RENEWABLES: German Wind Output Forecast Comparison

Jan-14 14:43

See the latest German wind output forecast for base-load hours from SpotRenewables vs Bloomberg's EC...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

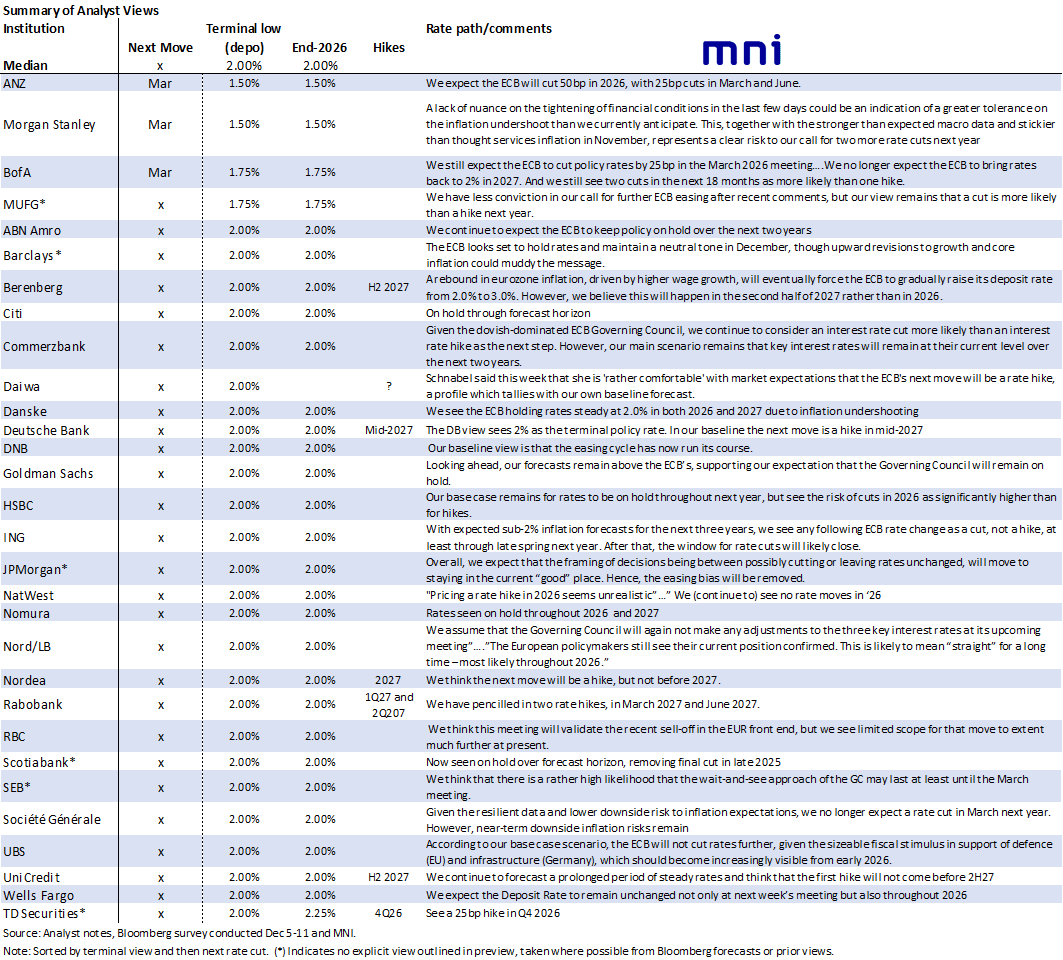

ECB: Analyst Views Ahead Of Thursday's ECB Decision

Dec-15 14:42

- There remains a solid consensus that the ECB will hold the deposit rate at 2.00% at the December decision and through next year.

- A handful of analysts still expect further easing this cycle, with ANZ and Morgan Stanley forecasting in a terminal rate of 1.50%.

- The only analyst with a 2026 hike in their baseline scenario is TD Securities (Q4 '26). Others have pencilled in hikes in 2027.

- Analysts expect the meeting-by-meeting and data-dependent approach to be retained, alongside President Lagarde’s characterisation of policy being in a “good place”. This implies no explicit endorsement of market pricing for the next rate move to be a hike.

EQUITY OPTIONS: Large Commerzbank Option

Dec-15 14:41

CBK (18/06/27 vs 16/06/28) 20p, trades 1.1 for the 2028 in 51k.

US SWAPS: 2-Year Spread Hits Widest Since April

Dec-15 14:37

2-Year swap spreads are ~2.5bp wider vs. levels seen ahead of last week’s FOMC decision, hitting the widest level seen since April in the process.

- Much of the post-Fed widening has stemmed from the central bank announcing that it will buy $40bln of monthly in bills as part of its reserve management purchase operations (which got underway on Friday).

- The announcement compared to expectations that RMPs would begin in 2026.

- The Fed also noted its plans to keep RMPs "elevated" for a few months to respond to anticipated seasonal funding pressures at year-end and during the April tax season.

- J.P.Morgan have recommended initiating 2s/10s swap spread curve flatteners. They believe that the “announcement for front-loaded reserve management purchases by the Fed is supportive for swap spreads”. At the same time, their H126 projections for swap spreads suggests that “the 10-Year sector is likely to underperform the rest of the curve, and seasonal factors point to a flattening of the 2s/10s swap spread curve”.

Related bullets

Related by topic

Renewables

Energy Data

Germany

Emissions

US Natgas

US

TTF ICE

Asia LNG

Asia

Gas Positioning