AUSTRALIA DATA: Employment Weakens But Forward Orders Improve

NAB business confidence continued to oscillate around zero in May as it has done for around two and half years. It printed at +1.9 after -0.9 in April, the highest since January. However, conditions carried on their downtrend reaching 0.3 in May following 1.6, the lowest since the Covid-impacted August 2020. Q2 average confidence is suggesting a stabilisation in annual growth in the quarter but conditions suggest it will slow.

Australia NAB business survey vs GDP y/y%

- Business conditions were driven down by employment and trading. Profitability was stable. In terms of the outlook, forward orders improved to -1.8 from -3.0, the best since October 2023. Given heightened global uncertainty, there was good news on the export front with both current and sales rising in May to their highest since December.

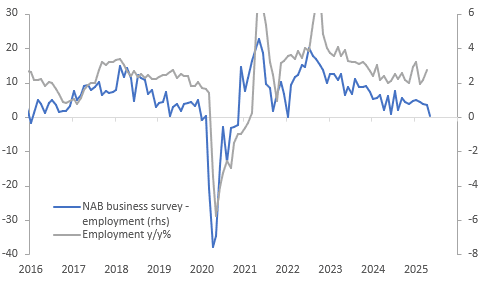

- Labour demand fell to 0.4 in May from 3.6, the lowest since January 2022. The trending down over this year is suggesting that employment growth is likely to slow. May data prints on June 19.

Australia employment

Source: MNI - Market News/LSEG/ABS

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

MACRO OUTLOOK: US PPI/Retail Sales And Powell Follow On Thursday [2/2]

- Core PCE implications will then be watched closely in Thursday’s PPI report, and we expect with additional focus on portfolio management after last month’s huge upward revision to February.

- Retail sales, whilst only reported in nominal terms, will offer a keenly awaited look at consumer behavior.

- Real spending moderated to 1.8% annualized in Q1 after 4.0% in Q4 despite likely tariff front-running, with April a good test of how much discretionary spending was pulled forward.

- Finally, Powell provides “Opening Remarks” at the Second Thomas Laubach Research Conference, although he’s allotted twenty minutes so there is scope for more substantive remarks than you’d usually expect. His message at Wednesday’s FOMC press conference was one firmly of being in no hurry to cut rates amidst huge uncertainty. He also appeared to put more weight on hard data over soft indicators that appear more stagflationary in nature.

MACRO OUTLOOK: US CPI Offers Look At April Tariff Distortions on Tuesday [1/2]

- The week’s US data calendar is highlighted by CPI inflation on Tuesday although PPI inflation and retail sales reports on Thursday are in close second. All three releases are going to be important, offering further hard data for April in the first month under reciprocal tariffs. What’s more, PPI and retail sales are followed by Fed Chair Powell just ten minutes after their release (more on that below).

- Core CPI inflation is seen accelerating to 0.3% M/M in April, with six unrounded estimates we’ve seen to date averaging 0.27% M/M.

- A potential for a ‘low’ 0.3% aside, it’s still likely a swift acceleration from a particularly soft 0.06% M/M in March which was in large part down to surprisingly abrupt declines in lodging away from home (-3.5%) and airfare (-5.3%) prices.

- This lodging weakness carried over to core PCE inflation back in March, at just 0.03% M/M after a particularly strong 0.50% M/M in February in a large wedge with core CPI at 0.23% M/M.

- Markets currently price a next Fed cut with the September FOMC meeting.

USDCAD TECHS: Pressuring Resistance

- RES 4: 1.4296 High Apr 7

- RES 3: 1.4111 High Apr 4

- RES 2: 1.4041 50-day EMA

- RES 1: 1.3943 High May 9

- PRICE: 1.3930 @ 16:06 BST May 9

- SUP 1: 1.3751 Low May 6

- SUP 2: 1.3744 76.4% retracement of Sep 25 ‘24 - Feb 3 bull run

- SUP 3: 1.3696 Low Oct 10 2024

- SUP 4: 1.3643 Low Oct 9 ‘24

USDCAD has recovered from its recent lows. Despite the recovery, the trend condition remains bearish and short-term gains are considered corrective. A fresh cycle low on Tuesday reinforces the bearish theme. Potential is seen for a move towards 1.3744, a Fibonacci retracement. Note that moving average studies are in a bear mode position, highlighting a dominant downtrend. Key resistance is seen at 1.4041, the 50-day EMA.