AUSSIE BONDS: Futures Lower But Above Key Support Ahead Q3 CPI Print

Aussie bond futures are tracking with a modestly softer bias in early trade, as markets await the Q3 CPI (and monthly CPI print) later. RBA easing expectations for Nov have been pared, now around 9bps priced in (roughly 36% chance of a cut). We did have 16bps priced in at the end of last week. Given recent market shifts we could see greater reaction today to a dovish CPI outcome rather than a hawkish one.

- The Q3 trimmed mean is expected to rise 0.8% q/q leaving annual inflation stable at 2.7% y/y. A 2.5%y/y print is likely needed to re-ignite Nov easing prospects. A 2.6%y/y print could deliver an easing in Nov (if services inflation is supportive) as this was the Q4 RBA forecast made in Aug. A 2.8%y/y for trimmed mean or higher may reduce Nov easing chances back to flat.

- 3yr futures (YM) were last 96.525, (off 1.5bps), slightly underperforming the 10yr (XM) (last near 95.8050). Levels wise we are still some distance from important support for the 3yr (96.28, May 15 low), through late Sep/early Oct, dips under 96.40 were supported. On the upside, recent highs were marked at 96.70.

- Cash ACGB yields are up a little over 1bps across the benchmarks, the 3yr up to 3.46%, as it re-establishes a likely 3.40-3.60% range. The 10yr around 4.18%.

- The 3/10s curve is holding just under 72bps, while the AU-US 10yr spread is pushing up towards +21bps, eyeing another +30bps test.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUD: AUD/USD - Finds Buyers Towards 0.6500 As The USD Move Stalls

The AUD/USD had a range overnight of 0.6521-0.6552, Asia is trading around 0.6550. US stocks found some support and the USD’s bout of strength stalled as the data on Friday came in as expected. The AUD found some demand back towards the 0.6500 area and is trying to bounce. Price is back in the range and the market will be turning its attention towards Fridays Payroll number if it is released. The AUD outperformance continues to be better expressed in the crosses for the time being.

- MNI RBA WATCH: On Hold, Eyeing Further Labour, CPI Data. The Reserve Bank of Australia board is likely to hold the cash rate at 3.6% tomorrow as it considers the floor of its easing cycle and awaits clearer signals on inflation and labour market tightness, making a November cut a possibility. Former RBA officials argue that a tight labour market, weak productivity, and strong wage growth could limit the Bank to just one or two more cuts, with the risk tilted toward one. They agree labour market performance will be central to the Bank’s next steps.

- Bloomberg - “Trump will meet the top four congressional leaders at the White House Monday as an Oct. 1 shutdown looms. The US will still continue to collect tariff revenue and pursue its immigration crackdown if the government closes.”

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6550(AUD405m), 0.6625(AUD1.29b), 0.6725(AUD1.19b). Upcoming Close Strikes : 0.6600(AUD943m Oct 1), 0.6600(AUD1.57b Oct 2), 0.6700(AUD1.64b Oct 1) - BBG

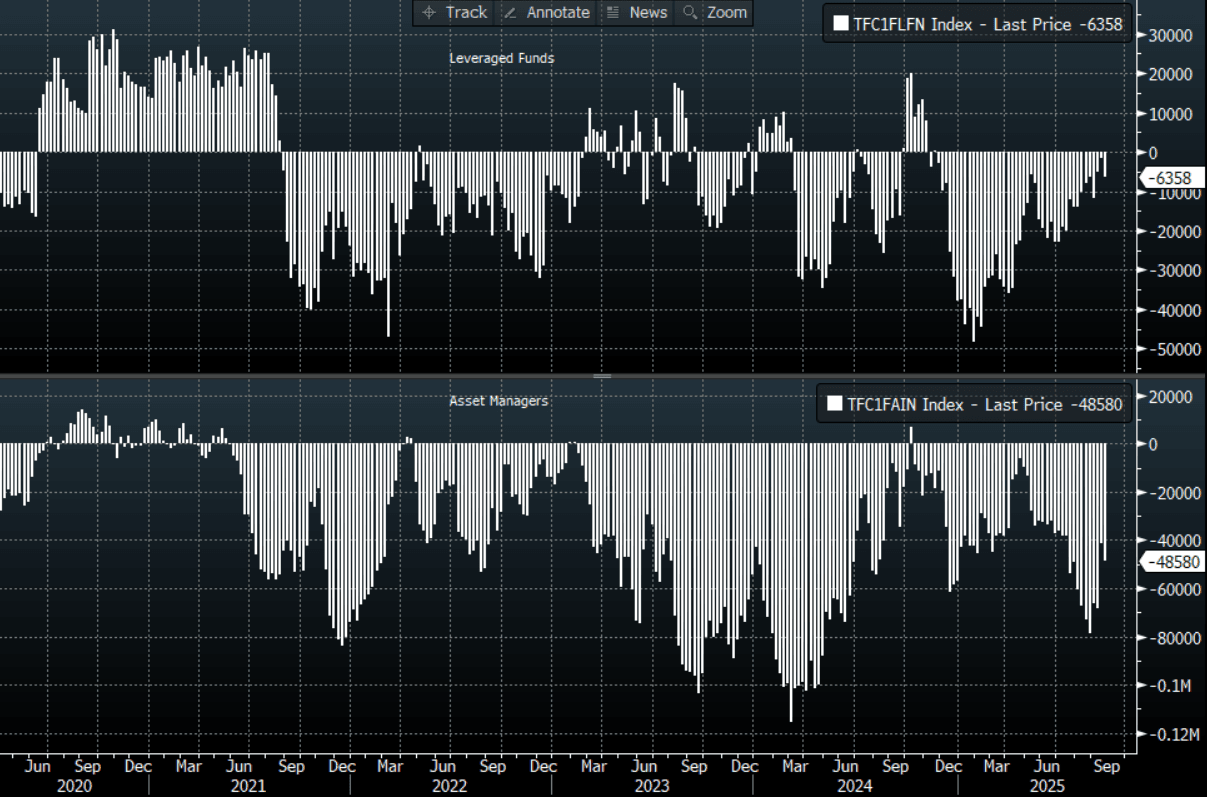

- CFTC Data last week shows Asset managers added back to their recently reduced shorts, -48580(Last -41095). The Leveraged community did likewise, -6358(Last -1519).

Fig 1: AUD CFTC Data

Source: MNI - Market News/Bloomberg Finance L.P

US TSYS: Yields End Mixed, Attention Turns Toward Payroll Data This Week

TYZ5 reopens at 112-10+, up 0-02 from closing levels in today’s Asia-Pac session.

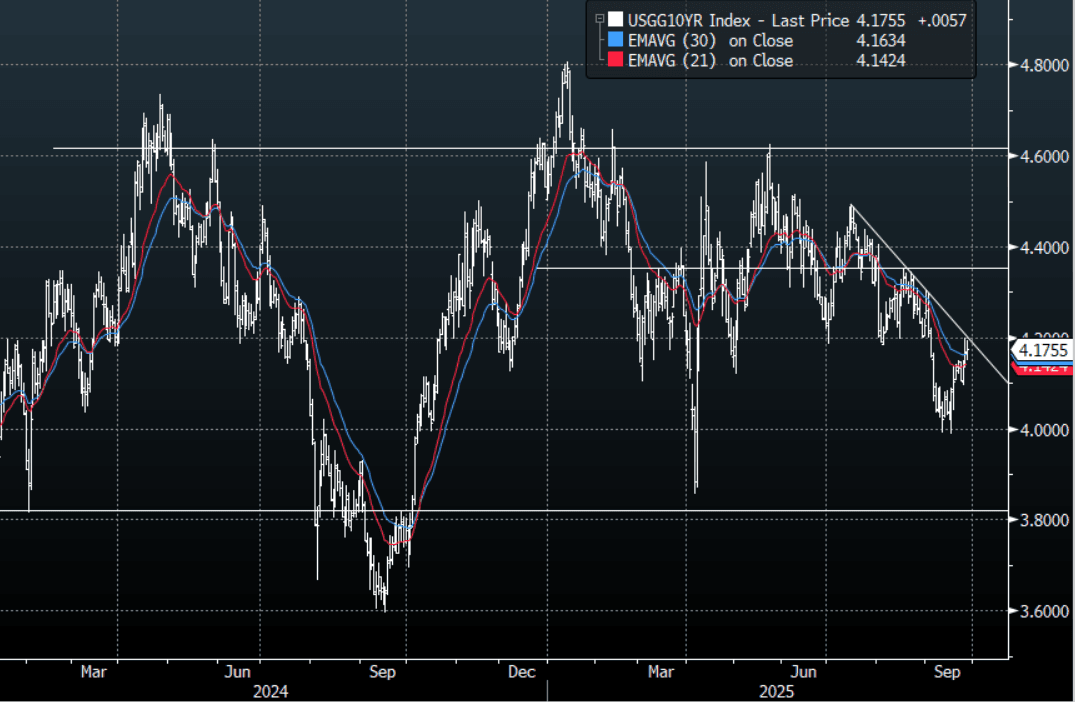

- Friday night the US 10-year yield had a range of 4.1503% - 4.1949%, closing around 4.175%.

- Treasury yields ended mixed on Friday night; (2s10s +1.80 at 53.048, 5s30s -4.55 at 98.616).

- 10-Year yields persisted with its probe of the 4.20% area, I suspect buyers continue to be should be around 4.20% initially and look to fade the move higher. The jobs data if released will be key this week. A move back above 4.35%/4.40% is needed to negate the downtrend.

- MNI FED: Bowman Advocates Fed Take More Forward-Looking Approach.Federal Reserve Governor Miki Bowman on Friday said the Fed should place more emphasis on a proactive forward-looking approach and down-weight the latest data points, repeating that the Fed must act "decisively and proactively" to address increasingly fragile labor market conditions.

- MNI US DATA: Core PCE Inflation Steady In August, Supercore M/M Stays Elevated. August's core PCE reading of 0.227% M/M was basically exactly in line with expectations (0.22% MNI median), and came with a downward revision to July's figure (now 0.235%, was (0.273%). That marks the slowest monthly M/M print in 4 months.

Fig 1: 10-Year US Yield Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P

NEW ZEALAND: Monthly Data May Shape OCR Expectations

This week will provide more information on how NZ’s recovery tracked in Q3. The higher frequency data have been the focus of the RBNZ for over a year and so should help shape expectations for the 8 October RBNZ decision where some are forecasting a 50bp rate cut following the very weak Q2 GDP print.

- The ANZ business survey for September is released on Tuesday. The activity assessment compared to a year ago is an important signal for GDP in the quarter. Business confidence and the activity outlook are off the May lows, following the announcement of US tariffs, but remain below the Q4 2024 peak. The price/cost components are also important to monitor.

- On Wednesday, August building permits print. They rose 5.4% m/m in July but the construction sector as a whole has been weak for some time.

- Cotality home values for September are scheduled to be released between October 1 and 10. August was the fifth consecutive monthly decline in house prices, which may be weighing on consumer confidence.