AUSSIE BONDS: Hot CPI Data Pushes AU-US10Y Diff To Widest Since Mid-2022

ACGBs (YM -12.0 & XM -8.0) are sharply cheaper after the release of the new CPI Monthly series.

- The new complete monthly CPI printed at 3.8% in October, higher than expected, after September’s partial CPI of 3.5%. The trimmed mean rose 3.3% y/y, also above consensus and September’s 2.8%. This is above the top of the RBA’s 2-3% band for the first time since Q4 2024.

- Cash US tsys are ~1bp cheaper in today’s Asia-Pac session.

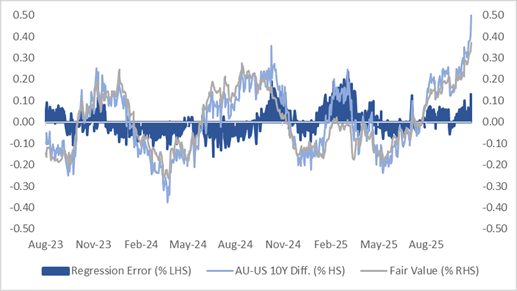

- Cash ACGBs are 8-12bps cheaper with the AU-US 10-year yield differential at +50bps, its widest level since mid-2022. This move has extended the differential’s push above the ±30bps range that had persisted since November 2022.

- However, a simple regression of the 10-year yield differential against the AU–US 1-year forward 3-month swap rate (1Y3M) differential over the past two years suggests the current spread is around 12bps too wide relative to fair value.

- The bills strip has bear-steepened, with pricing -3 to -17.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 1% probability, with a cumulative 4ps of easing priced by mid-2026.

Figure 1: AU-US Cash 10-Year Yield Differential (%)

Source: Bloomberg Finance LP / MNI

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

JGBS: Risk On Pauses Long End Yield Slide, 30yr JGB Yield Around 100-day EMA

JGB futures are holding negative, but downside sub 136.00 has been limited so far. We were last 135.96, -.18 versus settlement levels. We are still above key support levels (135.61 from Oct 8). Near term focus will be on global bond futures weakness, as markets digest positive weekend news around de-escalating US-China trade tensions. US 10yr futures are down 8 ticks to 113-06, sub its 20-day EMA support point.

- JGB yields are a touch higher, led by the belly of the curve. 5-10yr tenors up a 1bps or more. The 10yr outright yield was last near 1.67%. 20-40yr tenors are close to flat, but the recent downtrend has stalled today. The 30yr yield holding at 3.07%, which is around the 100-day EMA support point. The 2/30s JGB curve is steady at +213bps.

- We had the PPI services earlier, which ticked up to 3.0% y/y, from 2.7% prior, implying some headline CPI upside risks. Still, while some hawkish BoJ board members feel the price target has been achieved, this doesn't appear to be a core board viewpoint yet. The meeting outcome is due Thursday, with no change expected and focus on hike risks for Dec or Q1 next year.

- The local data calendar is empty tomorrow, with debt supply not returning until Friday when a 2y sale is due.

AUSSIE BONDS: Weaker Futures, Risk On Weighs, RBA's Bullock May Signal Caution

Aussie bond futures are holding weaker, but slightly up from session lows. 10yr futures (XM) were last 95.81, off 3.5bps (session lows rest at 95.79), while 3yr futures were 96.58 off 4bps (session lows at 96.57). After the initial gap lower at the open, as risk on was dominated by positive US-China trade sentiment from the weekend, we have largely been range bound. ACGB yields are off earlier highs, around +3.5-4.5bps firmer, outperforming US Tsys so far today (benchmarks

- Domestic news flow has been light, as markets await an RBA Bullock Fireside chat latter, at the ABE dinner (7:15pm AEDT). This is the final RBA speak before next Tuesday's monetary policy outcome. It may be the case Bullock stays quite non-committal around easing risks at that meeting (in Bullock's style of not ruling anything in or out). Market pricing is delicately poised, with a 25bps cut around 60% priced per OIS dated RBA contracts for the Nov meet.

- Monetary policy centered questions this evening may focus on this recent disappointing jobs data but Bullock has said previously that given volatility it is best to focus on the 3-month average of the unemployment rate which was consistent with a gradual easing in conditions.

- The 3y ACGB yield is trying to recapture the 3.40% handle, with after the earlier break in Oct out of the 3.40-3.60% range to the downside. The 10yr is short is potential resistance around 4.20%.

- The AU-US 10yr spread is +15bps, so within recent ranges. The bias would be for higher levels in this spread if we see further risk on related to US-China trade outcomes.

- On the data front, things are quiet until Wednesday's Q3 CPI print.

GOLD: Gold & Silver Continue Correction As Trade Risks Ease Substantially

While gold prices are off their earlier low of $4058.46/oz, they have held onto most of today’s losses driven by news of a draft US-China trade deal being reached. Presidents Trump and Xi are due to confirm it when they meet this week. Bullion is currently down 1.4% to $4056.0. US yields are higher while the US dollar is flat.

- US-China trade progress reduces global risks substantially as the 100% US tariff is unlikely now to be imposed on 1 November which would have resulted in retaliation from China and an escalation that would have had global consequences. Thus safe-haven demand for gold has pulled back.

- The focus this week is on Wednesday’s Fed decision. The USD OIS market has a 25bp cut priced in with another one at the 10 December meeting. Gold has expected this for some time helping to drive the rally as easing is positive given it is non-yield bearing.

- Silver is down 1.6% to $47.83 today after a low of $48.008. It fell 6.3% last week but the metal remains overbought. Initial support is at $47.55, 22 October low.

- Risk appetite has improved with the S&P e-mini up 0.7%, Nikkei +2.1% and Hang Seng +1.0%. Oil prices are flat with WTI at $61.53/bbl. Copper is 1.4% higher.

- Later October Dallas Fed manufacturing and October German Ifo survey are released. The ECB’s Elderson and Tuominen speak.