ECB: ECB Accounts: Very Difficult To Net Out Balance Of Inflation Risks

The ECB accounts from the Sep 10-11 meeting also highlight an array of two-sided risks to the inflation outlook, with it being "very difficult" to net them out. As for medium-term risks, there were arguments made from Governing Council members at either side of the hawk-dove spectrum: the characterisation of "several" viewing risks tilted to the downside and "a few" to the upside is the same as the accounts from the July meeting.

- On inflation risks: “risks surrounding the inflation outlook were identified on both sides. This assessment was also supported by staff risk, sensitivity and scenario analyses. There were multiple upside and downside risks to inflation, and while any overall assessment was a matter of judgement, it was very difficult to net all the factors out into strong balance of risk statements.”

- Dovish view: “Several members viewed inflation risks as tilted to the downside over the medium term. From this perspective, the appreciation of the euro had been a genuinely exogenous shock unrelated to euro area economic conditions, and it could have a larger effect on inflation than included in the projections. Further appreciation was also possible given increasing expectations of interest rate cuts by the Federal Open Market Committee in the United States. It was also argued that trade tensions and uncertainty still posed downside risks to inflation. In particular, it was suggested that intensifying re-routing of goods to the euro area, from China and other countries with overcapacity, could manifest itself in lower export prices and result in lower inflation. These effects were likely larger than any upward risks from supply chain disruptions.”

- Hawkish view: “A few members viewed inflation risks as tilted to the upside over the medium term, also noting that external forecasts for inflation in 2026 and 2027 stood above the latest staff projections. While monetary policy had supported the disinflationary process, the decline in inflation back to target could also partly be attributed to volatile developments in energy prices and the exchange rate, which could easily reverse. In addition, the pass-through from lower input costs linked to a stronger exchange rate or falling import prices might be smaller than assumed in the projections, as importers might be less willing to pass on lower costs to consumers owing to downward price rigidities, especially given robust domestic demand and the appetite of firms to rebuild their profit margins.”

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

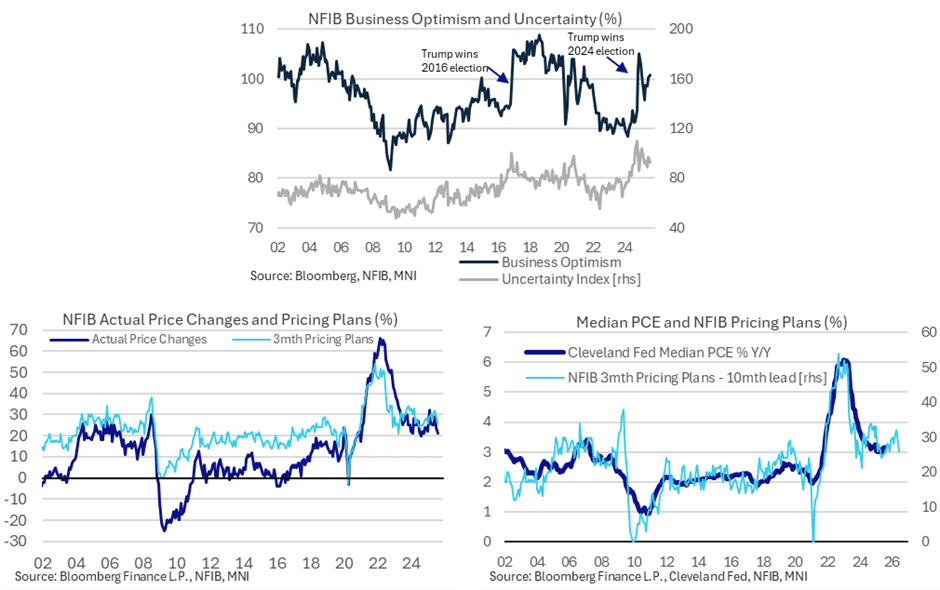

US DATA: Small Businesses Imply Largest Tariff Price Increases Have Passed

Small business optimism continued its improvement from lows seen after April tariff announcements in August. Both backward- and forward-looking price metrics pulled back further after some recent increases although a longer-term trend remains one at a level above that consistent with the 2% inflation target.

- The NFIB small business optimism index firmed slightly more than expected in August as it ticked up to 100.8 (cons 100.5) from 100.3 in July for technically its highest since January.

- It extends what has been a trend recovery from the 95.8 seen after reciprocal tariff announcements in April. For context, the index saw a recent high of 105.1 in December, fully reflecting US election results, an average of 93 in 2024 and a very long-term 52-year average of 98.

- Ahead of Thursday’s US CPI report for August, the net share who increased prices compared to three months ago fell for a second month to 21% (lowest since Oct 2024) vs 29% in Jun and a recent high of 32% in Feb.

- It’s below the 23% averaged in 2024 but remains above pre-pandemic averages of ~12%.

- Also on the softer side, the net share expecting to increase prices over the next three months fell for a second month to 26%, the joint lowest since Sep 2024, having recently peaked at 32% in June.

- It’s back below the 28% averaged in 2024 but remains above the 22% averaged pre-pandemic.

- The two price metrics therefore point to some cooling in price pressures after an initial firming in the early stages of the second Trump administration, although from a longer-term trend perspective they continue to point to some stabilization at level above those historically consistent with 2% inflation.

OUTLOOK: Price Signal Summary - USDJPY Support Remains Exposed

- In FX, the trend theme in EURUSD remains bullish. This week’s move higher reinforces current conditions and confirms a clear breach of 1.1743, the Aug 22 high. This highlights a short-term bullish development and signals scope for an extension towards 1.1829, the Jul 01 high and bull trigger. Support to watch is around the 50-day EMA, at 1.1625. A clear breach of this average would signal scope for a deeper retracement.

- GBPUSD is trading higher today as the pair extends the recovery from the Sep 3 low. The move higher has retraced the steep sell-off on Sep 2 and highlights a stronger bullish development. This also suggests the corrective cycle between Aug 14 - Sep 3 is over. Sights are on resistance at 1.3595, the Aug 14 high and a bull trigger. A break would strengthen a bullish condition. Initial support to watch is 1.3463, the 50-day EMA.

- USDJPY is trading lower as the pair extends the reversal from last week’s 149.14 high on Sep 3. The move down refocuses attention on key short-term support at 146.21, the Aug 14 low and a bear trigger. A break of this level would highlight a stronger bearish threat and expose 145.40, 50% of the Apr - Aug upleg. Clearance of the Sep 3 high is required to reinstate a bullish theme.

US 10YR FUTURE TECHS: (Z5) Bull Cycle Remains In Play

- RES 4: 114-10 High Apr 7 (cont.)

- RES 3: 114-00 Round number resistance

- RES 2: 113-26+ 2.764 proj of the Jul 15 - 22 - 28 price swing

- RES 1: 113-21+ High Sep 5

- PRICE: 113-13+ @ 12:29 BST Sep 9

- SUP 1: 112-28+/112-11+ Low Sep 5 / 20-day EMA

- SUP 2: 111-26+ 50-day EMA

- SUP 3: 111-13+ Low Aug 18 and a key support

- SUP 4: 110-25 Low Aug 1

Treasury futures rallied sharply higher last Friday and the contract remains closer to its recent highs The move higher highlights an acceleration of the uptrend. Note too that moving average studies are in a bull-mode position, highlighting a dominant uptrend. This paves the way for an extension through 113-21 next (pierced), the 2.618 projection of the Jul 15 - 22 - 28 price swing. Initial firm support to watch is 112-11+, the 20-day EMA.