POWER: German Spot at Highest Discount to France Since 29 Dec 2024

Dec-31 12:32

The German spot settled at its highest discount to the French equivalent since 29 December 2024 as German wind is expected to reach a 70% load factor, revised up by around 2GW on the day, placing the contract €38.93/MWh below France.

- The German spot power index dropped to €9.75/MWh, compared with to €87.31/MWh in the previous session.

- Mean temperatures in Dusseldorf are forecast at 1.5C on Thursday, up from 1.1C on Wednesday but below the seasonal average of 3.3C.

- German wind output is forecast at 50.01GW during base load on Thursday, up sharply from 27.64GW on Wednesday.

- German rescom gas demand is forecast at 197.13mcm/d on Thursday, firm from 197.82mcm/d on Wednesday, Bloomberg data showed.

- Power demand in Germany is forecast at 55.47GW on Thursday, up from 51.39GW on Wednesday, Bloomberg data showed.

- The French spot power index cleared at €48.68/MWh, compared with €89.07/MWh the day before.

- French nuclear availability is at 91% on Wednesday, up from 90% on Tuesday, data from RTE show, cited by Bloomberg.

- Mean temperatures in Paris are forecast at 0.1C on Thursday, up from -0.1C on Wednesday but below the seasonal normal of 4.7C.

- Wind output in France is forecast at 5.77GW during base load on Thursday, from 4.3GW on Wednesday, according to SpotRenewables.

- Power demand in France will be at 67.55GW on Thursday, down from 70.16GW on Wednesday, Bloomberg data showed.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Key Support In Bunds Remains Exposed

Dec-01 12:22

- In the FI space, a bear threat in Bund futures remains present and recent gains appear corrective. Key short-term support and the bear trigger to watch lies at 128.37, the Nov 20 low. Clearance of this level would resume the bear leg and open 128.25, the Oct 7 low. Key short-term resistance has been defined at 129.21, the Nov 26 high. A clear break of the average would highlight a stronger reversal and open 129.40, the Nov 13 high.

- A volatile spike higher in Gilt futures on Nov 26 resulted in a breach of some important short-term resistance points. This strengthens a bullish theme and a continuation higher would signal scope for a climb towards resistance at 92.55, the Nov 11 high. A gap in the daily chart has been filled. For bears, a stronger reversal would refocus attention on the first important support at 90.53, the Nov 26 low.

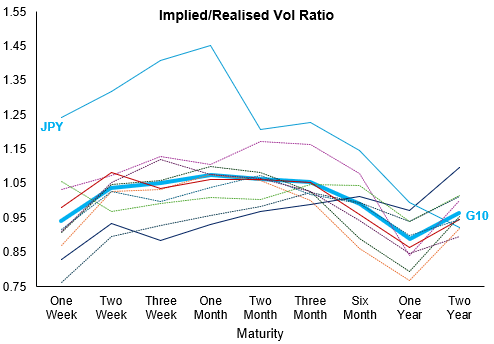

JPY: USDJPY Extends Break of Support, Aided by Moderate Phase of Risk-Off

Dec-01 12:22

- We noted the break below 20-day EMA support earlier this morning, and that effect is being compounded by the moderate phase of risk-off into the NY crossover. The Y155.00 handle is under pressure, with support seen scant above Y153.06, the 50-day EMA.

- Ueda remains the initial trigger here, but the incoming US ISM Manufacturing data will keep focus on the USD leg in very near-term trade. We note support expected into the 98.992-99.063 area for the USD Index, which could contain any further decline in USDJPY.

- Notably, vol markets are signalling JPY is the currency in focus across December, evident in the front-end of the JPY implied vol curve being notably elevated relative to broader G10. This effect translates to the implied/realised vol ratio clearing all other currencies for maturities out to 2 years (see below):

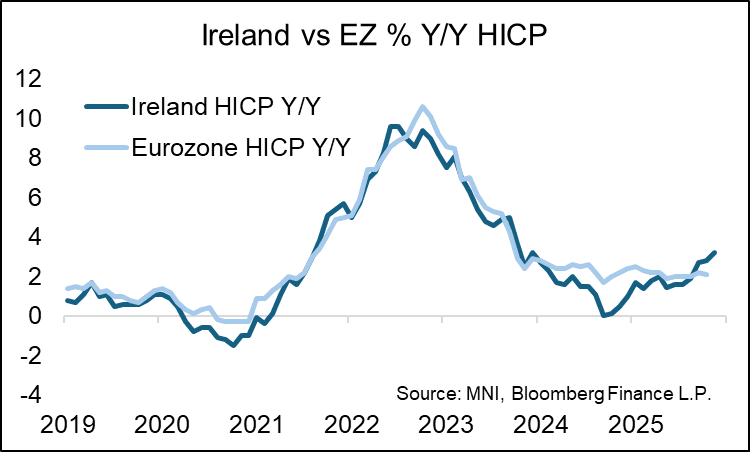

EUROPEAN INFLATION: Ireland HICP Acceleration Driven By Base Effects

Dec-01 12:11

Ireland's 0.4pp headline HICP acceleration to 3.2% Y/Y does not materially impact MNI's tracking estimate of Eurozone HICP, now standing at 2.12% Y/Y. As noted earlier, we have seen analyst estimates after last week's "big four" eurozone releases in the 2.1-2.2% Y/Y range.

- The Y/Y acceleration in Ireland was driven by base effects, with HICP at -0.2% M/M vs -0.5% M/M in Nov 2024 (and with mixed November history further back including -0.9% M/M in 2023 and 0.2% in 2022).

- "Excluding energy and unprocessed food, the HICP is estimated to have risen by 3.0% since November 2024", the Irish statistics office comments.

- On non-core: "Energy prices are estimated to have grown by 0.7% in the month and rose by 3.3% over the 12 months to November 2025. Food prices are estimated to be unchanged in the month and increased by 4.2% in the last 12 months."

- On a broader perspective, Irish HICP continues to widen its gap to the Eurozone-wide measure after being one of the countries with the lowest readings in the bloc around late-2024.