POWER: German Coal Use from Reserve Could Weigh on Gas Demand

Mar-13 09:34

The increased use of Germany coal power plant reserve may weigh on German gas-fired generation next winter.

- Germany plans to use its power plant under the reserve not only for bottlenecks but also to stabilise power prices, it said in exploratory talks document from future coalition partners CDU and SPD.

- Germany currently has 6.4GW of coal power plants in the reserve with 2.7GW slated for closure in 2027 according to BNEF.

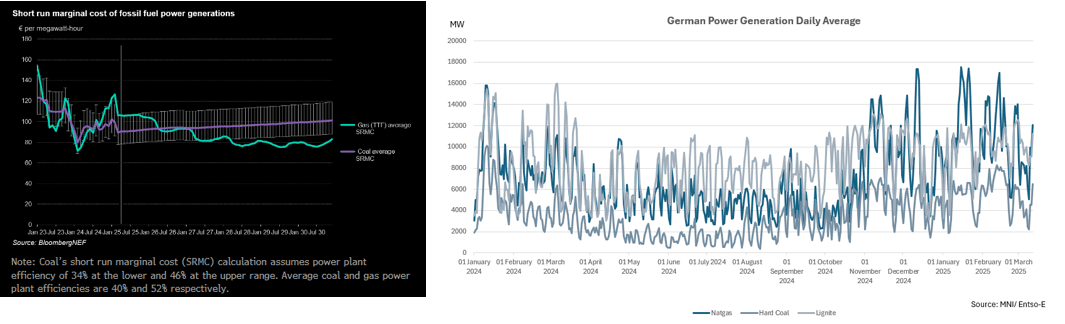

- However, BNEF’s SRMC model suggests costs for German gas-fired plants will fall below costs of coal plants from mid next year (see chart).

- Increased coal-fired generation in Germany would be a relieve, with German gas inventories currently well below seasonal averages.

- Germany’s natural gas inventories stood at 31.45% as of 11 March, well below the five-year normal of 51.76%, GIE data showed.

- German gas-fired power generation averaged 8.26GW so far this month, well above the 4.27GW of coal burn and but below the 9.93GW of lignite power generation.

- The paper between two parties also suggested Germany is planning to build up to 20GW of new gas-fired power plants by 2030.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITIES: EU Bank call option trade

Feb-11 09:33

SX7E (20th Jun) 175c, bought for 2.90 in 6k.

NORWAY: Offsetting Productivity and Compensation Impacts From Q4 GDP Report

Feb-11 09:28

The Q4 GDP print had mixed implications for the March MPR rate path from an income/productivity perspective. Although mainland real productivity per hour growth was -0.5% Q/Q (vs 0.5% prior), annual wage growth was below Norges Bank’s December MPR projection at 5.0% Y/Y (vs 5.2% forecast, 5.7% prior).

- Whole-economy employment growth was 0.2% Q/Q (in line with the Q4 Regional Network Survey) and 0.6% Y/Y (in line with the December MPR projection). Meanwhile, hours worked grew 0.1% Q/Q on a whole-economy and mainland basis.

- These productivity, compensation and hours worked dynamics have offsetting impacts on overall unit labour cost growth.

- The weak productivity reading takes some of the shine off last quarter’s upward productivity revisions going back to 2022, but we don’t want to overstate its impact. We noted earlier that headline GDP weakness (-0.6% Q/Q) was largely due to a pullback in inventory investment, and a good deal of that would’ve bled into the mainland GDP reading too (and thus weigh on productivity growth).

- Taken alongside the GDP expenditure breakdown covered earlier, with think the Q4 GDP report should still be a dovish factor in the March MPR rate path. Governor Wolden Bache will likely reaffirm guidance for a 25bp March cut at her annual address on Thursday.

CROSS ASSET: New session lows for Bond Futures

Feb-11 09:27

- New lows for the Bund, and German Govie futures lead the way to the downside, Supply Delta hedging needs has been weighing since the Cash open.

- Tariffs announcement has also played its part, although the move in the US Treasuries lags, with the 109.01 level still holding in TYH5, this was the Post NFP printed low.

- As noted on the Bund open, 132.95 is the first downside hurdle, the NFP printed low, but better support is seen at 132.72.

- The move in Yields could keep the USDJPY underpinned.

Related bullets

Related by topic

Energy Data

US Natgas

TTF ICE

Asia LNG

Gas Positioning

Germany