AUSSIE BONDS: Cheapening Ahead Of US Payrolls But Still Richer Than Pre-CPI

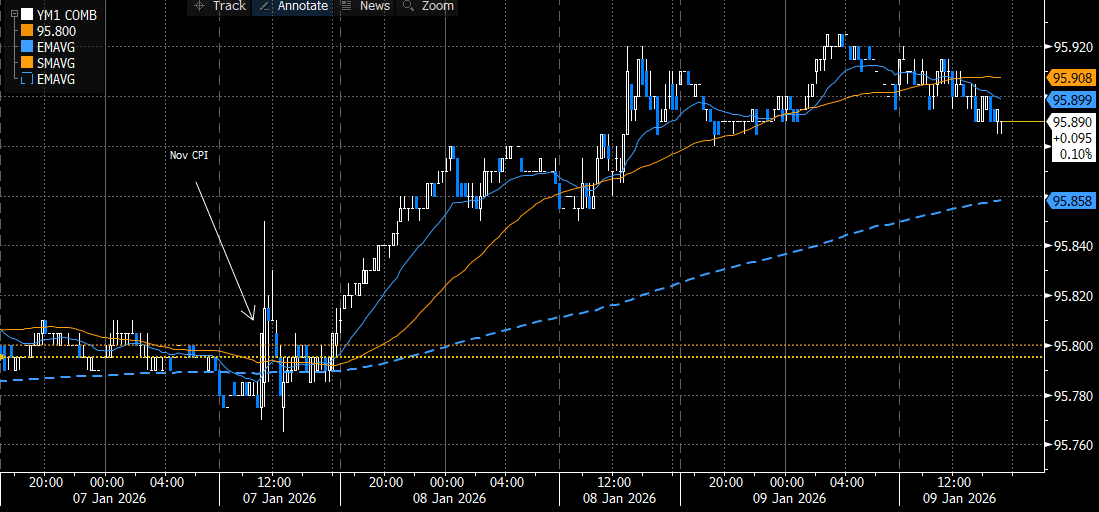

ACGBs (YM -1.0 & XM -2.0) are weaker, hovering near session lows, ahead of tonight’s US payrolls data (see chart).

- Cash US tsys are slightly cheaper in today's Asia-Pac session, with consensus looking for nonfarm/private payrolls growth of 69k/75k.

- Cash ACGBs are 1-2bps cheaper with a steeper curve and the AU-US 10-year yield differential at +52bps, its lowest level since early December. In the month leading into this week's CPI release, the spread had traded in a 55-65bps range, marking its widest levels since mid-2022.

- The price action had effectively consolidated the differential's breakout above the 30bps range that had prevailed since November 2022. This widening coincided with a steady lift in market-implied expectations for the RBA cash rate.

- The bills strip is little changed.

- RBA-dated OIS pricing is 3-13bps softer than Wednesday’s pre-CPI levels, with December 2026 leading. Nonetheless, pricing continues to show tightening across all meetings, with the probability of a 25bp hike rising from 28% for February to 91% by June and 138% by December 2026.

- On Monday, the local calendar will see Household Spending and ANZ-Indeed Job Advertisements data.

- Next week, the AOFM plans to sell A$300mn 4.75% 2054 bond on Tuesday, A$1bn 4.25% 2036 bond on Wednesday and A$700mn 3.25% 2029 bond on Friday.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

BOJ: Rinban Purchase Offer

Today, the BoJ offered to buy a total of Y680bn of JGBs from the market:

- Y300bn worth of JGBs with 1-3 Years until maturity

- Y305bn worth of JGBs with 5-10 Years until maturity

- Y75bn worth of JGBs with 25+ Years until maturity

AUSSIE BONDS: Post-RBA Sell-Off Extends Ahead Of Tomorrow's Jobs Data

ACGBs (YM -6.0 & XM -5.0) have extended the sell-off that started during yesterday's RBA presser by Governor Bullock. As it stands, futures are 6-10bps weaker, with a flatter curve.

- Cash US tsys are ~1bp richer in today's Asia-Pac session ahead of today's FOMC policy decision. Inter-meeting communications reinforced that the FOMC is finely split between those who would ease further and those who are resistant - if not outright opposed - to providing further accommodation.

- Cash ACGBs are 3-4bps cheaper with the AU-US 10-year yield differential at +60bps.

- The bills strip has bear-steepened across contracts, with pricing flat to -6.

- RBA-dated OIS pricing is 1–8bps firmer across meetings today, extending yesterday’s post-press conference sell-off. Markets are pricing a steady build-up in tightening risk, with the implied probability of a 25bp hike rising from 36% in February to 97% by May and 219% by December 2026.

- The spread between the 1-year forward 3-month swap (1Y3M) and the 3-month rate—often used as a proxy for policy expectations a year ahead—has widened by more than 150bps since April, underscoring the magnitude of the shift in rate expectations (see chart).

- Tomorrow, the local calendar will see labour market data, with the market expecting +20k jobs but a higher unemployment rate (4.4% vs. 4.3% prior).

Figure 1: 1Y3M Swap Rate Vs. 3M Swap Rate

Source: Bloomberg Finance LP / MNI

AUD: AUD/USD - Treading Water Just Below 0.6650

The AUD/USD has had a range today of 0.6629 - 0.6647 in the Asia- Pac session, it is currently trading around 0.6640, -0.05%. The AUD/USD has drifted lower today with risk on the backfoot in Asia ahead of the FOMC. US yields continue to rise, the 10-Year is approaching the pivotal 4.20% area as we come closer to the FOMC. The AUD price action remains very constructive and it continues to ignore the pullback in the USD for now. While the AUD remains above 0.6500-0.6550 I suspect dips should continue to be supported. In the Asian session, watch to see if price can continue to hold above 0.6620-0.6630 to rebuild momentum to have another look back toward the 0.6700 area at some point. If that support does not hold I suspect bids will return back towards the 0.6570-0.6600 area. The AUD outperformance is being expressed more clearly in the crosses.

- MNI AU - Nov Unemployment Rate Forecasts Split Between Rise & Unchanged: With the RBA saying this week that “recent data suggest the risks to inflation have tilted to the upside, but it will take a little longer to assess the persistence” and noting signs of capacity pressures, the data before the 4 February decision will be key to the policy outlook. This begins with Thursday’s November job figures. The RBA doesn’t just look at the headline employment and unemployment but also the underemployment & youth unemployment rates as well as hours worked. The split between full-time and part-time will also be important.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6600(AUD822m). Upcoming Close Strikes : 0.6550(AUD1.59b Dec 11), 0.6650(AUD767m Dec 12) - BBG

- The AUD/USD Average True Range for the last 10 Trading days: 36 Points

Fig 1: AUD/USD spot Daily Chart

Source: MNI - Market News/Bloomberg Finance L.P