BUND TECHS: (H6) Trading Closer To Its Recent Lows

- RES 4: 129.55 High Nov 26 and key resistance

- RES 3: 129.24 High Dec 1

- RES 2: 128.75 High Dec 3 and a key resistance

- RES 1: 128.08/24 High Dec 8 / 20-day EMA

- PRICE: 127.55 @ 05:37 GMT Dec 17

- SUP 1: 127.05 Low Dec 10

- SUP 2: 127.00 Round number support

- SUP 3: 126.81 2.764 projection of the Nov 12 - 20 - 26 price swing

- SUP 4: 126.58 3.000 projection of the Nov 12 - 20 - 26 price swing

Bund futures are in consolidation mode. A bear cycle is intact and the contract is trading closer to its recent lows. Scope is seen for an extension towards the 127.00 handle. Key short-term resistance is 128.75, the Dec 3 high. Note that the contract is still oversold. A stronger corrective bounce would allow this oversold condition to unwind. The price pattern on Dec 10 is a doji candle - a short-term reversal signal.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

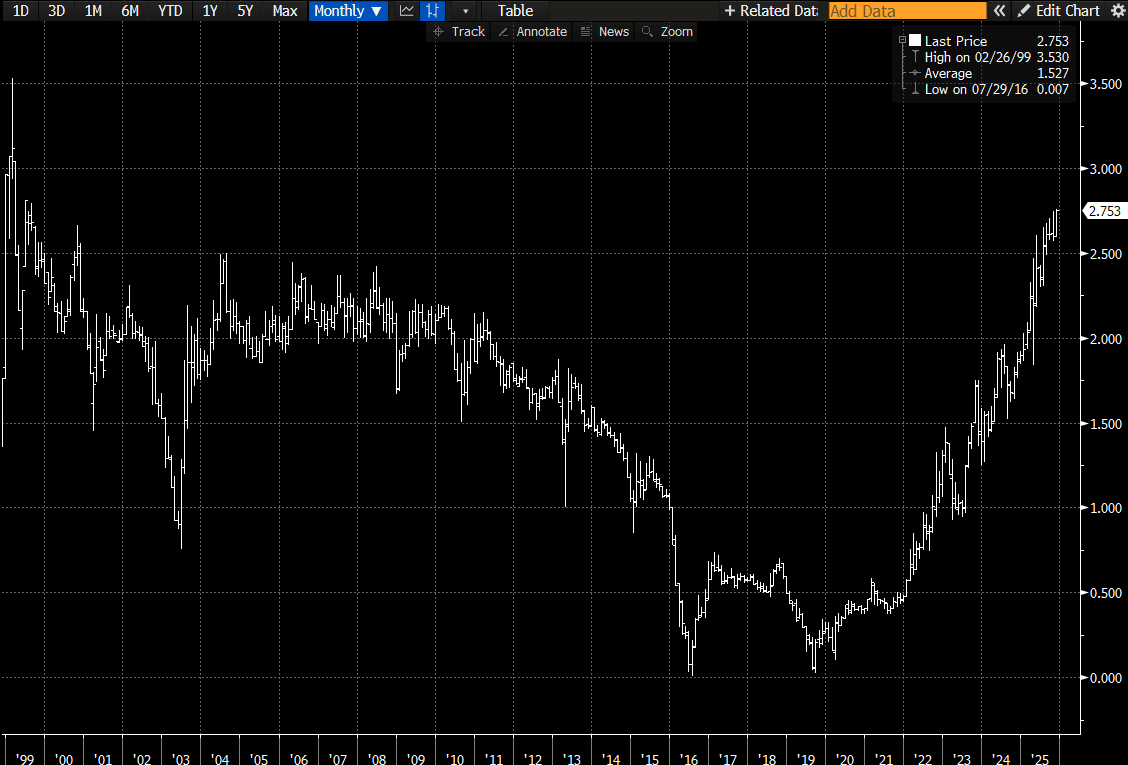

JGBS: Bear-Steepener As Market Focuses On Econ Stimulus, 20YY Highest Since '99

JGB futures are weaker and at session lows, -17 compared to settlement levels, after the release of Q3 GDP data.

- Q3 GDP (preliminary) in Japan was negative q/q, but not as much as the market forecast, thanks to upbeat business spending (+1.0%q/q versus -0.1% forecast). This was the first GDP decline since Q1 2024, but the detail paints a resilient underlying economic backdrop and comes ahead of fresh fiscal stimulus from the new Takaichi government.

- The data will likely bolster the Takaichi administration's conviction that aggressive fiscal spending is needed to shore up the economy, with the premier expected to unveil her first economic package as soon as this week. The Finance Ministry is preparing an economic package of roughly Y17tn, according to a Nikkei report published Saturday.

- Cash US tsys are flat to 1bp richer, with a steepening bias, in today's Asia-Pac session.

- Cash JGBs are flat to 4.5bps cheaper across benchmarks, with a steepening bias. The benchmark 10-year yield is 2.3bps higher at 1.733%, a fresh cycle high.

- Meanwhile, the yield on 40-year climbed as high as 3.603%, while the 20-year yield reached 2.756%, the highest since 1999. (see chart)

- Swap rates are flat to 5bps higher.

- Tomorrow, the local calendar will be empty.

Source: Bloomberg Finance LP

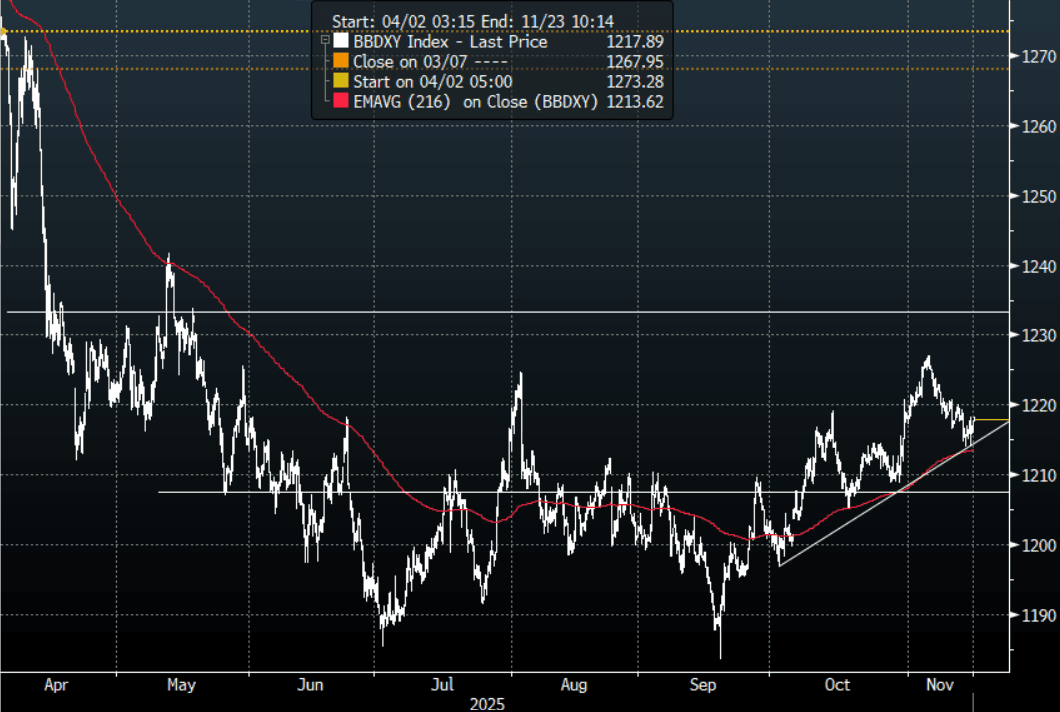

FOREX: Asia-Pac USD: BBDXY Moves Higher, Support Building Around 1213

The BBDXY has had a range today of 1216.04 - 1218.27 in the Asia-Pac session; it is currently trading around 1218, +0.15%. The USD has drifted higher in our session thanks to demand across USD/Asia, this might be differentiated when London comes in with risk turning higher after opening under early pressure. The USD again found support on Friday in the 1210-1215 area and is looking to build a base from which to move higher. I expect we do some more work around these levels but I would be looking for signs of a base forming from which to potentially move higher again. Short-term the 1221-1222 area remains the pivot on the topside and we would need a move back above there to build for a retest of the 1230-35 area.

- EUR/USD - Asian range 1.1597 - 1.1625, Asia is currently trading 1.1600. The pair stalled and moved lower after finding some decent resistance toward the 1.1650-1.1700 area. This has been the pivot within the larger 1.1400-1.1900 range over the past few months.

- GBP/USD - Asian range 1.3142 - 1.3176, Asia is currently dealing around 1.3145. I continue to favor fading rallies, as GBP looks to have put in a medium term top. A sustained move back below 1.3080-1.3100 support would see the momentum lower reinstated and focus turn back toward the 1.3000 area. Suspect rallies back toward the 1.3250-1.3300 will be sold into if we see a bounce.

- Cross asset : SPX +0.40%, Gold $4080, US 10-Year 4.144%, BBDXY 1216, Crude Oil $59.57

- Data/Events : France Bloomberg Nov. France Economic Survey, EZ Bloomberg Nov. Eurozone Economic Survey/European Commission Publishes Autumn Economic Forecasts, Spain Bloomberg Nov. Spain Economic Survey, Italy Bloomberg Nov. Italy Economic Survey, Germany Bloomberg Nov. Germany Economic Survey/CPI

Fig 1: BBDXY Spot 4H Chart

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Little Changed, Focus On Upcoming Data & Nvidia Results

TYZ5 is trading at 112-17+, +0-00+ from closing levels in today's Asia-Pac session.

- Cash US tsys are 1bp richer to 1bp cheaper, with a steepening bias, in today's Asia-Pac session. On Friday, US tsys finished showing a modest bear-steeper, with benchmark yields 1-4bps higher.

- US equity futures are slightly firmer in today's Asia session. The S&P looked to be rolling over again on Friday night, down almost 1.5% before it found solid demand during the N/Y session and pared back all the day's losses.

- The market will be looking toward the release of some US data this week (September's delayed nonfarm payrolls report for next Thursday) to get a gauge on things and also heavily focused on the upcoming Nvidia results, which will heavily impact the direction of markets this week.

- Friday's Fed commentary (with the usual exception of Gov Miran calling for further easing in December) was roundly hawkish, with Dallas's Logan and KC's Schmid reiterating their opposition to a December rate cut, largely out of concern over entrenched inflation. A December cut remained around 50/50 priced.

- Along with the newly-rescheduled data, this week's calendar includes the October FOMC minutes (we're watching for colour on the debate over whether to ease any further) and flash November PMI data.