BUNDS: Bund Issuance Risks Approach

- Bunds have given away their temporary gains following middle east escalation in full, and returned to levels seen earlier this month, around the 2.55% yield mark in the 10y segment. Next to global risk sentiment, domestic factors could prove decisive for price action over the next week:

- A Q3 refunding announcement on 24 June will likely be where we will see a material ramp-up of Bund issuance following the debt brake loosening earlier this year, and that announcement looks likely to be followed by a 2025 budget press conference on 25 June from finance minister Klingbeil.

- DFA (the German DMO) has touted the re-introduction of a 7-year Bund for that refunding - we see a Nov-32 maturity most likely, for more details see page 2 of our EGB Daily Supply publication here.

- The 2025 budget will give more clarity around plans for German public investment rising to E110bln this year (channelled through both the core budget and special funds, from around E75bln 2024), the E46bln tax breaks through 2029 (E9.2bln per year on average, or 1.9% of 2024 federal spending), the military spending increase (potential commitment for a gradual move up to 3.5%/GDP), and a more longer-term debt brake reform and structural reform agenda.

- Despite this push, Finance Minster Klingbeil has urged ministries to identify savings and attempts to signal that fiscal prudence remains key for the current government (similar statements seen from Merz). This also comes amid lower tax estimates for Germany (-E6.7bln/year, around 0.2% of GDP or 1.6% of projected revenues at the federal level).

- We'd not be surprised to see an additional sources report from local media potentially citing net issuance for 2025 in the lead-up to the refunding and budget announcements - we will cover accordingly.

- On balance, JP Morgan think "the peak in German government debt will likely be at around 70% of GDP (versus last year’s 62%), rather than the near-90% that the fiscal space would allow."

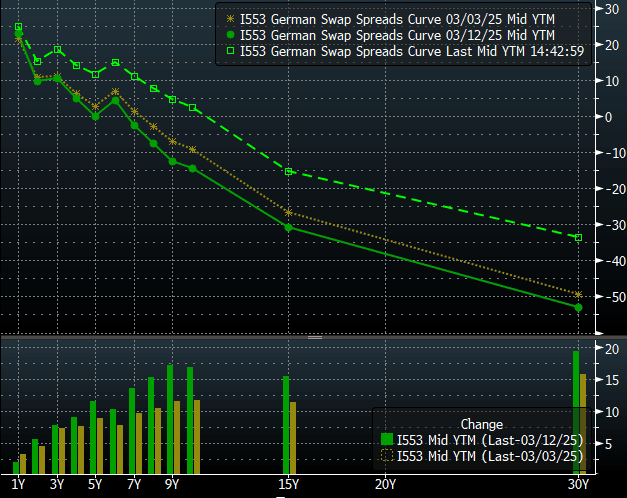

- Swap spreads appear to have largely priced in the German fiscal ramp-up likely being comparatively less pronounced than initially "feared" - since mid-March, German swap spreads have more than reversed their initial tightening seen on the debt brake loosening announcement, widening move than 15bps by now at the long end of the curve.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

EQUITY TECHS: E-MINI S&P: (M5) Trend Needle Points North

- RES 4: 6080.75 High Feb 26

- RES 3: 6057.00 High Mar 3

- RES 2: 6000.00 Round number resistance

- RES 1: 5977.50 High May 16

- PRICE: 5911.00 @ 14:29 BST May 19

- SUP 1: 5837.25/5681.27 High Mar 25 / 50-day EMA

- SUP 2: 5455.50 Low Apr 30

- SUP 3: 5355.25 Low Apr 24

- SUP 4: 5127.25 Low Apr 21 and a key support

A bullish trend condition in S&P E-Minis remains intact and last week’s appreciation reinforces current conditions. The contract has cleared an important resistance at 5837.25, the Mar 25 high and a bull trigger. This strengthens the bullish theme, paving the way for a continuation near-term. Sights are on the 6000.00 handle next. Initial firm support to watch lies at 5681.27, the 50-day EMA.

EUROPEAN INFLATION: Eurozone Services Uptick Was An Easter Effect

As was suggested in final country-level data over the last week, the April acceleration in Eurozone services inflation was largely driven by Easter effects. Services related to package holidays and accommodation rose to 6.73% Y/Y (vs 3.92% prior), while airfares accelerated to 13.77% Y/Y (vs -4.54% prior). Other services sub-components were mostly steady in April.

- Notably, insurance inflation eased to 7.42% Y/Y (vs 8.78% prior). While the monthly rate of 0.55% M/M was still above the 1997-2019 average of 0.40%, it was well below the 1.81% seen in 2024.

- A reminder that NSA services inflation was revised up to 3.98% Y/Y in April (vs 3.93% flash, 3.45% prior).

- On a seasonally adjusted basis using ECB data, services prices rose 0.73% M/M (vs 0.67% flash, 0.28% prior). That meant 3m/3m momentum accelerated to 4.16% (vs 4.08% flash, 3.31% prior).

- Headline PCCI inflation, which is judged by ECB staff as the best indicator of underlying medium-term inflation pressures, was steady at 2.21%. Other ECB underlying inflation metrics ticked up on the month.

- The ECB Governing Council remain more concerned about the growth outlook when it comes to near-term policy. There is a general expectation for wage pressures to continue easing through 2025, which should filter into weaker services price pressures. Friday’s Q1 negotiated wages release is expected to confirm these dynamics.

EQUITIES: E-Minis Tick Lower As China Laments U.S. Chip Guidance

E-minis tick lower (but remain above worst levels of the day) as China issues a statement noting that the recent U.S. guidance warning against the use of Huawei’s Ascend chips.

- China notes that the guidance undermines the consensus that was reached between the U.S. & China at the recent Geneva talks, urging the U.S. to correct its “wrongdoings”.

- This isn’t the first time we’ve seen such rhetoric from China on the matter, with similar comments surrounding the U.S. “abusing export controls” made on Thursday of last week.

- That helps explain the limited nature of the move lower in e-minis, but this does serve as a reminder that some of the recent moderation in Sino-U.S. trade tensions could be quickly reversed if one side doesn’t like the actions of the other.

- A reminder that the step down in tariffs between the two is only in play for 90 days, although the closely watched nationalist Global Times media outlet in China has suggested that the truce should be extended.