AUSSIE BONDS: Cheaper But Off Worst Levels, No Cash Trading In US Tsys

ACGBs (YM -3.5 & XM -5.0) are weaker but off the session’s worst levels.

- “Australia's manufacturing sector continued to expand in December 2025, supported by rising orders, increased production, and stronger hiring, even as supply constraints and cost pressures intensified, according to a survey by S&P Global published Friday.

The headline seasonally adjusted S&P Global Australia Manufacturing Purchasing Manager's Index (PMI) held steady at 51.6, indicating a modest improvement in manufacturing sector conditions for the second consecutive month.” – MTN via BBG - There is no cash trading in US tsys in today’s Asia-Pac session with Japan out.

- Cash ACGBs are 7-10bps cheaper with the AU-US 10-year yield differential at +64bps (based on US closing levels). At this level, the differential sits around its cycle high, the widest since mid-2022. December's price action has consolidated the differential's breakout above the 30bps range that had prevailed since November 2022.

- The bills strip has bear-steepened, with pricing -1 to -5 across contracts.

- RBA-dated OIS pricing shows tightening across all meetings, with the probability of a 25bp hike rising from 40% for February to 104% by June and 177% by December 2026.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

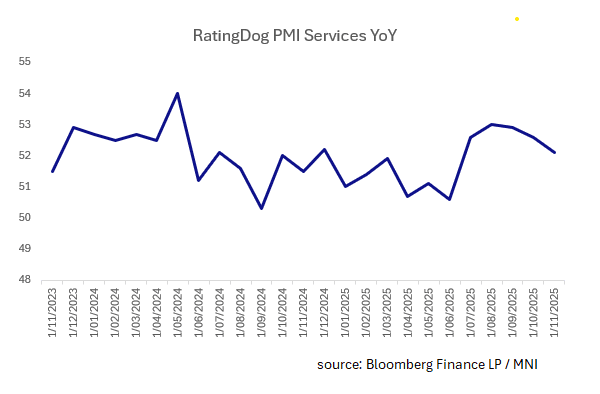

CHINA: PMI Services Moderates Again

- After declining in October, the RatingDog PMI Services fell again in November.

- November's reading takes the index to mid-year levels.

- Within the release some positives were an uptick in employment to 49.2 from 49, yet remains in contraction for the fourth consecutive month.

- Prices charged were up relative to last month.

- When coupled with the RatingDog PMI Manufacturing, the PMI Composite fell to 51.2, the lowest since July.

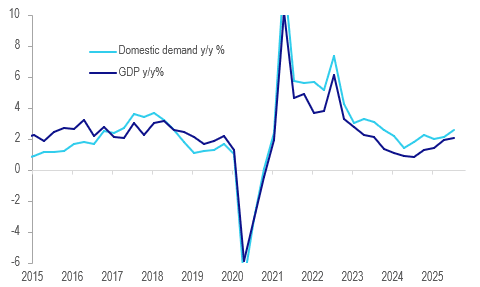

AUSTRALIA DATA: Strong Domestic Demand Growth To Keep RBA Cautious

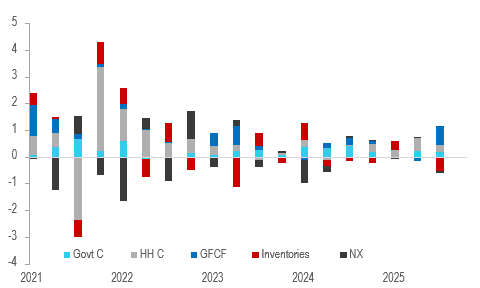

Q3 GDP was lower than expected at 0.4% q/q & 2.1% y/y after an upwardly revised 0.7% q/q & 2.0% y/y. However, the details are a lot stronger than the headline with domestic demand rising 1.2% q/q to be up 2.6% y/y, the strongest since Covid-impacted Q1 2022. The softer GDP print was due to a 0.5pp inventory detraction, largest since Q2 2023, which may reflect stronger demand driving a drawdown and which may be followed by a rebuild.

Australia contributions to q/q GDP pp

Source: MNI - Market News/ABS

- In November, the RBA forecast Q4 GDP growth of 2.0% y/y. Excluding revisions, this would require a 0.5% q/q rise and so growth is developing as it expects. However, it has been around the bank’s estimate of trend and today Governor Bullock said that while the output gap size is uncertain, it probably has closed, which increases risks to inflation from stronger demand. Thus, rates are likely on hold for some time and domestic demand strength poses an upside risk to inflation.

- Private consumption rose 0.5% q/q, concentrated in essential spending, and contributed 0.3pp to quarter GDP. The savings rate rose 0.4pp to 6.4%. A 1.7% q/q increase in disposable income supported expenditure.

- Public consumption rose 0.8% q/q contributing 0.2pp.

- Investment was strong up 3.0% q/q contributing 0.7pp with 0.2pp from the public sector and 0.3pp from private machinery & equipment, which rose 7.6% q/q. Data centre development was a major driver.

- Strong import growth is consistent with stronger domestic demand and especially capex. Imports were up 1.5% q/q & 4.2% y/y after Q2’s 2.5% y/y. Exports were also solid at +1.0% & 3.6% but not enough to prevent net exports detracting 0.1pp.

- The statistical discrepancy made a -0.1pp contribution after Q2’s +0.2pp.

- GDP per capita was flat but up 0.4% y/y.

Australia GDP vs domestic demand y/y%

Source: MNI - Market News/ABS

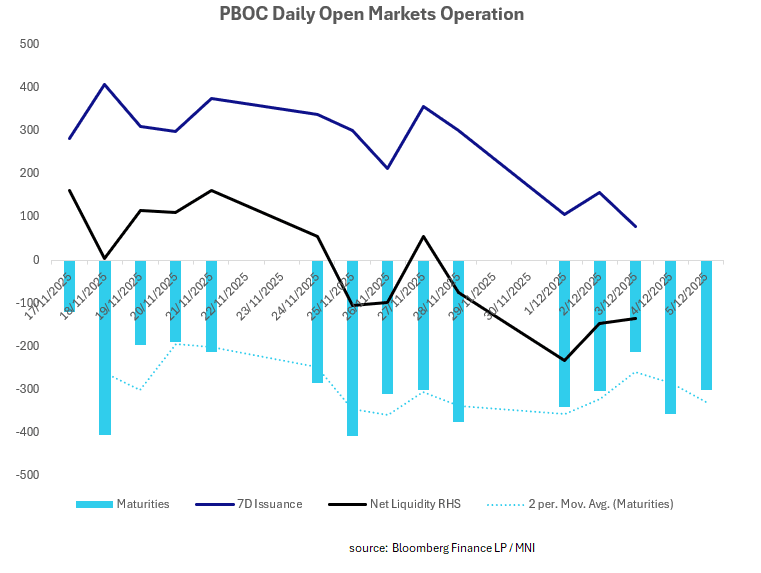

CHINA: Central Bank Withdraws CNY134bn via OMO

The PBOC withdrew liquidity again today ahead of sizeable maturities in the days ahead. Money market / repo rates have largely moderated from prior highs and with the equity market volatility muted, the liquidity need is seemingly reduced.

- The PBOC issued CNY79.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY213.3bn.

- Net liquidity withdraws CNY134bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.44%.

- The China overnight interbank repo rate is at 1.28%, from the prior close of 1.28%.

- The China 7-day interbank repo rate is at 1.41%, from the prior close of 1.48%.