ECB: ECB Accounts Watched For Growth and Inflation Risk Assessment Colour

The ECB accounts of the Oct 29-30 meeting will be published ahead at 1230GMT/1330CET. Some areas we’ll be watching include:

- The extent of discussions around the decision to not describe risks to growth as “more balanced” (per September language) or “balanced” at all, with Lagarde instead highlighting that some downside risks had abated. Recall that the change to this risk assessment was acknowledged as preventing the ECB from repeating “more balanced” ad nauseum, despite it only having been introduced at the last meeting prior to which growth risks were tilted to the downside.

- Any notable divisions specifically as policymakers looked ahead to the fresh round of economic projections due with the December meeting. The Reuters post-meeting sources piece described December as “something of a showdown” as policymakers remain sensitive to a continued undershoot in inflation projection. However, subsequent ECBspeak suggests it might be less contentious now.

- The extent of discussions around some additional upside risks to inflation, including supply chain pressures, which as Lagarde added didn’t make it to the written statement (with its multiple two-sided risks – deemed too many to net out in the accounts of last month’s meeting). Whilst bringing them up, she Lagarde also noted that these have not yet materialised.

ECB-dated OIS only prices 9bp of cuts ahead, broadly reached in June with then little change towards year-end. A combination of resilient growth signals and fairly cautious ECBspeak have factored into the post-meeting repricing, even with some Governing Council members still cognizant of downside inflation risks in the medium term.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

OUTLOOK: Price Signal Summary - Fresh Cycle High In Gilts

- In the FI space, Bund futures are trading closer to their recent lows. The bear phase that started on Oct 17 is considered corrective and is allowing an overbought trend condition to unwind. Initial key support at 129.45, the 20-day EMA, has been breached. This exposes the 50-day EMA, currently at 129.08. For bulls, a reversal would refocus attention on the key resistance at 130.59, the Oct 17 high.

- A bull cycle in Gilt futures remains intact. The recent clearance of 93.17, the Oct 17 high, and a fresh cycle high high today, confirms a resumption of the uptrend and signals scope for an extension towards the 94.00 handle next and 94.24, a 1.618 projection of the Sep 3 - 11 - 26 price swing. Moving average studies are in a bull-mode position, highlighting a dominant uptrend. Note that the contract is overbought, a pullback would allow this condition to unwind. Firm support to watch lies at 92.27, the 20-day EMA.

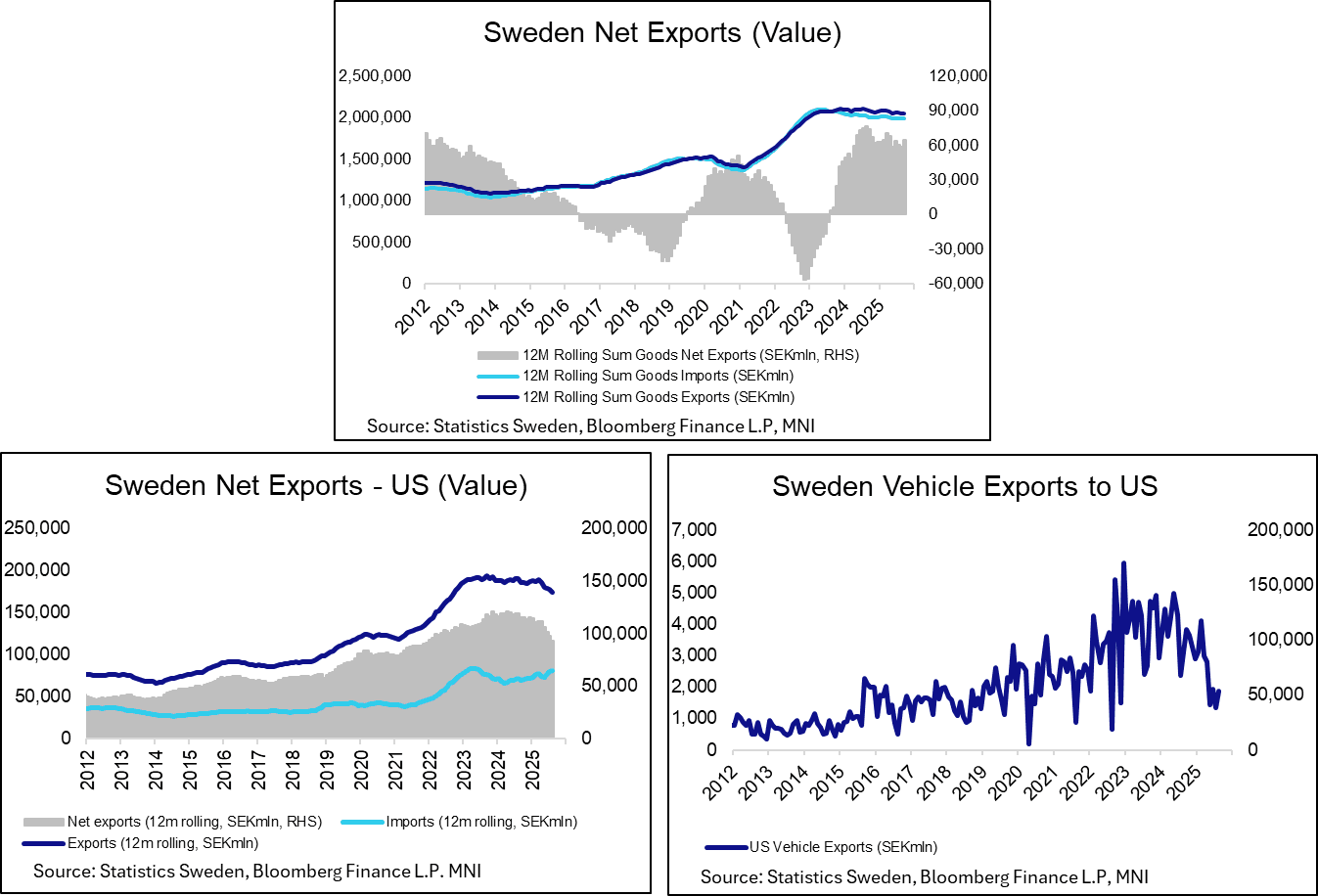

SWEDEN: US Tariffs Having A Direct Impact On Swedish Exports

Although trade/tariff policy uncertainty has moderated from the extremes seen earlier this year, US tariffs are clearly having a direct impact on Swedish exports. In August, total exports to the US were SEK8.9bln, the lowest single-month reading since August 2021. 12-month rolling exports have also fallen in each month since March 2025.

- Vehicle exports to the US have fallen noticeably since March. The Riksbank’s Q3 Business Survey (released this morning) cited weaker US demand for new vehicles as a significant drag on the automotive industry.

- Total net exports were SEK5.4bln in September. On a 12-month rolling basis, net exports totalled SEK64.7bln, up from SEK59.1bln in August.

- Volume indices are only available as of August. The import volume index has been steady at 126 for four consecutive months now, while the export volume index ticked up to 131 after seven months stuck at 130. On a sequential basis, this suggests a broadly neutral contribution from net goods trade to Q3 GDP so far. A reminder that Q3 flash GDP is due tomorrow morning.

- The Riksbank’s Business Survey also highlighted that US tariffs have increased costs for some businesses: “Others describe how costs have increased as a result of increased regionalisation. For example, some companies have had to move their production from China to Europe, where it is generally more expensive to produce the same product. Companies also state that imports to Sweden have become more expensive. Among others, they mention construction materials, aluminium and some input goods. Costs are also expected to continue to rise in the future as a result of the tariffs. “In our fourth quarter, we will see almost the full impact of the tariffs in our costs,” explained one business leader".

BUNDS: Bund vs Schatz Swap related trade

- RXZ5 ~2.22k at 129.65 (suggest Payer).

- DUZ5 10.83k at 107.07 (suggest Receiver).