FOREX: Higher Inflation Print Drives A$ & AUDNZD Higher, RBA Expected To Hold

Aussie is outperforming the G10 today after Q3 CPI printed higher than expected across the board and likely means that the RBA will be on hold on 4 November. The AUD OIS market has almost no chance of a cut priced in with only around 25% of 25bp for the 9 December decision. AUDUSD jumped to 0.6607 on the data release but has struggled to hold moves above 0.6600. It is currently up 0.2% to 0.6599. The USD index is flat and risk appetite mixed.

- The difference in Australia-NZ central bank expectations has pushed AUDNZD higher with it reaching 1.1427 following the Aussie CPI, highest since 9 October, and is now up 0.2% to around 1.1409. NZDUSD is slightly higher today at 0.5784 off the intraday low of 0.5772.

- The RBNZ is widely expected to ease in November but the RBA looks like being on hold as underlying inflation hit the top of its 2-3% band. The RBA has been more wary of the Q3 pickup in inflation than the RBNZ, which believes that spare capacity will bring it back towards 2%.

- In August the RBA forecast Q4 trimmed mean inflation at 2.6% and now a 0.2% q/q rise is needed to achieve that which hasn’t happened since 2016 outside of Covid.

- Acting RBNZ Governor Hawkesby speaks on central bank independence at 1705 NZT/1505 AEDT today. The speech will be published on the RBNZ website.

- The Fed and BoC decisions are later Wednesday and both are expected to cut rates 25bp. US September inventories and pending home sales as well as Q3 Spanish GDP and UK September lending print.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

FOREX: AUD Crosses - Tread Water Albeit With A Long Bias

US equities ended their 3 day retracement on Friday and had a healthy bounce as US data came in as expected with no smoking guns with respect to inflation. This morning US futures have followed through, extending higher in our session, E-minis(S&P) +0.25%, NQZ5 +0.35%. The AUD continues to trade sideways albeit with a long bias in the crosses as the USD remains centre stage.

- EUR/AUD - Friday night range 1.7849 - 1.7900, Asia is currently trading around 1.7870. The pair is trading sideways after finding demand just below 1.7800 last week. Price is still in the middle of its recent 1.7600 -1.8100 range. Expect sellers to fade bounces while price remains below 1.8000.

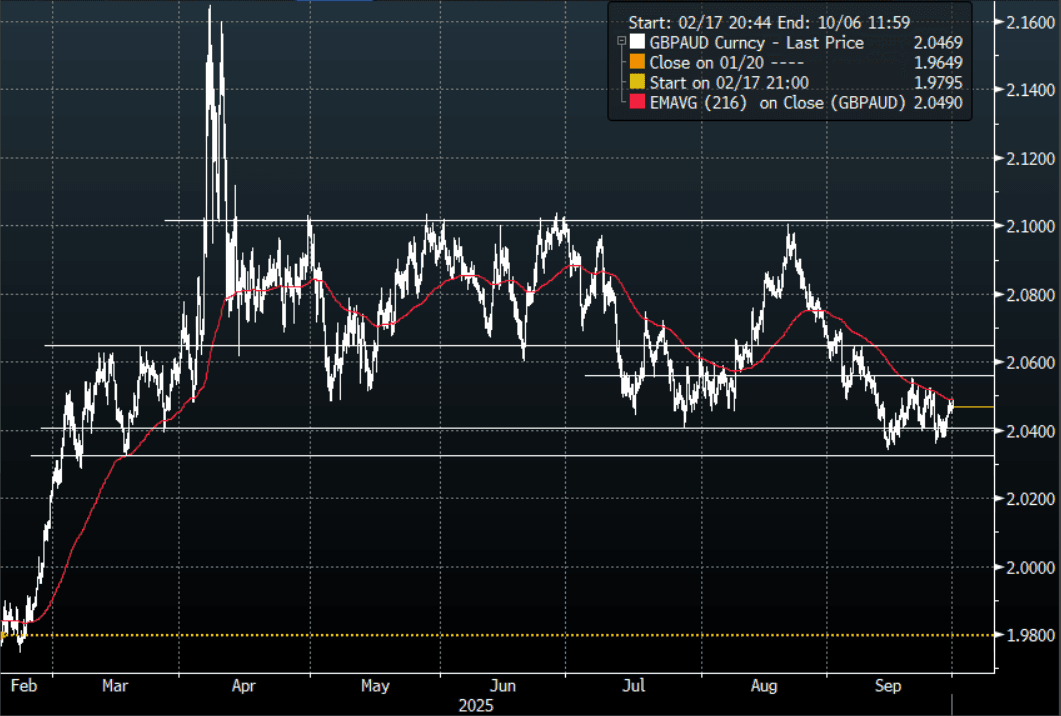

- GBP/AUD - Friday night range 2.0409 - 2.0490, Asia is trading around 2.0470. The pair has seen supply return on every look above 2.0500, I suspect rallies back to 2.0550/0650 will continue to be met with supply initially. The price action of the pair is looking potentially exhaustive but a sustained break sub 2.0300 is needed to open up a deeper pullback towards 1.9800/2.0000.

- AUD/JPY - Friday night range 97.77 - 97.99, Asia is trading around 97.75. The pair found solid demand back towards 97.00 and bounced last week with the help of the AU CPI print. While above 97.00 the focus will remain on September’s highs toward 98.50.

- AUD/NZD - Friday night range 1.1328 - 1.1349, the cross is dealing in Asia around 1.1340. The Cross has broken above the multiple highs around the 1.1200 area and is consolidating its move above 1.1300, helped by the AU CPI print. Dips should now continue to be supported as the market turns its focus towards the 1.1400/1.1500 area.

Fig 1: GBP/AUD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

USD: BBDXY - Tops Out Toward 1210, Drifts Lower Very Easily

The BBDXY range Friday night was 1204.85 - 1209.02, Asia is currently trading around 1202, -0.20%. The USD topped out towards 1210 again on Friday and has drifted lower very easily. I can’t see any big directional moves this week until the market sees the Payroll number. Next resistance is back towards the 1215-1225 area where I would expect sellers to remerge initially. The big question is at what level do the global asset managers return to selling for hedging purposes. First support back towards the 1200 area and then 1195. Quarter-end for Asset managers likely to see some USD selling to rebalance portfolios.

- Bloomberg - “Barclays Sees Dollar Sales At Quarter-End As US Assets Hold Firm: The climb in US equities to records - coupled with resilient gains in the treasury market - means that global fund managers will have to sell the dollar into the end of this quarter as they rebalance portfolios.”

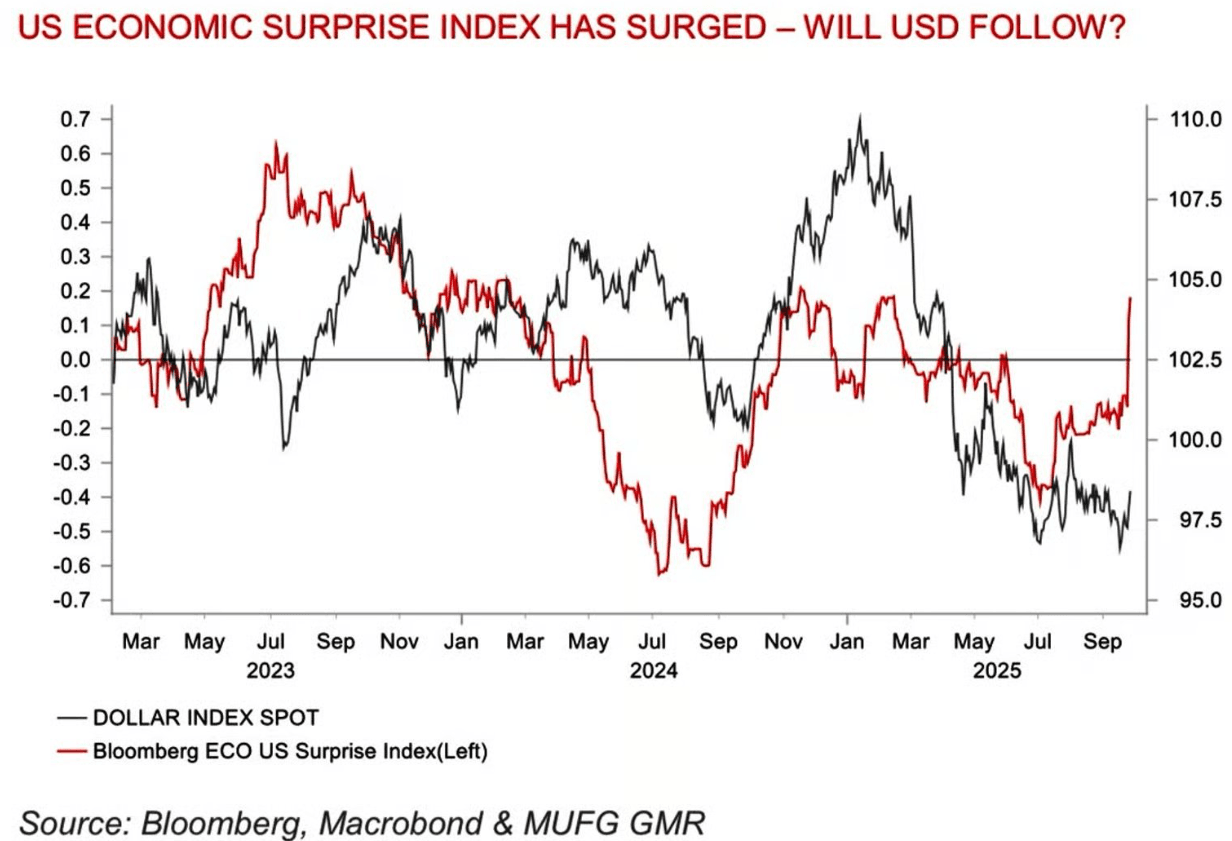

- Daily Chartbook on X: "Market is not positioned for stronger US data." - MUFG. See Graph Below.

- Sean D.Emory on X: “Government shutdown headlines always spark fear. But history tells a calmer story. Looking back at every shutdown since 1976: The S&P 500 has been flat on average during shutdowns (0.0%) and actually up +0.6% the week after. The 10-year Treasury barely moves, average change of +0.03% during, then reversing after. In other words, the market tends to look through shutdown noise quickly.

- “Investors who are bearish on the dollar should also seek protection via long positions on the yen and Swiss franc given the extent of event risks — from the US jobs report to a possible government shutdown — in the week ahead, according to JPMorgan Chase & Co.” - BBG

Fig 1: USD vs US Surprise Index

Source: MNI - Market News/Bloomberg Finance L.P

US STOCKS: Russell Index - Bounces Back From 2400, Payrolls This Week Is Key

The Russell 2000 overnight range was 2413.550 - 2434.32, closing +0.97%. The Russell 2000 found demand back towards 2400 and bounced nicely as the market reacted to benign US data. The Russell would be the biggest beneficiary of a new cutting cycle but with the market recalibrating its very dovish expectations the small cap exuberance is being tempered. CFTC data for last week show the leveraged fund community pulling back on their short holdings, the position remains significant so the risk of further scaling back remains. Payrolls this week if released will be very closely watched.

- MNI FED BRIEF: Fed's Barkin-Jobs Shakier, Inflation Less Troubling. The U.S. employment outlook has deteriorated following recent weakening in payroll growth and large downward revisions to past numbers, while inflation has not risen as much as had been feared due to tariffs.

- Bloomberg - “If the labor market data was to prove better than expected next week, it would certainly undermine the primary argument put forward by Fed Chair Powell to cut rates further and force the Fed to give more weight to the upside inflation risks,” said Derek Halpenny, head of global markets research at MUFG.”

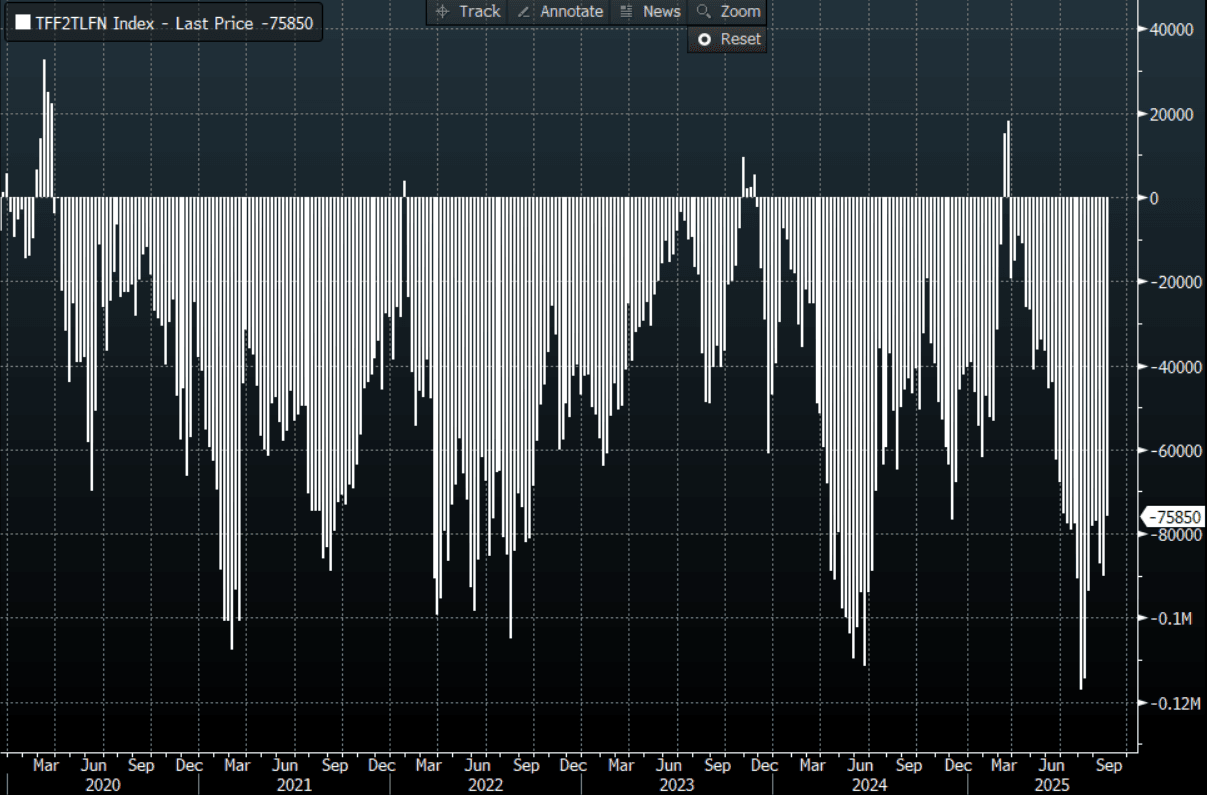

- CFTC data shows leveraged funds reduced their shorts last week to -75850( previously -90215). This has been cut back from a high of around -117000 at the beginning of August.

- These shorts would most likely be held against longs in other sectors which have done remarkably well and so the losses would not be as acute, but a move through all-time highs might make some of these reconsider the position.

Fig 1: CFTC Russell Leveraged Funds Positioning

Source: MNI - Market News/Bloomberg Finance L.P