AUSTRALIA: December Jobs Forecast To Rise, Q4 Average Should Be Focus

Jan-18 23:09

The highlight of this week will be December jobs data released on Thursday. Bloomberg consensus expe...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUDUSD TECHS: Corrective Phase Still In Play

Dec-19 21:00

- RES 4: 0.6759 High Oct 11 ‘24

- RES 3: 0.6723 High Oct 21 ‘24

- RES 2: 0.6707 High Sep 17 and a key resistance

- RES 1: 0.6661/86 High Dec 16 / 10

- PRICE: 0.6608 @ 15:56 GMT Dec 19

- SUP 1: 0.6593 Low Dec 18

- SUP 2: 0.6566 50-day EMA

- SUP 3: 0.6517 Low Nov 27

- SUP 4: 0.6466/21 Low Nov 26 / 21

The trend condition in AUDUSD remains bullish and the latest pullback appears corrective. The move down is allowing a recent overbought condition to unwind. Support at the 20-day EMA, at 0.6598, has been pierced. The 50-day average is at 0.6566. The area between the two averages represents a key short-term support zone. A resumption of gains would refocus attention on key resistance at 0.6707, the Sep 17 high and bull trigger.

LOOK AHEAD: US Macro Week Ahead: Long-Awaited Q3 GDP Plus Labor Updates

Dec-19 21:00

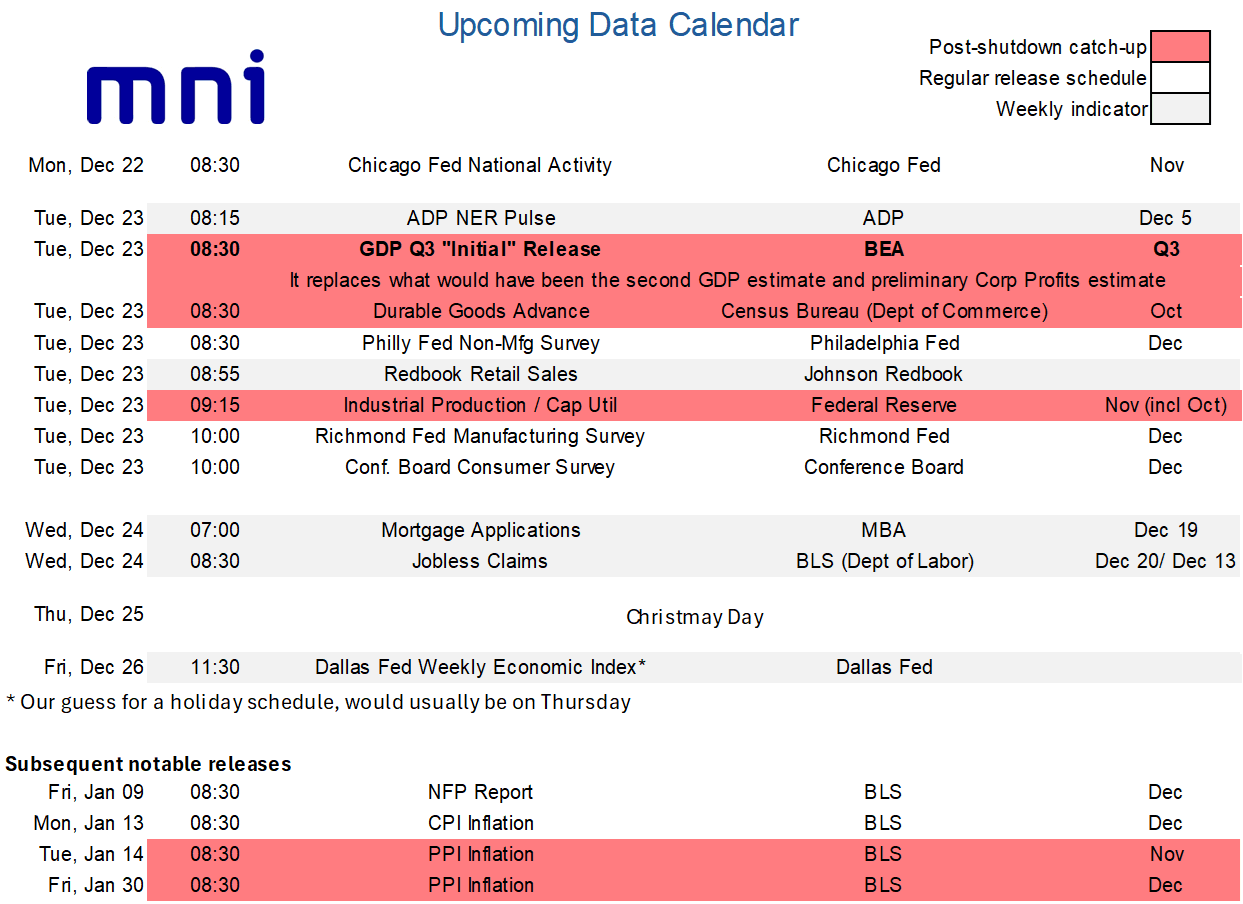

- The week ahead sees a slimmed down data schedule after a particularly busy few weeks, including distorted NFP and CPI reports in the week just gone. There are still some important releases though, with the highlight being the long-awaited “initial” Q3 GDP release on Tuesday.

- This report will replace what would have been the second GDP and the preliminary corporate profits estimates, with the extended tracking window of the Atlanta Fed’s GDPNow pointing to strong real GDP growth of 3.5% annualized after an average 1.6% in 1H25 (-0.65% in Q1 before 3.84% in Q2).

- Expect continued close attention on private demand, best seen by Powell’s preferred PDFP category, which is currently tracking at ~2.4% annualized for similar to the 2.4% averaged in 1H25 (1.9% Q1 before 2.9% in Q2).

- Tuesday also sees updates for the weekly ADP tracker in the four weeks up to Dec 5, getting closer to the reference period for the monthly report, after last week’s further improvement. It’s followed by useful updates for Q4 GDP tracking with durable goods for October and industrial production for both October and November, before the Conference Board consumer survey for December with its closely watched labor differential having stalled at subdued levels but not deteriorated further since September.

- Note as well that Wednesday then sees weekly jobless claims a day early ahead of Christmas Day, with continuing claims capturing the December payrolls reference period. There is currently minimal Fedspeak scheduled and we suspect this will remain the case ahead of Christmas, likely confined to media appearances if any.

MACRO OUTLOOK: MNI US Macro Weekly: More Noise Than Signal From Key Data

Dec-19 20:56

We've just released our weekly US macro publication - Download Full Report Here

- A highly unusual payrolls report saw multiple caveats that drove a swift fade of an initially dovish reaction.

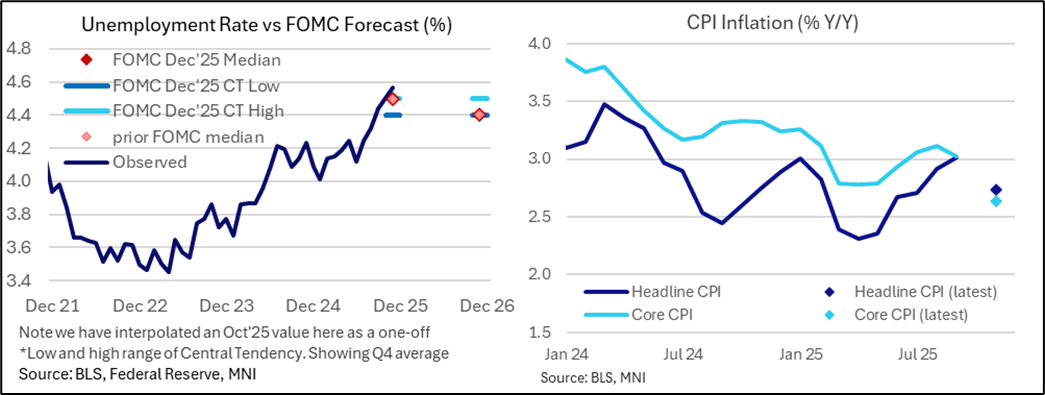

- The highlight was the surprise push higher in the unemployment rate to 4.56% in November from 4.44% in September, with NY Fed’s Williams since estimating it was boosted 0.1pp by distortions.

- Subsequent labor indicators saw initial jobless claims remain at a very healthy level in a payrolls reference week whilst QCEW data suggest downward NFP revisions look on track for Powell's 60k/month estimate.

- Later in the week, the November CPI report was even messier than had been feared coming into its delayed release, leaving several lingering questions in its wake. On the surface, inflationary pressures appeared much softer than expected, but various factors appear to have downwardly biased the readings – and distortions look poised to reverberate for months to come.

- The FOMC will thus interpret these latest inflation readings with extreme caution, using the December CPI report due out before the January meeting to make more sense of underlying price dynamics.

- Elsewhere, core retail sales started Q4 with strong momentum but with more recent indicators somewhat mixed since then. Real GDP growth tracking for Q3 has been trimmed a little further but remains robust with GDPNow at 3.5% ahead of Tuesday’s long-awaited update.

- Business surveys meanwhile came in softer, including flash PMIs and regional Fed manufacturing for Dec.

- NEC’s Hassett remains a firm favorite for the next Fed Chair role despite reports of pushback from Trump officials in CNBC and Politico reporting. Trump expects to announce his pick in the next couple weeks.

- Speaking after CPI, NY Fed’s Williams signalled little urgency for a January cut after messy data (noting CPI looked understated) though Chicago Fed’s Goolsbee (next voting 2027) saw a “lot to like” in the November CPI report.

- Speaking after payrolls but before CPI, Gov. Waller sees the Fed being 50-100bp above neutral, noting that faster GDP growth isn’t inflationary amid supply side improvements.

- Next week sees a holiday-shortened calendar, highlighted by delayed Q3 GDP data along with durable goods orders/industrial production and various labor updates.

- A next Fed cut remains fully priced for the June FOMC under a new Fed Chair but has drifted closer to being fully priced for April (22bp currently). There is just 5bp of cuts priced for January and we suspect it will be difficult to materially shift from here until the December NFP and CPI reports on Jan 9 and 13.