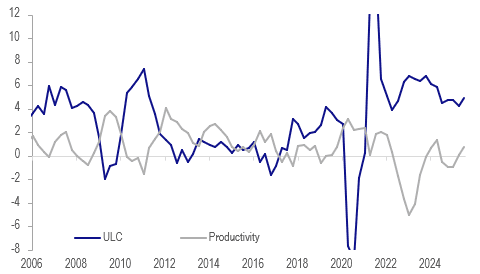

AUSTRALIA DATA: Gradual Productivity Recovery, ULC Growing Strongly

Productivity growth in Australia has been lacklustre for some time and concerning the RBA as it limits the rate of wage growth consistent with its inflation target over the medium-term. It appears to be slowly improving though with a 0.1% q/q rise in Q3, the third straight increase, bringing annual growth to +0.7% up from Q2’s 0.1%. However, RBA Governor Bullock said in November that the Board is concerned about the pace of unit labour cost (ULC) growth and Q3 is likely to have added to these worries.

- Q3 ULC rose 1.3% q/q to be up 4.9% y/y, the highest growth rate since Q2 2024 and historically elevated. It was up 4.2% y/y in Q2. Q3 2024 saw a 0.7% q/q rise in ULC and so it was substantially higher this year.

- Bullock told the Senate Economics Committee on Wednesday that the Q3 rise in inflation may suggest a rebuilding in margins after they were squeezed earlier but still reflects demand strong enough to allow this. Given the strong rise in Q3 ULC, businesses may have had to increase prices.

- Hours worked rose 0.2% q/q in Q3, the seventh straight quarterly increase, but annual growth eased to 1.3% after Q2’s 1.9%. The fact hours are still rising is consistent with the RBA’s view that the labour is a little tight.

Australia productivity vs ULC growth y/y%

Source: MNI - Market News/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OIL: Crude Post-OPEC Gains Unwinding As Excess Supply Remains A Concern

Oil prices rose moderately when the APAC session started today following OPEC’s decision to increase output in December by 137kbd, in line with November, but announced it would pause production rises through Q1, which is a time of lower demand. It has been increasing quotas to regain market share but a jump in both non-OPEC and OPEC output is driving excess supply with a record surplus forecast for 2026.

- WTI reached a high of $61.48/bbl early in the session and has trended lower since and is currently +0.2% to around $61.12, close to the intraday low. Initial support is at $59.64. Brent rose to $65.26/bbl to start with and then fell to a trough of $64.89, above support at $63.37. It is currently up 0.3% to $64.95.

- It appears that the latest US/EU sanctions targeting Russian oil majors Rosneft and Lukoil are having an impact with reports that refiners in China are looking to alternatives. Bloomberg reports that around 400kbd are impacted or around 45% of China’s Russian oil imports, which is pressuring prices for Russian grades.

- Morgan Stanley has lifted its Brent forecast $2.50 to $60/bbl for Q1, as OPEC decides to leave production targets unchanged over Jan-Mar, according to Bloomberg.

- Later the Fed’s Daly and Cook appear with Cook speaking on the economy and monetary policy. With US data still scarce due to the government lockdown, the October manufacturing PMI & ISM data are likely to be watched closely. European October manufacturing PMIs are also released and the ECB’s Lane speaks.

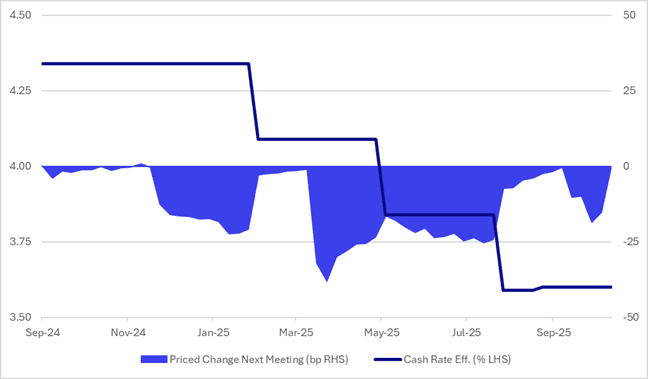

AUSSIE BONDS: Weaker Ahead Of Tomorrow's RBA Policy Decision

ACGBs (YM -5.0 & XM -5.5) are weaker and at or near session lows.

- Tomorrow, the local calendar will see the RBA Policy Decision.

- The Q3 trimmed mean print at 3.0% y/y up from 2.7% and at the top of the 2-3% target band was a “material miss” for the RBA and meant that the Board is now highly likely to leave rates at 3.6% at its 4 November decision.

- The Board is likely to remain highly data-dependent and cautious given inflation’s renewed shift higher and the emerging domestic recovery, but easing labour market conditions. (see MNI RBA Preview here)

- Cash ACGBs are 5bps cheaper.

- The bills strip is -2 to -6 across contracts, with a steepening bias.

- RBA-dated OIS pricing implies almost no chance of an easing, with just a 2% probability assigned. As it currently stands, the OIS market has only an 80% chance of a 25bp cut by mid-2026. (see chart)

- The AOFM plans to sell A$1200mn of the 4.25% 21 March 2036 bond on Wednesday and A$800mn of the 3.00% 21 November 2033 bond on Friday.

Figure 1: RBA-Dated OIS – Cash Rate Vs. Priced Change Next Meeting

Source: Bloomberg Finance LP / MNI

GOLD: Softer USD Helps Gold Recover From China VAT Change Losses

Gold prices dipped to $3962.59/oz early in the APAC session driven by news that China was removing the retail tax exemption on gold but they have since recovered to make a high of $4015.42 supported by a weaker US dollar (BBDXY -0.1%). They are currently up 0.1% to $4005.5.

- China’s retailers will no longer be able to offset VAT on gold sales including bars and jewellery, which is likely to reduce demand through higher prices. The main impact is likely to be on sentiment which has contributed to gold’s major rally in 2025, according to Bloomberg.

- Silver is 0.2% higher at $48.80, close to the intraday peak at $48.911 but holding below initial resistance at $49.456.

- Equities are generally stronger with the S&P e-mini up 0.2% and Hang Seng +0.6%. Oil prices are higher with WTI +0.4% to $61.19/bbl. Copper is flat.

- Later the Fed’s Daly and Cook appear with Cook speaking on the economy and monetary policy. With US data still scarce due to the government lockdown, the October manufacturing PMI & ISM data are likely to be watched closely. European October manufacturing PMIs are also released and the ECB’s Lane speaks.