AUSSIE BONDS: Front End Yields Lower, AOFM Lowers 2025-26 Bond Issuance F/C

The early bias in Aussie bond futures is firmer, led by the 3yr. YM was was up around 3.5bps to 95.83, while the 10yr (XM) has ticked up 1.5bps to 95.21. This keeps us within recent ranges. A short while ago the AOFM lowered its estimate for 2025-2026 bond issuance to A$125bn, from A$150bn (with this estimate made back in the middle of this year). Note CBA had stated markets expected around A$130bn in issuance (via BBG) ACGB yields are lower, led by the front end. The 3yr last off close to 4bps to 4.08%, while the 10yr is down nearly 2bps, last near 4.725%. For both benchmarks we are close to the mid-point of Dec ranges seen so far this month.

- US Tsy futures see-sawed off early Wednesday lows to steady/mixed in late trade, focus on Thursday's heavy data (weekly claims, CPI, regional Fed and Tsy TICS) and Riksbank, Norges, Bank of England and ECB policy announcements.

- Equity market sentiment was negative in the US, which may be aiding at the margin the early Aussie bond futures bid.

- The AU 3/10s curve is slightly steeper at +64bps.

- The AU-US 10yr spread is consolidating near recent highs, last at +59bps.

- Note on the data front today we have Dec consumer inflation expectations (the prior outcome was 4.5%).

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

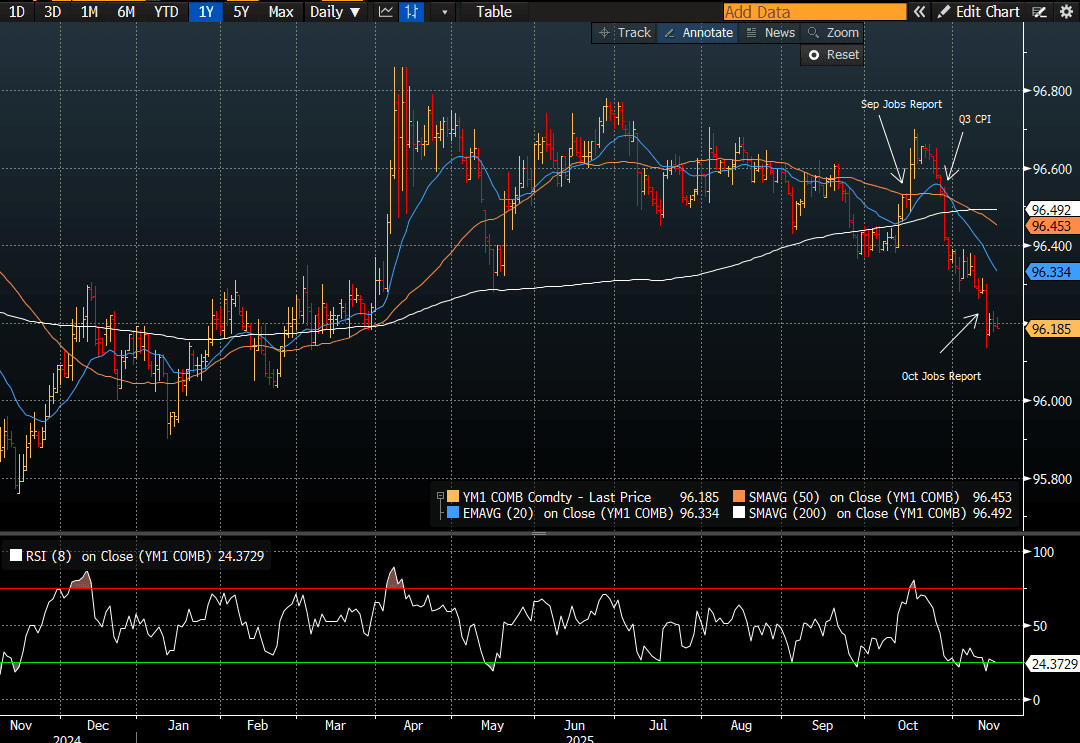

AUSSIE 3-YEAR TECHS: (Z5) Struck by Strong Jobs

- RES 3: 97.796 - 1.618 proj of the Sep 3 - 12 - 15 price swing

- RES 2: 96.780 - High Jun 26 (cont)

- RES 1: 96.700 - High Sep 12

- PRICE: 96.200 @ 15:48 GMT Nov 17

- SUP 1: 96.135 - Low Nov 13

- SUP 2: 95.900 - Low Jan 14 (cont.)

- SUP 3: 95.760 - Low 14 Nov ‘24

Prices slid sharply on the better-than-expected jobs data, pushing prices through first support at 96.280. This makes for a fresh contract low, exposing 95.900 on the continuation chart for direction. The slower pricing for additional RBA easing should keep the front-end of the curve under pressure. This keeps prices well below prior resistance at 96.615, the Sep 12 high, and refocuses attention on 95.900 as the next major support.

AUSSIE BONDS: Little Changed, Subdued Start To Week For US Tsys, Jun-54 Supply

ACGBs (YM -1.0 & XM -0.5) are little changed in line with cash US tsys Monday’s close.

- YM1 technicals continue to point to further weakness. (see chart)

- Fed Vice Chair Jefferson said he's likely one of the 9 FOMC members who anticipated cutting rates in Sep, Oct and Dec (in his September Dot Plot) and if forced to guess we would think he is still marginally in favor of a December cut and here he again highlights "increased downside risks to employment compared to the upside risks to inflation, which have likely declined somewhat recently".

- Cash ACGBs are little changed with the AU-US 10-year yield differential at +34bps.

- The bills strip is unchanged across contracts.

- RBA-dated OIS pricing is showing a 25bp rate cut in December at a 2% probability, with a cumulative 10bps of easing priced by mid-2026.

- Today, the local calendar will see RBA Minutes of the Nov. Policy Meeting ahead of the Wage Price Index on Wednesday.

- This week, the AOFM plans to sell A$300mn of the 4.75% 21 June 2054 bond today, A$1000mn of the 2.75% 21 June 2035 bond on Wednesday and A$700mn of the 1.25% 21 May 2032 bond on Friday.

Bloomberg Finance LP

CNH: Near 7.1100 On broader USD Gains, But CNH/JPY Breaks Higher

USD/CNH probed above 7.1100 amid broader USD gains as Monday trade unfolded, but there was no follow through. We track near 7.1090 in early Tuesday dealings, after losing a little over 0.10% for Monday's session. Upside focus will rest with the 20-day EMA at 7.1165, then the 50-day near 7.1270. For now, the pair looks to have found a base ahead of the 7.0900 level as broader USD sentiment stabilizes. US Tsy yields were little changed on Monday, with some Fed speak in support of a Dec rate cut (notably Waller). US equity sentiment was softer.

- USD/CNH gains were more modest than broader USD index gains on Monday, with the BBDXY index up around 0.30%, the DXY +0.25%. Spot USD/CNY finished up at 7.1077, while the CFETS basket tracker was at 97.80, little changed for the session.

- CNH/JPY broke higher (as USD/JPY rallied through 155.00) to 21.8440 and we track just below this level currently. Upside focus will rest on a test above 22.00. Focus today will be on a meeting between BoJ Governor Ueda and new PM Takaichi, amid signs of tension between the government and BoJ around potential hike timing.

- With the USD/CNY fixing bias still pointing to yuan gains/resilience we would expect CNH to continue to outperform broader USD gains.

- Local equity market sentiment may remain under pressure amid broader global tech concerns. The Golden Dragon index lost a further 1.21% in US Trade on Monday.

- On the data front, we should get Oct FDI figures today. Yesterday, the FX settlement ratio for Oct eased back to 62.9% from 71.2% in Sep.