ECB: June Projections: Scenario Analysis Provides Little Steer For Markets

As promised, the June projections contain a scenario analysis of “US tariffs and trade policy uncertainty” in Box 2. The analysis solely assesses the reactions of GDP and inflation, so does not give any guidelines/heuristics on the potential policy response. As such, while a useful tool to benchmark incoming data over the next few quarters, the signal from the scenario analysis for markets feels quite limited.

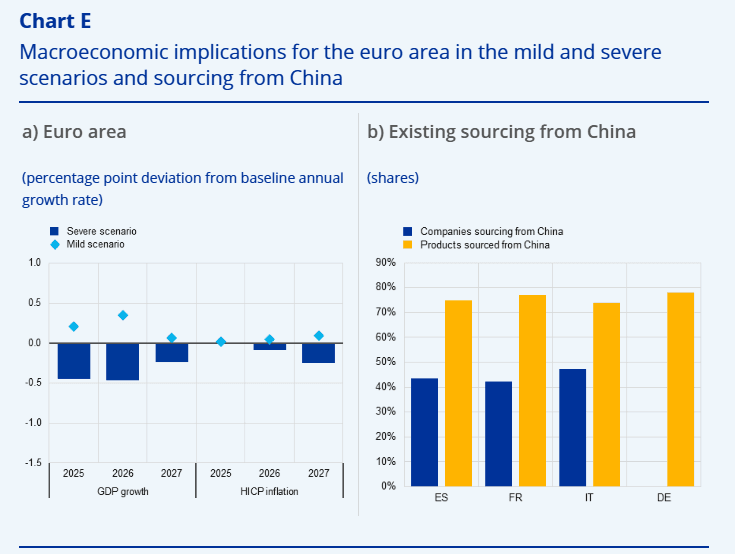

- “The June 2025 projections assume that tariffs remain at the May 2025 level over the projection horizon and that uncertainty will remain elevated, though gradually declining”. It also assumes no EU retaliation, but symmetric Chinese retaliation.

- The two scenarios analysed look at (i) “a mild scenario of lower tariffs and a faster unwinding of trade policy uncertainty” and (ii) “a severe scenario of higher tariffs and more persistently elevated trade policy uncertainty.”.

- The baseline scenario assesses GDP growth to be “overall almost 0.7 percentage points lower cumulatively over 2025-27, while the impact of US tariffs and uncertainty on euro area HICP inflation is seen as rather contained”

- The mild scenario assumed an effective US tariff rate of 13% on goods and services, including no bilaterial tariffs between the US and EU. Here, “GDP growth would be somewhat stronger, especially in 2025-26, mainly reflecting the drop in trade policy uncertainty. Inflation would be marginally higher than in the baseline in the latter part of the projection horizon, mainly reflecting stronger activity”.

- Under the severe scenario, the US effective tariff is assumed to be 28%, including almost 120% on China. EU tariffs are assumed to rise back to 20% (as announced on April 2), with the bloc also retaliating against the US. Here, GDP growth would fall to “0.5% in 2025, 0.7% in 2026 and 1.1% in 2027, cumulatively about 1 percentage point below GDP growth in the baseline, with inflation at 1.8% in 2027 compared with 2.0% in the baseline”.

- “The redirection of Chinese exports to the euro area poses a potential further downside risk to inflation beyond those entailed in the severe scenario”.

- A reminder that in today's press conference, Lagarde noted "Our projection exercise, but also the scenarios which encapsulate some of the channels of transmission to growth and inflation, some of them, not all of them. In particular, I would mention one that we discussed quite extensively during the Governing Council, which is the disruption of the supply chain that is not included in any of our scenarios."

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EURJPY TECHS: Retracement Extends

- RES 4: 165.92 2.0% 10-dma envelope

- RES 3: 165.43 High Nov 8

- RES 2: 164.90 High Dec 30 ‘24 and a key medium-term resistance

- RES 1: 164.63 High Mar 18 and the bull trigger

- PRICE: 161.74 @ 14:59 GMT May 6

- SUP 1: 161.69/60 50-day EMA / Intraday low

- SUP 2: 160.99 Low Apr 22

- SUP 3: 159.48 Low Apr 9

- SUP 4: 158.56 61.8% retracement of the Feb 28 - May 2 bull leg

A bullish theme in EURJPY remains intact despite the pullback from last Friday’s high. The recent print above key resistance at 164.19, Mar 18 high, is a positive development for bulls. A clear break of this hurdle would confirm a resumption of the upleg that started Feb 28. This would open 164.90 next, the Dec 30 ‘24 high. First key support to watch is 161.69, the 50-day EMA. It has been pierced, a clear break would undermine the bull cycle.

MNI: CANADA APR IVEY PURCHASING MANAGERS INDEX 47.9 SA

- CANADA APR IVEY PURCHASING MANAGERS INDEX 47.9 SA

US TSY OPTIONS: 5Y Midcurve Call Spread

- +10,000 wk2 FV 108.75/109 call spds, 3