EUROPEAN FISCAL: German Government GDP Revisions Likely To Lower Financing Gap

Oct-08 15:36

- Today's upward revisions of the German government's GDP estimates will likely have a net reductive impact on the current E172.3bln financing gap in the federal fiscal plan through 2029 relative to the estimates using the previous GDP assumptions.

- The new GDP forecast (0.2% 2025, 1.3% 2026, 1.4% 2027) will first flow into updated tax estimates scheduled for publication on October 23, and should, on balance, result in higher estimates for taxes including VAT, corporation tax, and income tax. Note that new legislation approved since the last estimates (includes the "growth booster" legislation package as well as the restaurant VAT decrease starting Jan 2026) will mechanically act counter to today's GDP impact.

- These tax estimates will subsequently be used in the finance ministry's financial plans / budget calculations.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

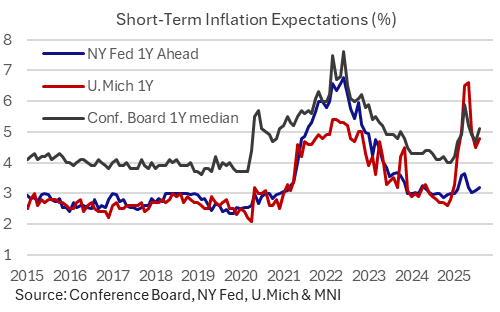

US DATA: NY Fed Consumer Survey: Inflation Expectations Looking Stubborn (1/2)

Sep-08 15:33

The New York Fed's Survey of Consumer Expectations leaned in a stagflationary direction in August, showing both an uptick in short-term inflation expectations and increasing pessimism on the labor market front. Overall the deterioration in the labor market outlook is likely to be the main takeaway from the FOMC going into its meeting next week, stubborn inflation expectations are unlikely to be ignored, illustrative of the Fed's current policy dilemma.

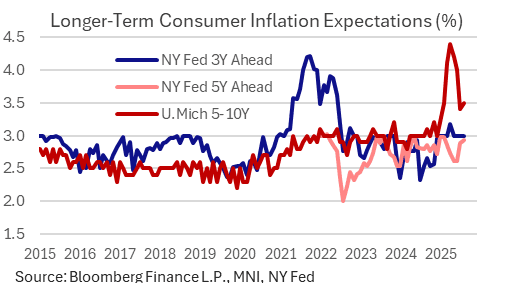

- Starting with the closely-watched inflation expectations, the survey saw a rise in the 1Y median to a 3-month high 3.20% from 3.09% prior. The 3Y median was steady at 3.00% for a 4th consecutive month, but the 5Y median ticked up to a 6-month high 2.93% (2.88% prior).

- The 1Y reading mirrors August increases in other consumer expectations surveys of 1Y inflation expectations, including UMichigan (4.80% from 4.50%) and Conference Board (6.20% from 5.70%). All are below tariff-related peaks earlier this year but appear to have bottomed out.

- We also note a subtle uptick in the UMichigan 5-10Y metric, to 3.5% from 3.4%. In both surveys, this metric appears to have stalled out above pre-2025 tariff levels.

- That said, we think most on the FOMC consider the NY Fed survey to be the most "robust" among these measures in terms of methodology. While it's shown much less dramatic swings than its counterparts, it is showing short-term/3Y pressures as being a little more elevated than in previous periods when the Fed was contemplating easing.

- Somewhat counter-intuitively, the survey's measure of median one-year ahead point predictions for various commodity price changes (eg gas, food, healthcare, education, rent, gold) were all flat to somewhat lower. The big standout on that front was for rent, for which inflation is seen running at 6.0%, down sharply since 9.1% in June and lowest since January.

- Median uncertainty over future inflation ticked a little higher though remained in recent ranges (which since the pandemic have been elevated vs the 2013-19 period,

FED: US TSY 13W BILL AUCTION: HIGH 3.940%(ALLOT 33.04%)

Sep-08 15:32

- US TSY 13W BILL AUCTION: HIGH 3.940%(ALLOT 33.04%)

- US TSY 13W BILL AUCTION: DEALERS TAKE 36.48% OF COMPETITIVES

- US TSY 13W BILL AUCTION: DIRECTS TAKE 8.35% OF COMPETITIVES

- US TSY 13W BILL AUCTION: INDIRECTS TAKE 55.17% OF COMPETITIVES

- US TSY 13W BILL AUCTION: BID/CVR 2.81

FED: US TSY 26W BILL AUCTION: HIGH 3.730%(ALLOT 60.48%)

Sep-08 15:32

- US TSY 26W BILL AUCTION: HIGH 3.730%(ALLOT 60.48%)

- US TSY 26W BILL AUCTION: DEALERS TAKE 22.61% OF COMPETITIVES

- US TSY 26W BILL AUCTION: DIRECTS TAKE 9.62% OF COMPETITIVES

- US TSY 26W BILL AUCTION: INDIRECTS TAKE 67.77% OF COMPETITIVES

- US TSY 26W BILL AUCTION: BID/CVR 3.17