ECB: Lagarde: MonPol Transmission Is Effective And On Time

Lagarde and Panetta answer two questions on Italian banks (and the proposed banking tax) and the digital euro.

Q: Transmission of monetary policy is usually six nine months, something like that. Your last cut was roughly four months ago, and yet monetary, monetary condition did tighten a little bit. Are you worried that transmission is hindered somehow, and therefore you're maybe not such in such a good place? Or can you just describe what do you think of the transmission?

A: "It's always more fashionable to make negative comments whenever you have good news. That I understand, but when we have some good news, we have to also acknowledge and draw the consequences and see what impact it has, because as I said repeatedly and as we are driven by data".

- "We maintain this three pronged approach that we have had to take into account inflation outlook, underlying inflation and transmission of monetary policy. And I would add to that, you know, since our strategy review, in addition to pure inflation outlook and the identification of our baseline, we also try to identify and measure risks to the baseline risk to the upside risk to the downside and we use different tools in order to do so, including scenario analysis"...."Everything that we see in terms of transmission leads us to believe that transmission is effective, is very much on time. The numbers that we see in terms of interest rates charged to corporates, interest rates charged to mortgages, lead us to believe that that transmission is not impaired at all, but is functioning well".

- "We have seen two things in the BLS. I) There has been a slight tightening of the credit terms by the banks, which was unexpected, and that is, in our view, and on the basis of their response to our survey, caused by the more attentive measurement of risk of their customers, particularly in the corporate sector. II) On the one hand, household interest rates have not budged at 3.3%. And on the other hand, the volume off loan to households eyes itself, increased, but again, we observe on the part of the banks based on the bank lending surveys, a more cautious attitude".

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FED: Boston's Collins: Limited Further Easing Possible By Year-End

Boston Fed President Collins (2025 FOMC Voter) says in a speech Tuesday (link) that "it may be appropriate to ease the policy rate a bit further this year – but the data will have to show that". This indicates that she may not be one of the 9 FOMC members at the median 3.6% dot seen in the latest SEP projections. Instead she may only see one further cut this year (there are two of 19 members in that camp). To take a literal interpretation, Collins says it may be appropriate to ease "a bit further" this year; having described the September 25bp cut as "a bit of easing", so it would stand to reason she is referring to 25bp moves in both instances.

- This would be 25bp more easing in 2025 than she saw as recently as July, when she said that one rate cut by year-end would likely be appropriate. Subsequently at Jackson Hole, she said “it is not a done deal in terms of what we do at the next meeting. But a range of possibilities is on the table and we are going to get more data between now and then."

- She supported the 25bp September cut because "in my view, a bit of easing was appropriate to address the recent shift in the balance of risks to our inflation and employment mandate. But I continue to see a modestly restrictive policy stance as appropriate, as monetary policymakers work to restore price stability while limiting the risks of further labor market weakening."

- Collins's "baseline outlook continues to be relatively benign. I anticipate hiring will pick up as firms adjust to the new tariff environment. And while inflation is likely to remain elevated into next year, I expect it to resume its gradual return to target over the medium term. This outlook is similar to the median forecast in the September Summary of Economic Projections (SEP)." Note that the latest PCE medians were: 3.0% 2025, 2.6% 2026, 2.1% 2027.

- But "in this highly uncertain environment, I do not rule out scenarios featuring higher and more persistent inflation, more adverse labor market developments – or both. Still, with less scope for inflationary pressures from the labor market, the upside inflation risks I was concerned about a few months ago are more limited."

- On the labor market she says "Anemic job gains amid solid economic growth are a somewhat puzzling combination." In Q&A she elaborates, saying "there's a lot of different indicators that I think make it quite clear that the labor market has softened... at the same time, there are a number of indicators that indicate what you might call a kind of curious type of balance" so assessing the incoming data will be key to "understand how labor supply and labor demand are evolving."

- She says in Q&A re inflation that "while I do expect tariffs to continue feeding through, I'm no longer expecting as large an impact as I had some months ago."

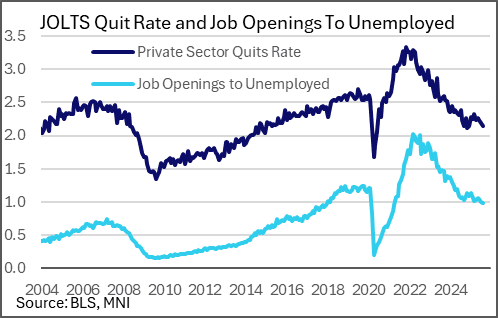

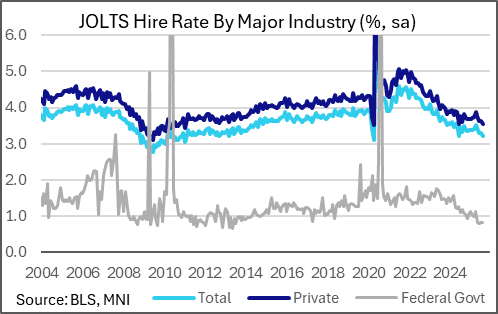

US DATA: JOLTS Reaffirms "Low Hiring, Low Firing" Labor Market Narrative

Job openings were relatively steady in August in the latest JOLTS report, totaling 7,227k (SA, vs 7,200k consensus) with July's slightly upwardly revised to 7,208k (from 7,181k). But secondary metrics suggested further loosening in labor market conditions, and while there was no marked deterioration in the month, overall the report bolstered the prevailing "low hiring, low firing" narrative.

- The first was the ratio of openings to the number of unemployed, which fell to 0.98 from 1.00 - lowest and first time below 1.0 since April 2021 (July's held that title, but was revised up from 0.99).

- The second was the quits rate, which fell to a 9-month low 1.9% (the number of quits fell to 3,091k vs 3,165k consensus - from 3,166k prior rev from 3,208k). The private sector quits rate dipped to 2.1% for the first time in 8 months, from 2.2% (we calculate at 2.14% from 2.20%). The rate dropped or was steady across the vast majority of sectors, with a fall in leisure and hospitality quits (3.3%, lowest in over a decade, from 4.2% prior) standing out in particular as this had been one of the hottest pandemic-reopening sectors.

- The third was a further deterioration in the hiring rate, at 3.21%, down from 3.28%. Excluding the pandemic-hit April 2020, that's the lowest hiring rate since September 2012. The private sector hiring rate is just 3.53%, with the government hiring rate of 1.36% (0.82% federal) both around the lowest in a decade or more (ex-pandemic).

- The fourth, in the "low firing" department, the level of layoffs was relatively tame at 1,725k, down from 1,787k prior for a 3-month low and well below the rise to 1,827k expected, keeping the layoffs rate steady at 1.1%.

- The vacancy rate ticked up very slightly (to 4.33% from 4.32%).

EUROPEAN INFLATION: Eurozone inflation tracking 2.2-2.3%Y/Y

- Ahead of tomorrow's flash Eurozone HICP print, we track the Y/Y print at 2.2-2.3%Y/Y.

- This is broadly in line with consensus. The median estimate in the Bloomberg survey is 2.2%Y/Y but 20/44 analysts in the survey look for 2.3% (or higher).

- We have so far received data from countries that make up 83.1% of the index.