AUSSIE BONDS: AU-US 10Y Diff Narrowers May Still Be Premature

ACGBs (YM -10.0 & XM -4.0) are sharply weaker but above the session lows seen shortly after the release of today's October employment data.

- After softer August/September prints, the labour market normalised in October in line with the RBA’s view. The recent trend, if sustained, is likely to keep rates on hold given the Q3 increase in price pressures and uncertainty over policy restrictiveness.

- Cash US tsys are little changed in today's Asia-Pac session. As expected, the US House has passed a bill to reopen the US government, and President Trump has signed it.

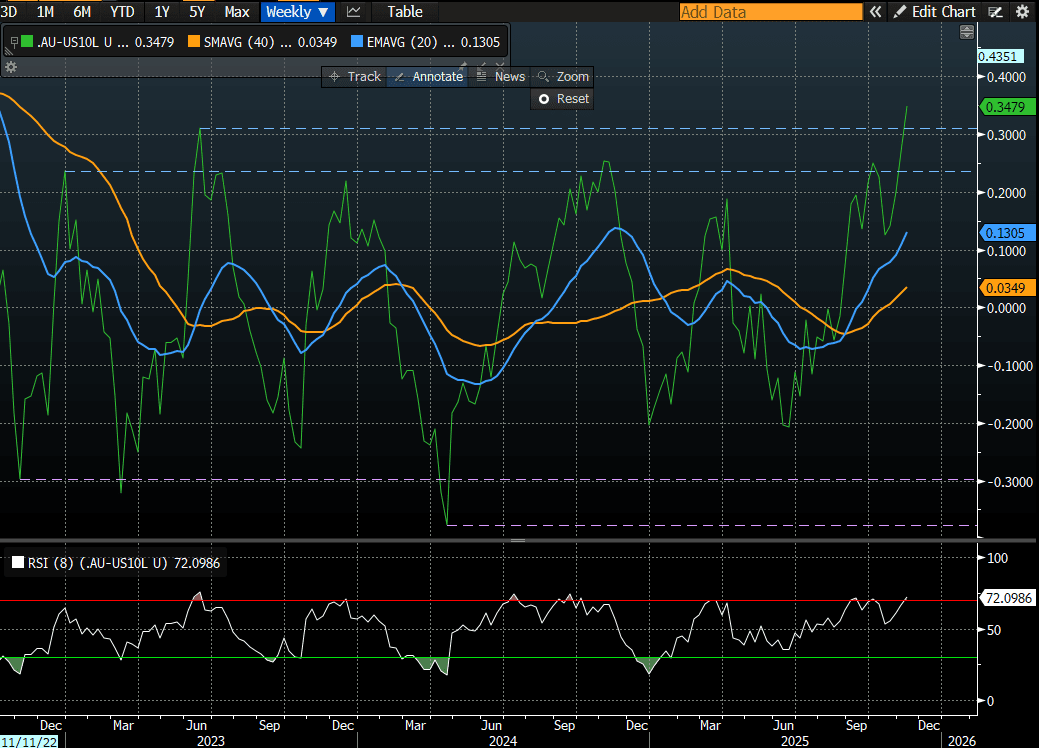

- Cash ACGBs are 6-11bps cheaper than pre-data levels, with the AU-US 10-year yield differential at +34bps. At this level, the differential is through the top of its well-defined +/- 30bps trading range (see chart).

- However, with the market still pricing in almost a 40% chance of a 25bps cut by mid-2026, initiating 10-year differential narrowers may still be premature.

- The bills strip shunted cheaper and steeper, with pricing -2 to -16.

- RBA-dated OIS pricing shows a 25bp rate cut in December at a 1% probability (9% pre-data).

- Tomorrow, the local calendar will be empty apart from the AOFM’s planned sale of A$800mn of the 1.75% 21 November 2032 bond.

Bloomberg Finance LP

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Futures Bid Fresh On US-China Tensions, AU-US 10yr Spread Lower

Futures have caught an afternoon bid amid renewed risk aversion centred on US-China tensions. 10yr futures (XM) were last +4bps to 95.73, while 3yr (YM) were at 96.505, +3bps. Upside focus will rest on Sep 12 highs, 95.78 for the 10yr and 96.615 for the 3yr. Broader risk aversion is higher, as China imposed curbs on the US units of Hanwha Ocean, a large South Korean shipbuilder. It also provided details on a broader probe into the impact of the US investigation into China shipping).

- AUD/USD is the weakest performed in the FX space, and will remain quite sensitive to US-China related developments, particularly from a proxy/risk standpoint.

- ACGB yields are lower across the board, off 2-3.5bps. As we noted yesterday, fresh US-China tensions, with no off ramp, could bring RBA easings back to play if it impacts the global/China growth outlook enough.

- The AU-US 10 spread is off recent highs, last +22bps (from +33bps on Friday).

- Earlier, the September NAB business survey showed the gradual recovery in the Australian economy continued. While, the RBA minutes clearly reflected the Board’s caution at the 30 September decision to keep rates unchanged. Its “decisions”, ie. not just last month’s, “remain cautious and data dependent”. Thus the outcomes of releases between now and 4 November are very important and the tone of the minutes was clear that a rate cut at that meeting is not a given.

BONDS: NZGBS: Softer Yields, Sep Card Spend Down, RBNZ Eases LVR

NZGB yields have held modestly softer across most of the benchmarks as Tuesday's session unfolded. Outside of a steady 2yr at 2.60%, most other parts of the curve are close to 1bps (although the 10yr is little changed at 4.075%). This comes despite US Tsys resuming cash trading with a firmer bias, this has faded as the session progressed, with fresh China shipping curbs on the US weighing on risk appetite (10yr back under 4.04%). Earlier data showed card transactions falling in Sep, while the RBNZ adjusted loan regulations (essentially easing NZ financial conditions), helping relative NZ yield trends.

- The NZ-US 10yr rate differential is slightly lower, last at +5bps, up a touch from recent lows sub 0bps. So far in Oct, this spread hasn't been able to sustain +10bps levels.

- New Zealand 2yr swap is near 2.37%, little changed for the session, but still close to recent lows near 2.35% and maintaining a downtrend bias.

- September retail card transactions fell 0.5% m/m after rising 0.6%, the first negative after three consecutive increases. Annual growth slowed to 1.2%. Despite the soft end to Q3, the quarter saw a 0.6% q/q increase in nominal retail spending.

- The Reserve Bank of New Zealand will ease mortgage loan-to-value ratio (LVR) restrictions from Dec 1, increasing the share of new lending allowed at higher LVRs, the central bank said in a statement Tuesday. For owner-occupiers, the limit on loans with an LVR above 80% will rise to 25% from 20%, while for investors, the limit on loans with an LVR above 70% will increase to 10% from 5%.

- Looking ahead, Thursday delivers Sep food prices, ahead of the all important Q3 CPI, out next Monday.

AUD: A$ Pressured By Risk Pullback Following China Shipping Retaliation

Aussie is underperforming pressured by weaker China/HK equities and US-China tensions over shipping duties due to be implemented Tuesday. China has not only retaliated with a fee on US ships docking at its ports but is also introducing restrictions on Chinese shipping companies’ US divisions. Risk appetite remains very sensitive to US-China developments. AUDUSD breached 0.6500 and is currently 0.5% lower at 0.6482, close to the intraday trough at 0.6481. The USD index is only slightly lower.

- US-China working-level trade talks occurred on Monday and China reiterated today its right to control rare earth exports and that the US should negotiate.

- Kiwi is also impacted by the pullback in risk but less than Aussie leaving AUDNZD down 0.2% to 1.1358, close to the intraday low. It reached a high of 1.1395 following weak NZ consumption data and the RBNZ announcing an easing of LVR requirements. The share of loans with an LVR above 80% will be increased to 25% from 1 December.

- AUDJPY is down 0.8% to 98.436 in the weaker risk environment. It reached 99.485 earlier. AUDEUR is 0.6% lower at 0.5595 and AUDGBP -0.6% to 0.4856.

- The ASX is up 0.1%, Hang Seng down 0.2% and S&P e-mini is flat. Oil prices are now flat with WTI around $59.53/bbl. Copper is down 0.5% and iron ore is around $104/t.

- Later Fed Chair Powell speaks on the economic outlook and monetary policy. The Fed’s Bowman, Waller and Collins, ECB’s Machado, Cipollone and Donnery, and BoE’s Bailey and Taylor also appear. US September NFIB small business optimism prints. On Wednesday, RBA Assistant Governor Hunter speaks and Westpac’s lead indicator for September is released.