GERMAN DATA: Labour Market Overall Shows Weakness

Feb-28 11:16

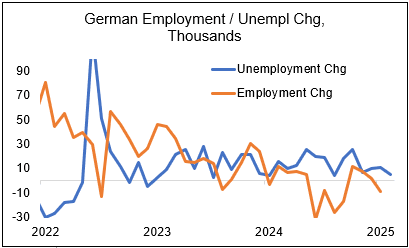

Latest German labour market data showed broad economic weakness continued to filter through. Employment fell while unemployment rose according to the latest data, and labour demand appears to have declined. The outlook remains weak, with the IFO employment barometer in February reversing its Jan bump, remaining clearly in contractionary territory at a 93.0 index value.

- Employment declined on a seasonally adjusted basis by 9k in January vs +2k in December, its first decline since September.

- More timely unemployment data for February also increased although it was admittedly by less than expected at 5k (14k cons) after 11k in January on a seasonally-adjusted basis, and last saw a smaller increase in Aug and Jan 2024 (both with 4k).

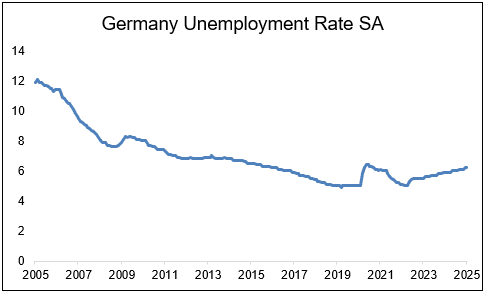

- The unemployment rate meanwhile remained at 6.2% as expected - it has been on a broader uptrend since early 2022.

- The expected number of employees impacted by 'Kurzarbeit' (which can be interpreted as an early indicator for future use of state benefits) was broadly stable in February vs Jan (to 54k Feb through 1st-24th) although it can be volatile.

- Labour demand, reflected by the employment agency's seasonally-adjusted job index "BA-X", fell in February by 2 points to 103. That's down 11pts since Feb 2024 and an all-time high of 138 in May 2022 (the index is normalised to 2015=100 and reflects vacancy levels and activity).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURIBOR OPTIONS: Call Condor vs Put Spread

Jan-29 11:15

ERM5 97.875/98.00/98.125/98.25c condor vs 97.5625/97.4375ps, bought the condor for 0.75 in 2k.

SONIA: Call fly seller

Jan-29 11:11

SFIM5 96.00/96.50/97.00c fly sold at 4.5 down to 4.25 in 2.5k.

OPTIONS: Expiries for Jan29 NY cut 1000ET (Source DTCC)

Jan-29 11:10

- EUR/USD: $1.0400(E918mln), $1.0420-30(E1.2bln), $1.0450(E668mln), $1.0500(E1.3bln)

- USD/JPY: Y154.00($627mln), Y154.75($700mln), Y155.00($1.4bln), Y156.00($544mln)

- USD/CAD: C$1.4500($1.1bln)

- USD/CNY: Cny7.2800($600mln)