AUD: AUDUSD Recovers Post-CPI With Yield Rebound & Rising Iron Ore

AUDUSD dropped to 0.6717 after the November CPI showed a larger-than-expected moderation in headline inflation but trimmed mean was as forecast at 3.2%. It has recovered since though driven by the rebound in Australian bond yields but also higher iron ore prices even though metals are lower and equities are lacklustre. The pair is currently up 0.2% to 0.6750, close to the intraday high. The USD BBDXY index is off its intraday peak to be little changed.

- AUDUSD approached resistance at 0.6759, 11 October 2024 high. AUDUSD broke above the bull trigger at 0.6728 on Tuesday reinforcing the uptrend.

- The 2-year yield fell to 4.051 following the CPI data but then rose to 4.110 and is now around 4.096.

- Iron ore is up to around $108/t after recently holding between $105.50-106. Copper is down 1.2% though and silver 0.7%. Equities are mixed with the ASX up 0.3% but Hang Seng down 0.8% and S&P e-mini is flat.

- AUDNZD reached a high of 1.1658, the highest since July 2013, on Tuesday and has moved higher during today’s APAC session. It is currently up 0.1% to 1.1657 after an intraday high of 1.1664.

- AUDJPY is also continuing its uptrend and is +0.2% to 105.75 today after falling to 105.238 after Australia’s CPI.

- November CPI inflation data moved in the right direction for the RBA to prolong its pause but still remain cautious as underlying 3-month momentum remains elevated. As this data is only new with little track record, the RBA will be looking to the Q4 data due on 28 January.

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

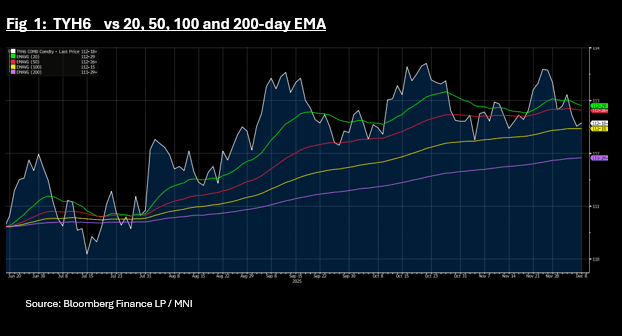

US TSYS: Yields Lower as TYH6 Fails Key Tech Resistance

US bond futures have edged higher in the Asia morning session, with the 10-Yr failing to break below a key technical. Opening at 112-18+ TYH6 was near to the 100-day EMA of 1132-15+ but has bounced higher in early trade to be up by +02 to 112-18+

Cash is stronger across the curve with yields -0.2 - -0.6 lower with short and intermediate maturities outperforming.

- The 2-Yr is at 3.556% -0.6bps

- The 5-Yr is at 3.708% -0.5bps

- The 10-Yr is at 4.133% -0.4bps

- The 30-Yr is at 4.791% -0.2bps.

Ahead tonight is a 13 and 26 week bill auction, with the focus being the U$58bn 3-Year auction.

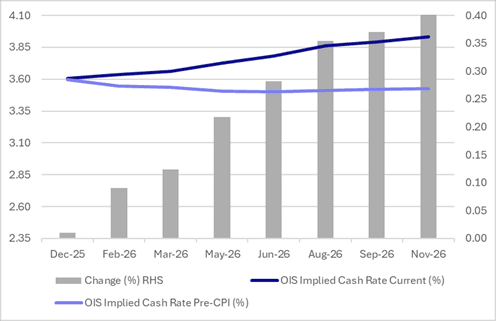

STIR: RBA-Dated OIS Pricing Fully Prices Hike By August 2026

RBA-dated OIS pricing is slightly firmer today, showing tightening across all meetings, with the probability of a 25bp hike rising from 2% tomorrow to 105% by August and 141% by December 2026.

- After today’s move, pricing is 9-40bps firmer across the curve beyond December 2025, than pre-Monthly CPI levels (26 November), led by December 2026.

Figure 1: RBA-Dated OIS – Current Vs. Pre-CPI Monthly

Source: Bloomberg Finance LP / MNI

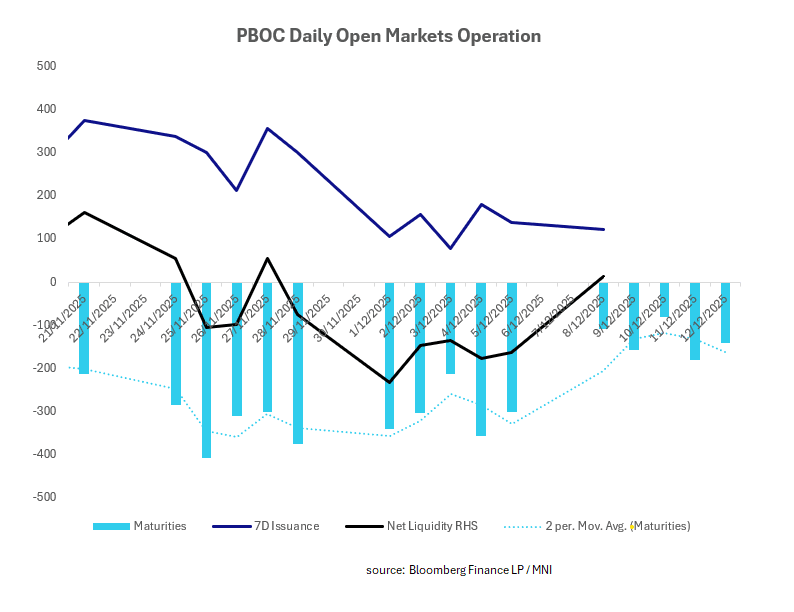

CHINA: Central Bank Injects CNY14.7bn via OMO

Last week the PBOC withdrew 7-day liquidity, adding 3-month liquidity. The week ahead has (relative to last) a more moderate redemption schedule and likely to see the resumption of some moderate injections.

- The PBOC issued CNY122.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY107.6bn.

- Net liquidity injects CNY14.7bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.43%.

- The China overnight interbank repo rate is at 1.31%, from the prior close of 1.31%.

- The China 7-day interbank repo rate is at 1.40%, from the prior close of 1.40%.