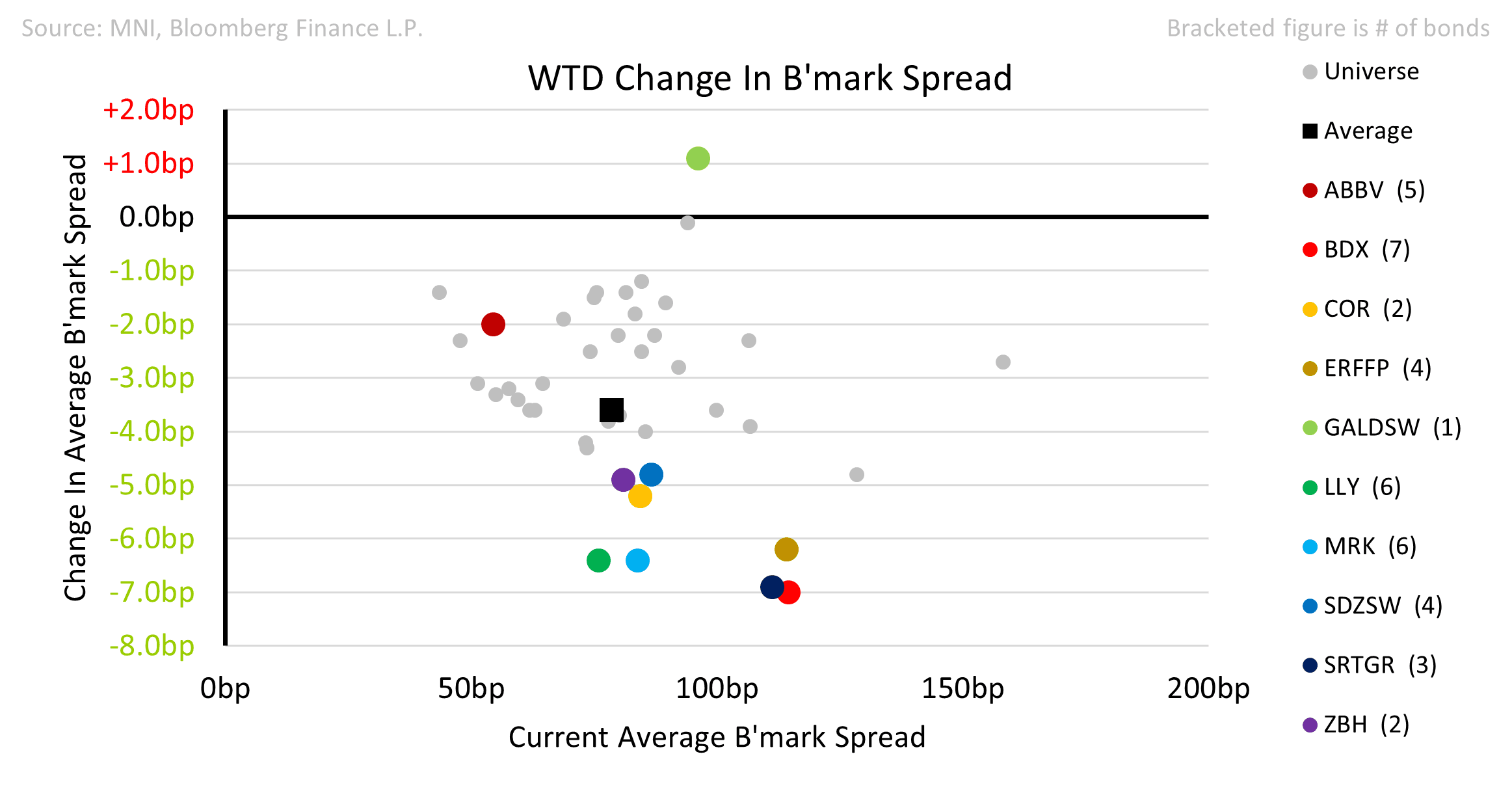

EU HEALTHCARE: Healthcare: Week in Review

The sector saw some spread compression with spreads on average 3.5bps tighter led by wider names.

• AbbVie equity was up 4% on Thursday following a successful settlement regarding Rinvoq generic competition. Rinvoq makes up c14% of ABBV sales. The company should now be immune from generic competition until 2037. Bonds 2 tighter.

• Fresenius SE tested retail appetite with €1bn of 4yr & 8.5yr 1k denomination bonds. The shorter date priced through secondaries. The company simultaneously announced a Make-Whole Call on the FREGR 4.25 2026 notes.

• Novo Nordisk announced that it would lay-off 9,000 workers (11% of total) in a cost cutting drive. Savings will be reinvested in Obesity and Diabetes opportunities. The company also reduced guidance for the full year.

• Sandoz resolved a patent dispute with Regeneron which will now enable it to produce a generic competitor to Bayer’s Eyelea from 4Q26. Bayer currently generates around 7% of total sales from the medication.

• Philips briefly sank on Monday on the announcement of a French Prosecutor probe into possible fraud at its ventilator business. It closed the week up.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

GLOBAL POLITICAL RISK: Trump To Speak To Euro Leaders Ahead Of Putin Summit

Download Full Report Here

CNN reports that the high-profile 15 August meeting between US President Donald Trump and Russian President Vladimir Putin will take place at Joint Base Elmendorf-Richardson in Anchorage, Alaska.

- In preparation for Friday’s meeting, Secretary of State Marco Rubio spoke with Russian Foreign Minister Sergey Lavrov on 12 August. “Both sides confirmed their commitment to ensure a successful event,” per a State Department readout.

- At 09:00 ET 14:00 BST, Trump will hold an emergency call with Ukrainian President Volodymyr Zelenskyy and European leaders to discuss the Ukraine war and strategy for the Putin meeting. Zelenskyy, NATO Secretary General Mark Rutte, and several European leaders will dial into the White House from Germany.

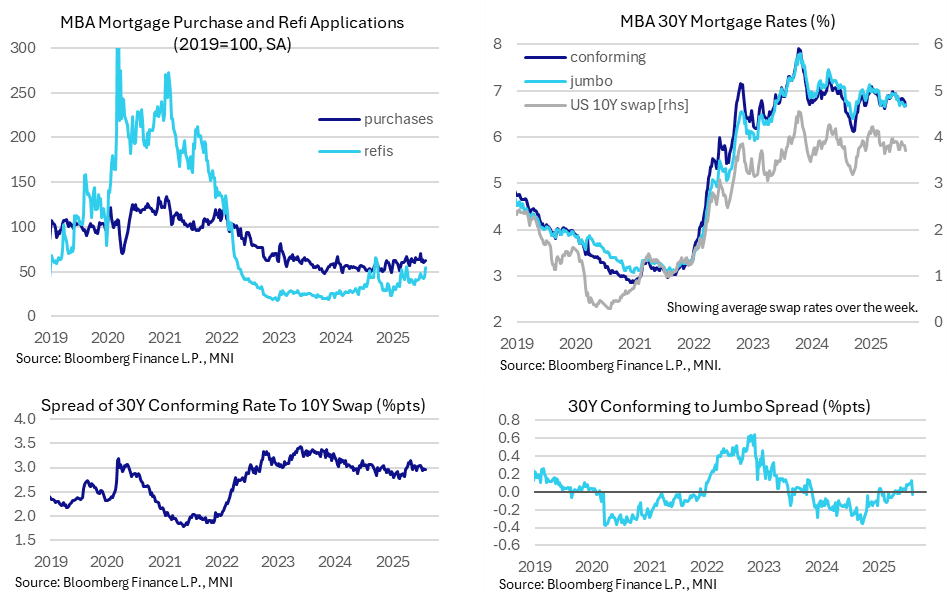

US DATA: Refis Lead An Uptick In Mortgage Applications

MBA mortgage applications increased to recent highs last week on the back of a rise in volatile refinance applications. Overall levels remains subdued however and new purchase applications continue to point an anemic trend for housing activity.

- MBA composite mortgage applications increased 10.9% sa last week after trending sideways in recent weeks, for their highest since single weeks in July and April and before that Sep 2024.

- It was however driven by a 23% increase in refis after 5.2% as new purchase applications once again saw relative underperformance with just a 1.4% increase after 1.5%.

- Comparison with 2019 averages: composite applications at 59.5%, new purchases at 62% and refis at 55%.

- These refis are reacting to a recent decline in mortgage rates, with the 30Y conforming rate falling 10bps to 6.67% after a 6bp decline the week prior. It leaves the conforming rate at its lowest since early April.

- 30Y mortgage rate to 10Y swap rate spreads remain at the low end of the 300 +/- 5bp range mostly seen since reciprocal tariffs were first detailed in early April, still wider than the 285bp averaged in Q1.

- Within the mortgage rate details, 30Y jumbo mortgage rates saw a relative correction as they increased 5bps to 6.70%. It saw the regular-jumbo spread slide from +12bp (highest since Oct 2023) to -3bp (lowest since mid-April), tentatively ending what had been a sign of some relative loosening in conditions or perhaps borrowers with higher FICO scores.

MNI: US MBA: MARKET COMPOSITE +10.9% SA THRU AUG 08 WK

- MNI: US MBA: MARKET COMPOSITE +10.9% SA THRU AUG 08 WK