AUSSIE 10-YEAR TECHS: (H6) Marked Lower

- RES 3: 95.982 - 76.4% retracement Sep’24 - Nov’24 downleg

- RES 2: 95.960 - High Apr 7 (cont.)

- RES 1: 95.900 - High Oct 17

- PRICE: 95.185 @ 16:18 GMT Dec 17

- SUP 1: 95.120 - Low Dec 10

- SUP 2: 95.087 - 2.0% Lower Bollinger Band

- SUP 3: 94.276 - 1.0% 10-dma envelope

Aussie 10-yr futures remain well toward the bottom of the recent range, having taken out all major support levels in the process. With 95.275 cleared, prices are pushing to new contract lows, opening vol-band support through 95.087 and into 94.276. Any recoveries need to break back above 95.900 to signal near-term bullish traction.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

US TSYS: Futures Open Slightly Weaker, Tuesday's Data-Calendar Is Light

TYZ5 is dealing at 112-18, -0-02+ from closing levels in today's Asia-Pac session.

- Cash US tsys finished Monday’s session slightly richer.

- August construction data - whose Oct. 1 release was delayed 6 weeks due to the federal government shutdown - showed a 0.2% M/M rise in spending (-0.1% expected, 0.2% prior rev from -0.1%). The NY Fed's Empire State Manufacturing Survey impressed in November, with the current General Business Conditions index rising 8 points to a 1-year high of 18.7 (well above the 5.8 expected).

- Fed Vice Chair Jefferson said he's likely one of the 9 FOMC members who anticipated cutting rates in Sep, Oct and Dec (in his September Dot Plot) and if forced to guess we would think he is still marginally in favor of a December cut and here he again highlights "increased downside risks to employment compared to the upside risks to inflation, which have likely declined somewhat recently".

- Stocks hit hard on Monday. Chip makers continue to lead late-session declines, followed by Financial names. Note, Nvidia is expected to release Q3 earnings this Wednesday.

- Tuesday's data schedule is light, with markets gearing up for the now-much-delayed September NFP print due this Thursday.

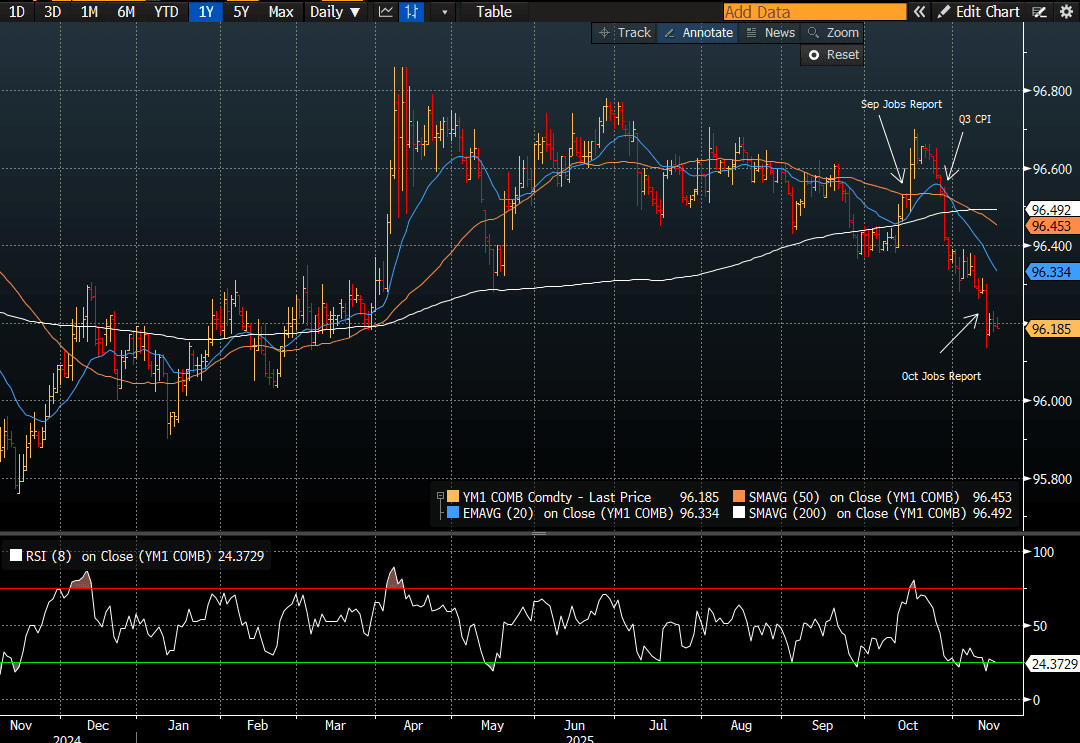

AUSSIE 3-YEAR TECHS: (Z5) Struck by Strong Jobs

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.200 @ 15:48 GMT Nov 17

- SUP 1: 96.135 - Low Nov 13

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Prices slid sharply on the better-than-expected jobs data, pushing prices through first support at 96.280. This makes for a fresh contract low, exposing 95.900 on the continuation chart for direction. The slower pricing for additional RBA easing should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.900 as the next major support.

AUSSIE BONDS: Little Changed, Subdued Start To Week For US Tsys, Jun-54 Supply

ACGBs (YM -1.0 & XM -0.5) are little changed in line with cash US tsys Monday’s close.

- YM1 technicals continue to point to further weakness. (see chart)

- Fed Vice Chair Jefferson said he's likely one of the 9 FOMC members who anticipated cutting rates in Sep, Oct and Dec (in his September Dot Plot) and if forced to guess we would think he is still marginally in favor of a December cut and here he again highlights "increased downside risks to employment compared to the upside risks to inflation, which have likely declined somewhat recently".

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +34bps.

- The bills strip is unchanged across contracts.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 10bps of easing priced by mid-2026.

- Today, the local calendar will see RBA Minutes of the Nov. Policy Meeting ahead of the Wage Price Index on Wednesday.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond today, A$1000mn of the 2.75% 21 June 2035 bond on Wednesday and A$700mn of the 1.25% 21 May 2032 bond on Friday.

Bloomberg Finance LP