EU HEALTHCARE: Bayer AG: S&P Negative

S&P have revised the Outlook to Negative.

• 2Q25 saw €1.7bn in provisions for litigation for glyphosate and PCBs.

• Reduced S&P Adj EBITDA to €6.6bn from €8.4bn forecast.

• Pushes Adj Debt/EBITDA to 4.5-4.7x from 3.7x expected.

• These litigation provisions have a one-off effect on EBITDA which is forecast to recover next year.

• Despite the forecast recovery, the company is constrained in its ability to grow.

• €600m annual milestone payments on past acquisitions will be a drain and cap the ability to make future acquisitions.

• Xarelta loss will be offset somewhat by Nubeqa and Kerendia growth.

• FOCF of €2bn expected in 2025 & 2026 even after €1-2bn of annual cash outflows for litigation.

(BAYNGR; Baa2 neg/ BBBneg / BBB)

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

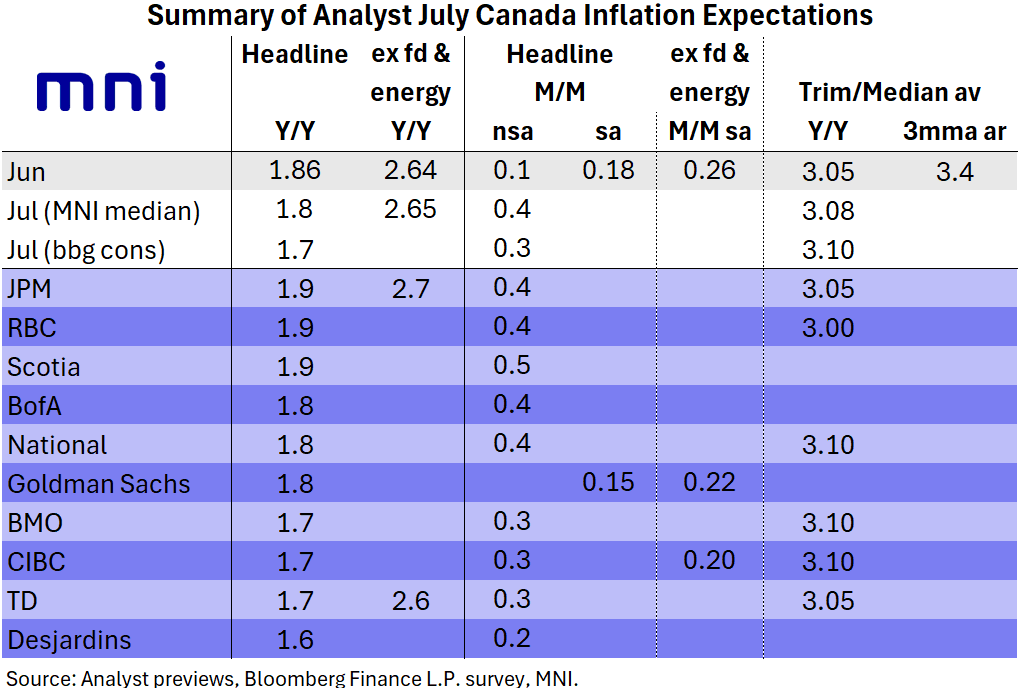

CANADA: Core Pressures Eyed In July CPI

Reminder - July's CPI report (0830ET) is expected to show steady core inflationary pressures on a Y/Y basis but a continued deceleration in headline on a Y/Y basis.

- Current BOC pricing sees roughly 30% implied probability of a September cut, with the first (and only remaining) full 25bp reduction seen only by about March next year. Today's won't be the deciding data in the September BOC decision - it's the first of two CPIs before Sep 17 (and of course we get another jobs report after July's poor numbers, and GDP before then too).

- MNI's median of sell-side analysts sees the average of the trim/median core measures at 3.075%, effectively reflecting an upside bias vs June's 3.05%. See table below.

- However, headline CPI is seen remaining below 2% (1.8% with a slight downside unrounded bias, vs 1.86% prior, all Bloomberg consensus). The M/M headline measure is seen at 0.3-0.4% M/M (vs 0.1% prior; not seasonally adjusted).

STIR: Repo Reference Rates

- Secured Overnight Financing Rate (SOFR): 4.34% (-0.02), volume: $2.810T

- Broad General Collateral Rate (BGCR): 4.33% (-0.01), volume: $1.159T

- Tri-Party General Collateral Rate (TCR): 4.33% (-0.01), volume: $1.134T

- (rate, volume levels reflect prior session)

US TSY FUTURES: September'25-December'25 Roll Update

The latest Tsy quarterly futures roll volumes from September'25 to December'25 below. Percentage complete is running 5% or lower across the curve ahead the "First Notice" date on August 29. Current roll details:

- TUU5/TUZ5 appr 12,300 from -8.12 to -8.0, -8.12 last; 3% complete

- FVU5/FVZ5 appr 37,400 from -4.75 to -4.25, -4.5 last; 6% complete

- TYU5/TYZ5 appr 30,600 from -0.25 to +0.25, +0.0 last; 5% complete

- UXYU5/UXYZ5 under 1,000 from 0.75, .75 last; 2% complete

- USU5/USZ5 appr 2,000 from 13.25 to 13.5, 13.5 last; 3% complete

- WNU5/WNZ5 appr 1,600 from 8.25 to 8.5, 8.25 last; 2% complete

- Reminder, Sep futures don't expire until next month: 10s, 30s and Ultras on September 22, 2s and 5s on September 30. Meanwhile, Sep'25 Tsy options will expire this Friday, August 22.