RENEWABLES: German Morning Renewable Forecast

See the latest German renewables forecast for base-load hours from this morning for the next seven days. German wind is expected to hit a weekday low next week on 26 Dec (Thurs) at just a 7% load factor, which could lift prices from the previous session and a weekday high.

German: Wind for 21 – 28 December

- 21 December: 36.70GW (+200MW),

- 22 December: 36.06GW (-177MW),

- 23 December: 32.14GW (-409MW),

- 24 December: 12.92GW (+2.63GW),

- 25 December: 9.60GW (+1.47GW),

- 26 December: 4.52GW (unchanged),

- 27 December: 6.44GW (unchanged)

- 28 December: 4.29GW

German: Solar for 21 – 28 December

- 21 December: 1.77GW (-190MW),

- 22 December: 1.50GW (unchanged),

- 23 December: 0.960GW (-186MW),

- 24 December: 2.16GW (-170MW),

- 25 December: 2.41GW (-1.45GW),

- 26 December: 5.53GW (unchanged),

- 27 December: 5.85GW (unchanged)

28 December: 6.03GW

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

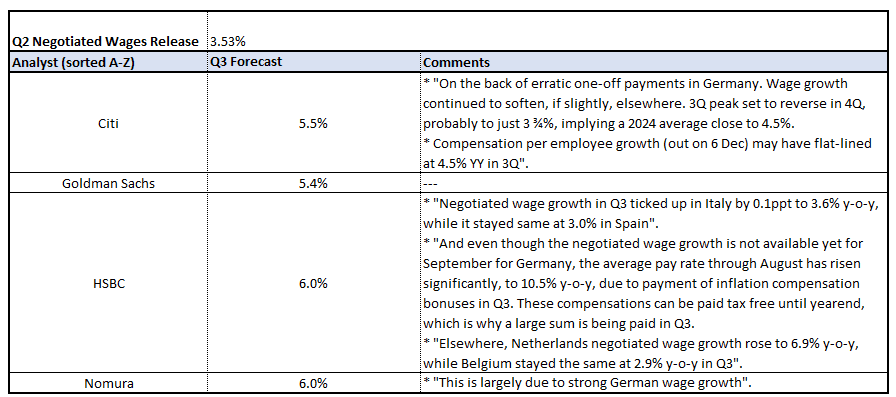

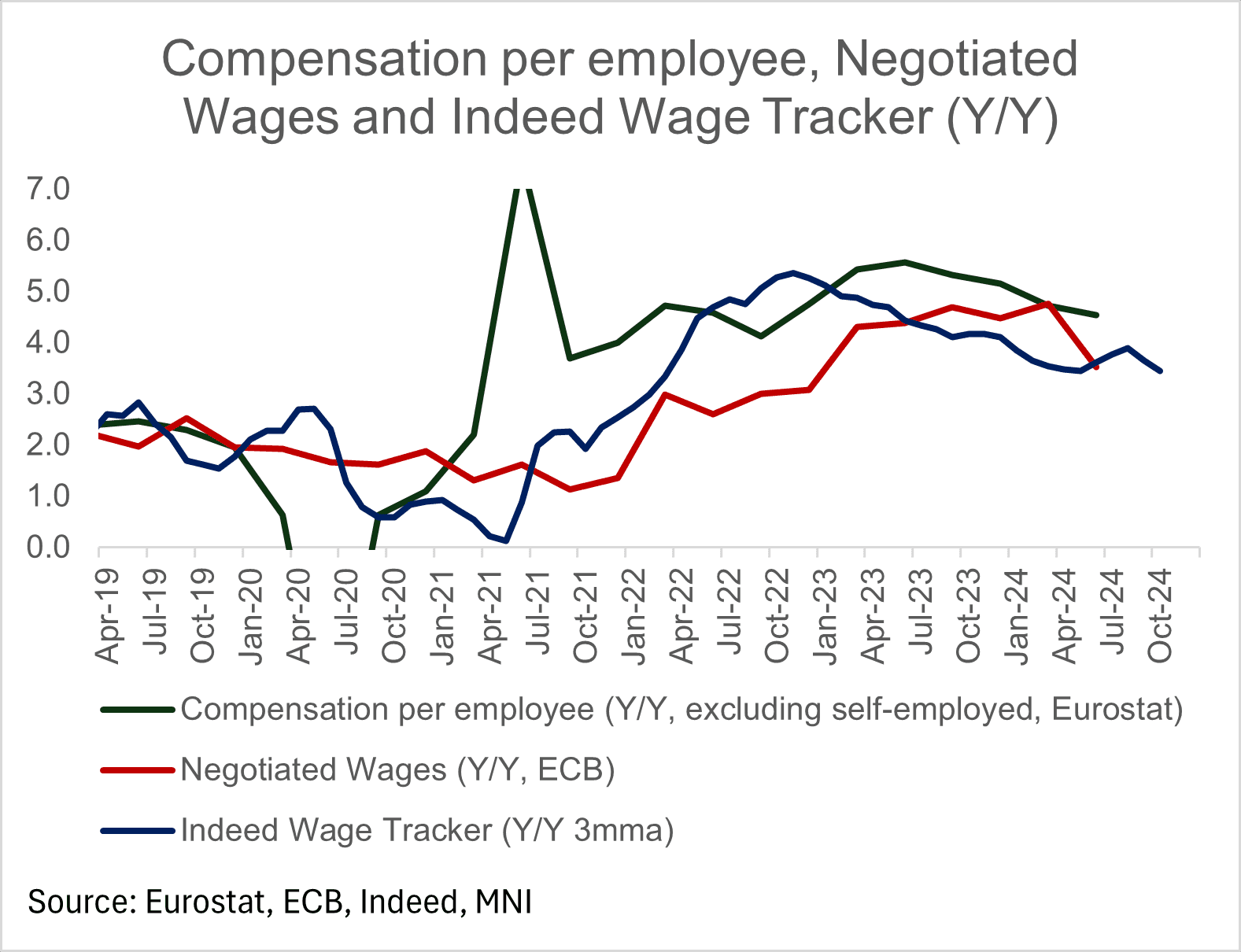

EUROZONE DATA: One-off German Deals Expected To Skew Q3 Negotiated Wages Higher

Euro-area Q3 negotiated wage growth, due at 1000GMT/1100CET, is expected to print between 5-6% Y/Y according to a handful of analyst estimates we have seen. This would be a marked uptick from the 3.5% Y/Y in Q2, but is largely due to one-off effects in Germany (German Q3 negotiated wages rose 8.8% Y/Y, and 5.6% Y/Y excluding one-off payments).

- Negotiated wage growth is expected to fall back in Q4 (Citi expect 3.75% Y/Y), not least due to last week’s IG Metall Union and Gesamtmetall pay deal in Germany. Analysts have generally viewed the deal as weaker than would have been expected by the ECB.

- Although negotiated wages were a key focus for the ECB earlier this year (amid concerns around persistent services inflation pressures) focus has shifted towards the weakening growth outlook in recent months.

- As such, the ECB can probably afford to look through the uptick in Q3 negotiated wages, placing more focus on Friday’s November flash PMIs as a timely indicator of economic activity.

EURIBOR OPTIONS: Call strip buyer

Euribor call strip, looking for more aggressive/ lower Interest Rate in the second half of next Year, 0.50%.

- ERM5/ERU5/ERZ5 99.50c strip, bought for 4 in 2k.

BUNDS: /SWAPS: ASWs Flat To Tighter, Long End Spreads Still Seem Most Vulnerable

This morning’s downtick in bonds leaves 3-month Euribor ASWs little changed to ~1bp tighter on the day, with the long end leading the tightening.

- This comes after yesterday’s 3-4bp of widening across the curve, which initially came on the back of risk-off trade surrounding the Russia-Ukraine conflict.

- Although that moved proved somewhat sticky, even as core global FI markets sold off in the afternoon

- Commerzbank dig a little deeper, noting “beyond risk-off, the tensions in term repos are showing tentative signs of easing and we see more room for markets to adjust into year-end.”

- This leads them to conclude that “this is in line with our view that repo and Schatz spreads should remain anchored, while the (ultra-) long ASW recovery looks more vulnerable once the focus shifts to next year's supply.”