AUSTRALIA DATA: Core & Services Inflation Pick Up, RBA On Hold

Both the new headline and trimmed mean monthly CPI annual inflation measures saw an increase in October from September. Services also rose which is likely to worry the RBA. On the face of it, the data signal that the RBA is on hold for an extended period but both it and the ABS have said that it will take time to assess the trends in the new monthly data and for seasonal factors to emerge. Governor Bullock has said until then it will focus on quarterly CPIs. Q4 is released 28 January.

- Trimmed mean CPI rose 3.3% y/y in October up from 3.2% in September (the partial CPI was 2.8%).

- Services rose 3.9% y/y up from 3.5%, which may be signalling more inflation persistence. It was driven by a 4.2% y/y rise in rents, 5.1% y/y in medical and 7.1% y/y in holiday travel & accommodation.

- Headline CPI was up 3.8% y/y after 3.6% in September (previous September +3.5%). The series continues to be impacted by the timing of government electricity rebates which drove electricity up 37.1% y/y after 33.9%. This increased the housing component to 5.9% y/y from 5.7% and overall goods inflation to 3.8% y/y from 3.7%.

- Food and eating out costs continued to run above 3.0% with the latter impacted by higher labour costs.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

LNG: US Gas Prices Higher Following Trade News

US natural gas has responded to news of a draft US-China trade deal which is expected to be agreed by Presidents Trump and Xi when they meet on Thursday. The agreement includes a year’s delay to China’s rare earths licensing regulations and should mean that the additional 100% US tariff won’t be imposed on November 1. The pullback from a trade war is positive for global energy consumption and the US was the largest LNG exporter in 2024.

- US prices are up 2.3% to $3.38 so far in Monday’s trading but off the initial jump to $3.433. They were little changed on Friday but finished the week up almost 11% on forecasts of cooler weather and thus a pickup in heating demand. Inventories remain ample which should put a cap on prices even with lower temperatures.

- Atmospheric G2 forecasts for the central and eastern US are lower as the month turns but then temperatures should be higher over November 3-7 over the east.

- US lower-48 gas production rose 5.4% y/y on Friday while demand was only 0.1% y/y, according to BNEF data. Flows for LNG rose 1.6% w/w.

- European prices continued range trading last week between EUR 31.365-32.885. On Friday they fell 1.8% to EUR 31.885 but were little changed on the week and up only 1.5% in October.

- The conflict in Ukraine remains a risk to Europe this winter with sanctions tightened on Russia and Europe’s goals of stopping Russian gas consumption by the start of 2027 as well as Russian attacks on Ukraine increasing its demand for global gas supplies. Also, Ukraine continues to target Russian oil & gas facilities.

US TSYS: Bond Yields Higher in Cash Open

The news from the US Treasury secretary that 'Trump's threat of 100% tariffs on Chinese goods "is effectively off the table" has given markets a boost Monday with equities strong and bonds weak. Bond futures are lower with TYZ5 down -06 at 113-08 with volumes light early.

Cash bonds have opened weak with yields +2bps higher across most maturities.

- The US 2-Yr is +2bps at 3.50%

- The US 5-Yr is +2.5bps at 3.63%

- The US 10-Yr has consolidated further above 4.00% at 4.02% (+2bps this morning)

- The US 30-Yr is back above 4.60%. It has risen +1.8bps this morning to 4.61% having shifted below 4.60% and held below last week.

Tonight sees multiple bill issuance, 2-Yr notes, 5-Yr notes as the key auctions for markets.

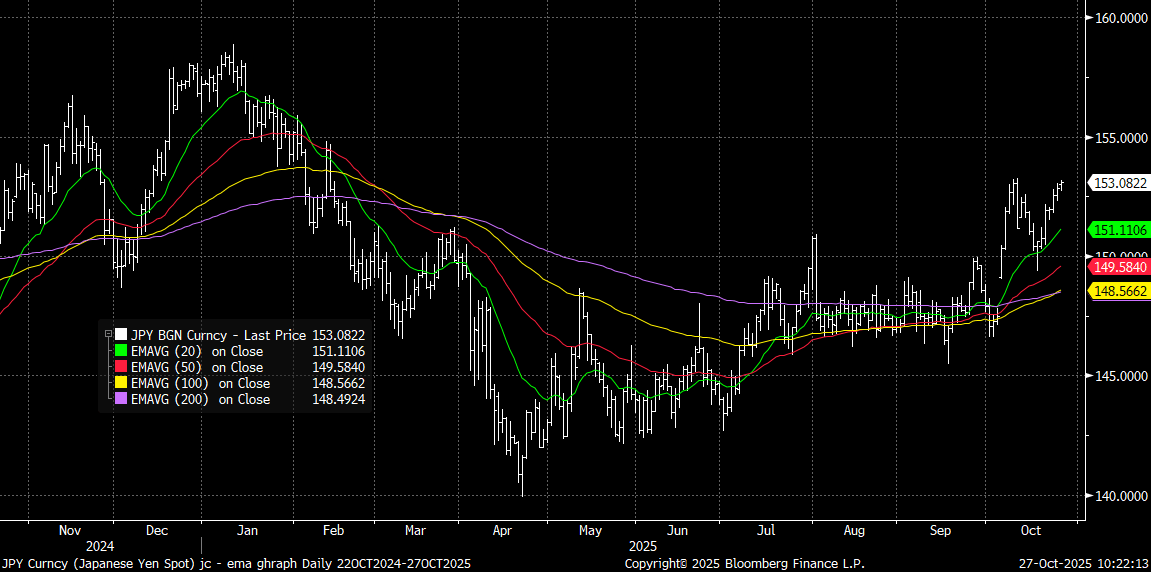

JPY: USD/JPY Close To Bull Trigger, Mkts Likely To Test Resolve On FX Weakness

USD/JPY sits a touch off earlier highs (153.18), but still above the 153.00 level, supported by the early risk on tones in the cross asset space, amid positive US-China trade developments from the weekend. This leaves the bull trigger nearby at 153.27 (which was also the Oct 10 high). A clean break higher opens risks of rally back towards the 155.00 region, see the chart below. On the downside, 151.82 is the Oct 23 low, while the 20-day EMA is back around 151.00

- Lack of concern around yen weakness from Japan officials on Friday was evident. With ministers preferring to refrain from FX comments, which contrasts with the previous Ishiba regime.

- This risks markets continuing to test the resolve around where the new regime's tolerance for FX weakness lies. Even as USD/JPY threatens to break to multi month highs, the 1 mth and 3mth rate of change remain within historical norms.

- The better risk on tone in US/global equities, along with higher US Tsy yields is also working against the yen. AUD/JPY is testing back above 100.00, with earlier Oct highs near 101 a potential upside focus point.

- On the data front, we had the PPI services print earlier, which was above market forecasts, (+3.0%y/y, versus 2.7% forecast). Market reaction has been muted though.

Fig 1: USD/JPY Versus Key EMAs

Source: Bloomberg Finance L.P./MNI