EUROZONE DATA: Bank Lending Steady Acceleration Trend Intact In July

Aug-28 09:17

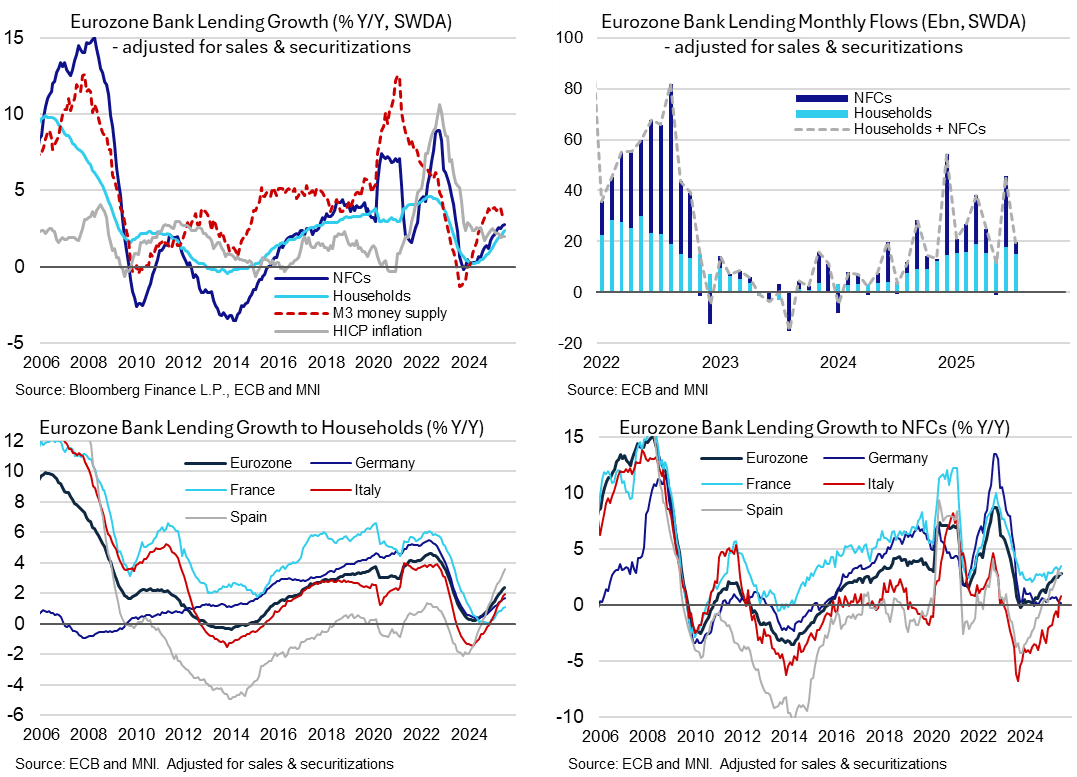

Bank lending to households and non-financial corporations continued its trend of steadily accelerating growth in July. This trend has been driven by relative improvements in lending growth in southern country whilst German lending to NFCs for instance remains particularly tepid. M3 money growth appears to have plateaued for now at least.

- On a sales & securitization adjusted basis, growth in lending to households increased two tenths to 2.4% Y/Y (fresh high since Apr 2023) whilst lending to NFCs increased a tenth to 2.8% Y/Y (fresh high since Jun 2023).

- Accelerating household lending growth was seen across major countries but continued to be driven by southern countries: Spain (3.6% Y/Y, +0.3pp), Italy (2.0% Y/Y, +0.2pp), Germany (1.7% Y/Y, +0.1pp) and France (1.1% Y/Y, +0.1pp). This is a new high since 2008 for lending growth to Spanish households.

- There’s a less clear regional split in lending to NFCs: France (3.5% Y/Y, +0.4pp), Spain (2.8% Y/Y, +0.1pp), Italy (0.8% Y/Y, +0.4pp) and Germany (0.2% Y/Y, -0.1pp). We note the continued improvement in Italy (the 0.8% Y/Y compares to -1.1% in May and -4.0% in Jul 2024) which has lagged an also impressive recovery in Spain. Also note the continued lethargy in German corporate lending, having averaged 0.4% Y/Y since mid-2024.

- Whilst year-ago credit growth continues to accelerate, monthly flows have plateaued, although the E19.7bn in July did follow a strong E45.6bn in June. It’s seen the credit impulse slow to ~1.2% GDP from 2% in Q2 (calculated as 3mth flows vs flows over the same period a year ago).

- M3 money supply meanwhile increased 3.4% Y/Y in July, up from 3.3% in June but softer than the 3.5% expected and below the 3.9% seen in three of the four months through Feb-May. For the monetarists, this compares with an average 4.0% Y/Y in 2018 and 5.0% Y/Y in 2019, periods when HICP inflation averaged 1.8% Y/Y and 1.2% Y/Y.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

ITALY T-BILL AUCTION RESULTS: 6-Month BOT

Jul-29 09:11

| Type | 6-month BOT |

| Maturity | Jan 30, 2026 |

| Amount | E6.5bln |

| Target | E6.5bln |

| Previous | E1.5bln |

| Avg yield | 1.993% |

| Previous | 1.950% |

| Bid-to-cover | 1.48x |

| Previous | 1.64x |

GILT AUCTION RESULTS: Another strong 3-year gilt auction

Jul-29 09:07

- Another strong 3-year gilt auction for the 4.375% Mar-28 gilt.

- The tail of 0.2bp was a little wider than the previous auction's 0.1bp but still very tight while the lowest accepted price (LAP) of 101.057 is higher than any other time of the day (excluding the first 10 minutes of trading).

- The price of the 4.375% Mar-28 gilt is still trading below that of the LAP at the time of writing but is moving higher. Gilt futures have shown little movement despite the strong result.

GILT AUCTION RESULTS: 4.375% Mar-28 Gilt

Jul-29 09:03

| 4.375% Mar-28 Gilt | Previous | |

| Amount | GBP5.00bln | GBP5.00bln |

| Avg yield | 3.941% | 3.847% |

| Bid-to-cover | 3.71x | 3.46x |

| Tail | 0.2bp | 0.1bp |

| Avg price | 101.062 | 101.327 |

| Low price | 101.057 | 101.324 |

| Pre-auction mid | 101.039 | 101.311 |

| Previous date | 02-Jul-25 |