EU HEALTHCARE: Healthcare: Week in Review

Nov-14 12:15

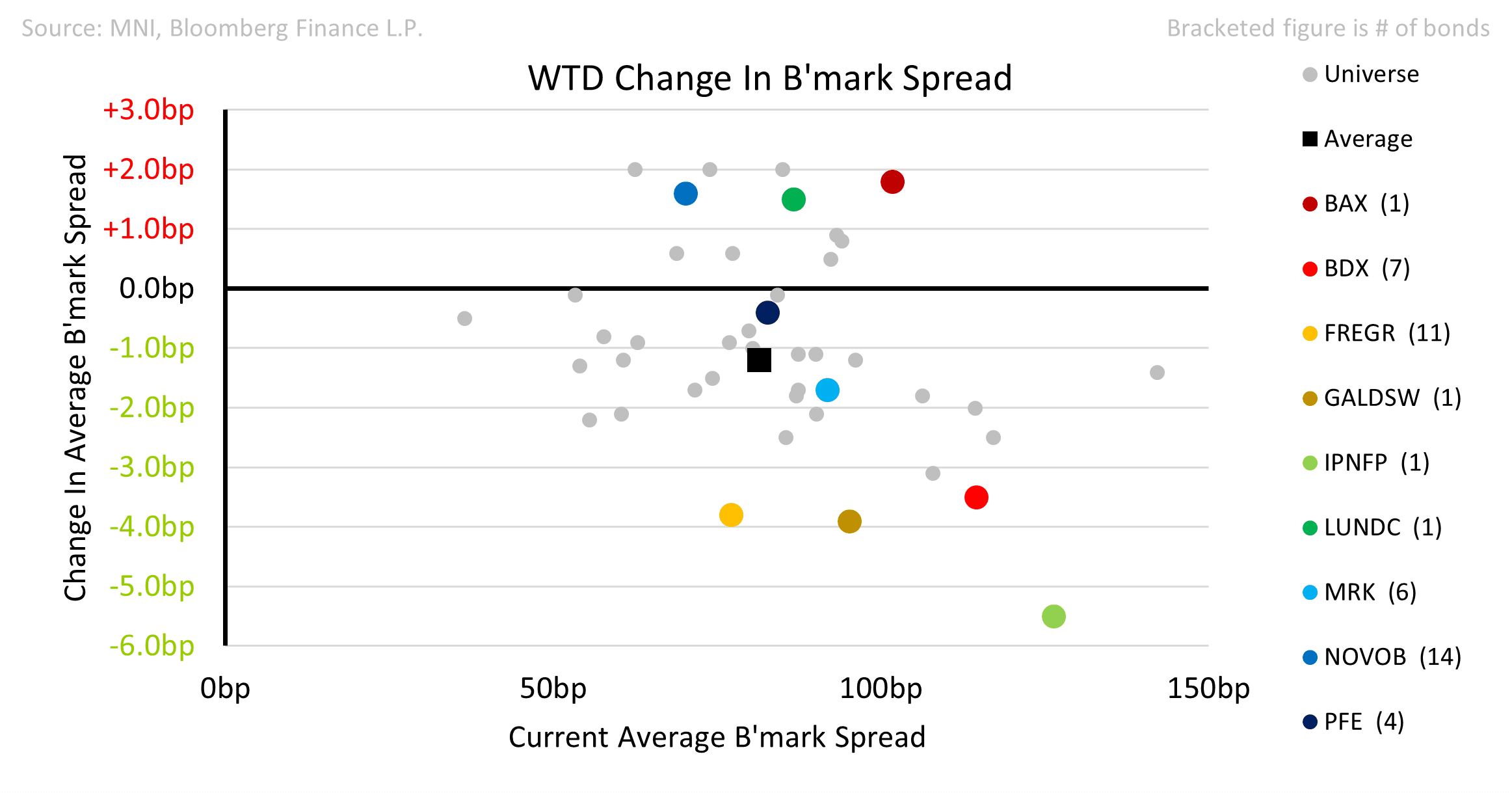

- Merck & Co agreed a $9.2bn cash acquisition of Cidara to gain access to a program of antibody treatments for influenza and cancer. M&A was always a risk, even after the $10bn Verona deal, given pipeline needs to replace Keytruda. MRK raised $6bn in Sep to finance Verona. We would expect some further issuance given $2.2bn matures in 2026.

- Pfizer sealed the Metsera takeover. An initial $6.9bn upfront payment can be made from cash but the company does have $6bn due in 2026 so issuance will come eventually.

- H Lundbeck reportedly made a $2bn bid for Avadel. The company has deleveraged from 2.4x to 1.3x post the Longboard $2.6bn deal. The CEO said this week that he had a $1bn war chest for deals.

- Baxter was cut to Baa3 following S&P’s cut last week. Deleveraging has been delayed due to headwinds in Infusion Therapies as well as in Injectables & Anaesthesia. Moody’s calculated Gross Debt/EBITDA at 5.2x. The company targets Net leverage of 3.0x – now delayed to YE26 – which equates to mid-high 3s at Moody’s. Outlook is stable. Moody’s threshold for a further downgrade is 4.0x but over a 12–18-month window.

- Bayer’s results were well received but Litigation remains a threat. We expect a Supreme Court ruling in mid-2026.

- Novo Nordisk raised €4bn in a 6-part deal to fund the Akero acquisition. The bonds priced aggressively through fair-value and held. We highlighted that NOVOB 3.25 31 looked wide on the curve.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Repo Reference Rates

Oct-15 12:03

- Secured Overnight Financing Rate (SOFR): 4.19% (+0.04), volume: $2.932T

- Broad General Collateral Rate (BGCR): 4.16% (+0.04), volume: $1.144T

- Tri-Party General Collateral Rate (TCR): 4.16% (+0.04), volume: $1.113T

- (rate, volume levels reflect prior session)

GILT PAOF RESULTS: The PAOF for the 0.125% Aug-31 Linker was not taken up.

Oct-15 12:02

- GBP375.0mln have been available.

- This leaves GBP14.254bln of the linker in issue.

EGBS: OAT Futures Narrowing Gap To Resistance; French Risks Still Present

Oct-15 11:57

OAT futures are slowly narrowing the gap to resistance at 123.23 (equates to the 3.35% 10-year yield level), currently +47 ticks at 123.16. Regional headline flow remains fairly limited, with yesterday’s pullback in near-term French political risks driving the intraday bid in EGBs.

Although French PM Lecornu now looks likely to survive tomorrow’s censure votes, France’s political/fiscal outlook still faces risks.

- Socialist leader Faure has noted that "I didn't buy the budget, I'm going to fight it tooth and nail from now on, and we'll see who on the right and the left gets satisfaction article by article."

- Lecornu will have to tread a fine line in budget negotiations to avoid losing implicit support of the Socialists and/or the LR. Some Socialist MPs (e.g. Paul Christophle) are still planning to censure the Government despite their Party’s intstructions.

- Additional concessions to the Socialists would further impede fiscal consolidation efforts, and likely push the expected 2026 deficit closer to 5.0%, rather than the 4.7% currently targeted.

That said, today’ s strength in OAT futures is continuing to support Bunds. Bund futures are once again testing the 130.00 figure (+29 ticks at 129.97), which shields resistance at 130.05 (76.4% retracement of the Jun 13 - Sep 3 bear leg).

Trending Top

Mar-27 20:13