant weapons purchases, have been asked by officials to sign off on projects including a €21bn order for clothing and protective equipment for soldiers, according to documents seen by the Financial Times."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

SONIA OPTIONS: Call Condor buyer

SFIH6 96.40/96.50/96.60/96.70c condor, bought for 3.25 in 3k.

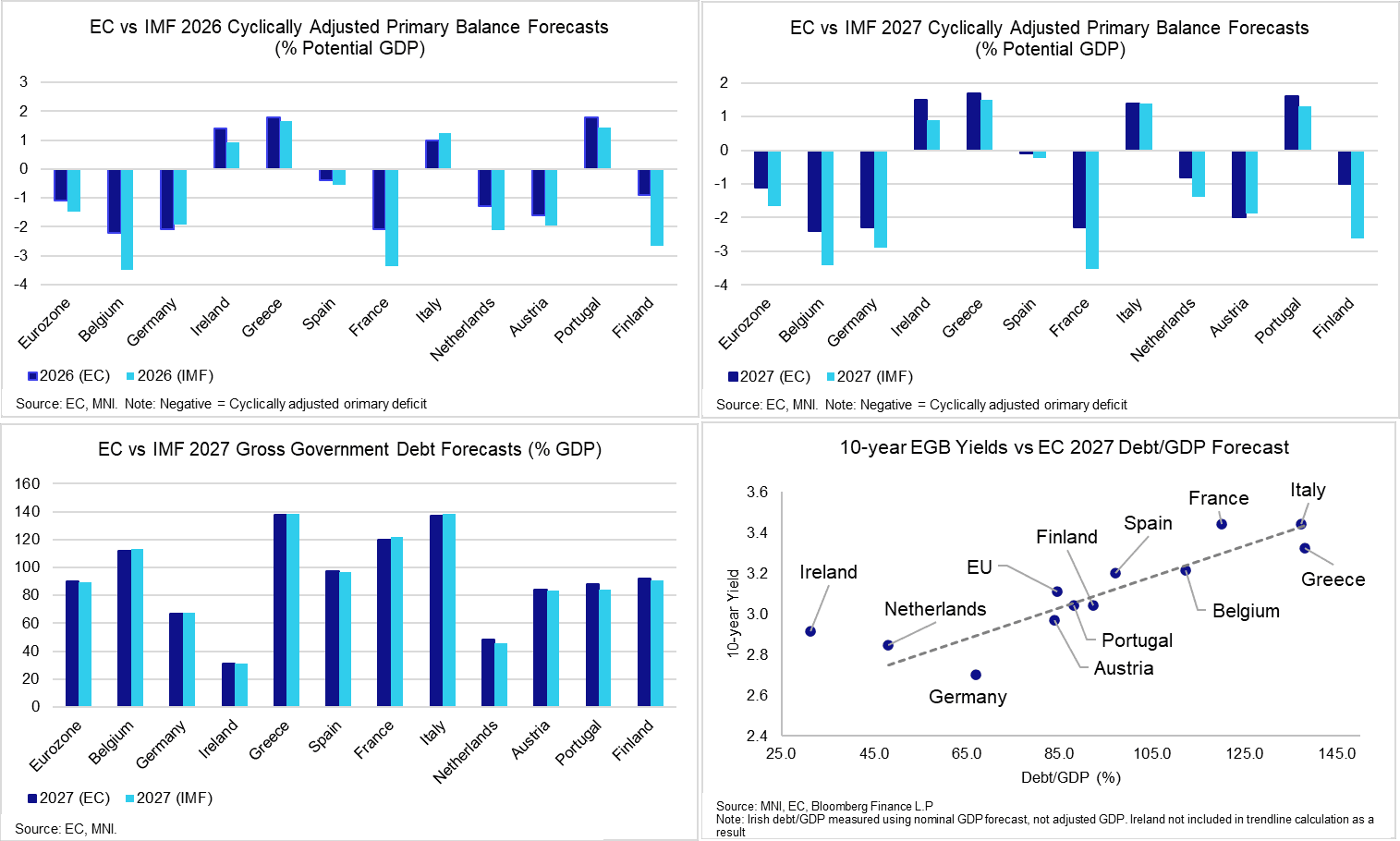

MACRO OUTLOOK: EC More Optimistic On FR/BE Fiscal Consolidation Than IMF

- Plotting current 10-year yields against the EC’s 2027 debt/GDP projections, France and Germany have the largest deviation from the trendline (we exclude Ireland from this analysis as the EC/IMF don’t project adjusted GDP, only total nominal GDP).

- For Germany, this likely reflects 10-year Bund’s safe haven properties. In the case of France, we interpret it as a crude estimate of political risk premium – currently around 15bps.

- Relative to the IMF’s latest Fiscal Monitor, the EC’s Autumn forecasts appear to embed more front-loaded German fiscal easing. The EC projects a slightly larger cyclically adjusted German primary deficit in 2026 than the IMF, but a smaller deficit in 2027 (see charts).

- The EC is more optimistic than the IMF on fiscal consolidation in some countries. 2026 and 2027 cyclically adjusted primary deficits in Belgium and France are visibly larger in the IMF’s Fiscal Monitor than in the EC's forecasts.

- Overall though, 2027 debt/GDP projections from both institutions are quite similar across countries.

SWAPS: Long End UK Spreads Comfortably Off Cycle Lows Despite Tax Rate U-Turn

Although markets have demanded higher gilt yields after press reports signalled an income tax rate hike u-turn from Chancellor Reeves, long-dated UK swap spreads remain some distance off their respective year-to-date/cycle lows.

- There are several counter points to consider here:

- Cross-market impulses, with long end U.S. & German spreads off cycle lows. Markets were also dealing with U.S. “Liberation Day” turbulence (which pressured U.S. swap spreads) and the German “whatever it takes” fiscal moment (which pressured German swap spreads) around the time of April’s sell off in UK swap spreads.

- The DMO & BoE have been nimble when it comes to shortening the WAM of supply, which has alleviated pressure for long end gilts on several occasions. There are expectations for an ongoing skew away from long end issuance.

- The UK is further along the disinflationary path than it was back in April.

- While income tax rate hikes have seemingly been scrapped, the fiscal stance is still expected to tighten in next week’s Budget. Outside of the pure fiscal implications, the Budget is set to hamper economic growth, which could expedite further BoE easing.

Fig. 1: UK 10- & 30-Year Swap Spreads (bp)

Source: MNI - Market News/Bloomberg Finance L.P.