AUSTRALIA DATA: Core Inflation Moderating Towards Band Mid-Point

Jul-30 02:18

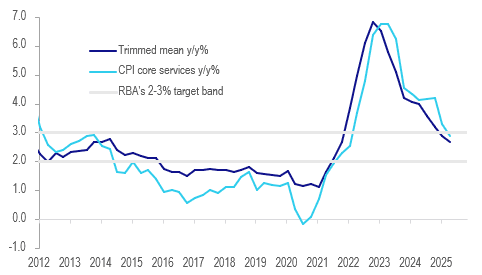

Australia’s Q2 trimmed mean CPI printed only 0.1pp above the RBA’s May Q2 forecast, which with the economy developing broadly in line with expectations since the July meeting should allow it to ease 25bp on August 12 when it also releases its updated outlook. Trimmed mean rose 0.6% q/q to be up 2.7% y/y, a moderation from Q1’s 0.7% & 2.9%.

Australia CPI y/y%

Source: MNI - Market News/LSEG

- The RBA assumed another 50bp of easing in H2 2025 in its May projections which resulted in underlying inflation close to the band mid-point at 2.6% in Q4. The Q2 CPI data should give the Board confidence that this can be achieved resulting in 25bp of that easing in August.

- Importantly services inflation continued to moderate after its 2024 stickiness. In Q2 it fell 0.4pp to 3.3% y/y while core services eased 0.4pp to 2.9%, the lowest since Q1 2022 and within the band, due to easing rental and insurance inflation. Non-tradeables was more stable at 3.1% y/y (-0.1pp). The RBA should be reassured that domestically-driven inflation is finally contained.

- Goods and tradeables inflation remain low and moderated further to 1.1% y/y (-0.2pp) and 0.2% y/y (-0.7pp) respectively.

- Headline CPI, which is still distorted by government electricity rebates, rose a less-than-expected 0.7% q/q and 2.1% y/y after 0.9% & 2.4% in Q1.

- The ABS cites housing as one of the main drivers of the quarterly CPI increase. It rose 1.2% q/q due to electricity prices +8.1% q/q due to rebates being used in Q1. Electricity is still down 6.2% y/y.

- Annual new dwelling and rental inflation continued to moderate at 0.7% and 4.5% respectively.

- Food prices rose 1.0% q/q due to fruit & veg +4.3% q/q. Health rose 1.5% q/q driven by annual insurance increase.

- Transport fell 0.7% q/q due to lower global crude driving auto fuel prices down 3.4% q/q.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

CANADA: Canada To Rescind Digital Services Tax To Aid Trade Talks

Jun-30 02:18

Headlines have crossed that Canada will rescind its digital services tax in order advance trade talks with the US.

- Bloomberg notes: "- Canadian Minister of Finance and National Revenue François-Philippe Champagne says that Canada would rescind the Digital Services Tax in anticipation of a mutually beneficial comprehensive trade arrangement with US, according to a statement."

- Other headlines indicate that trade talks will resume, with a dealing looking to be reached by July 21 between the two countries.

- This follows Trump's announcement towards the end of last week that trade talks between the two countries would be ended due to the digital services tax.

- USD/CAD is down modestly on these headlines, last near 1.3670. Session highs today were at 1.3700.

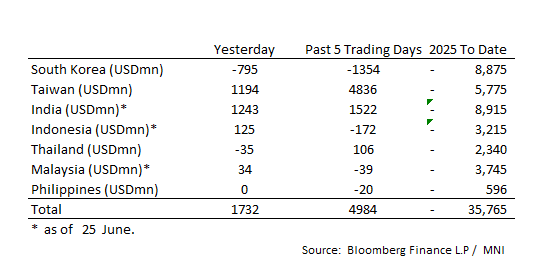

ASIA STOCKS: Taiwan Inflows Continue as India Follows

Jun-30 02:16

Taiwan has $5.1bn of Inflows in Four Trading Days.

- South Korea: Recorded outflows of -$795m Friday, bringing the 5-day total to -$1,354m. 2025 to date flows are -$8,875. The 5-day average is -$271m, the 20-day average is +$110m and the 100-day average of -$87m.

- Taiwan: Had inflows of +$1,194m Friday, with total inflows of +$4,836 m over the past 5 days. YTD flows are negative at -$5,775. The 5-day average is +$967m, the 20-day average of +$256m and the 100-day average of -$45m.

- India: Had inflows of +$1,243m as of the 26th, with total inflows of +$1,522m over the past 5 days. YTD flows are negative -$8,915m. The 5-day average is +$304m, the 20-day average of +$51m and the 100-day average of -$21m.

- Indonesia: Had inflows of +$125 as of the 26th with total outflows of -$172m over the prior five days. YTD flows are negative -$3,215m. The 5-day average is -$34m, the 20-day average -$20m and the 100-day average -$30m.

- Thailand: Recorded outflows of -$35m yesterday, with inflows totaling +$106m over the past 5 days. YTD flows are negative at -$2,340m. The 5-day average is +$21m, the 20-day average of -$32m and the 100-day average of -$21m.

- Malaysia: Recorded inflows as of +$34m as of 26th, totaling -$39m over the past 5 days. YTD flows are negative at -$3,745m. The 5-day average is +$2m, the 20-day average of -$23m and the 100-day average of -$21m.

- Philippines: Recorded no flows Friday, with net outflows of -$20m over the past 5 days. YTD flows are negative at -$596m. The 5-day average is -$4m, the 20-day average of -$18m the 100-day average of -$5m.

CANADA SAYS RESCINDING DIGITAL TAX TO ADVANCE US TRADE TALKS

Jun-30 02:12

- CANADA SAYS RESCINDING DIGITAL TAX TO ADVANCE US TRADE TALKS

- FINANCE MINISTER SAYS TRUMP, CARNEY AIM FOR DEAL BY JULY 21