AUSSIE BONDS: AU-US 10Y Diff At lowest Since Early December

Jan-08 01:39

Cash ACGBs are 6-7bps richer, extending yesterday's post-CPI rally. * As a result, the AU-US 10-yea...

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

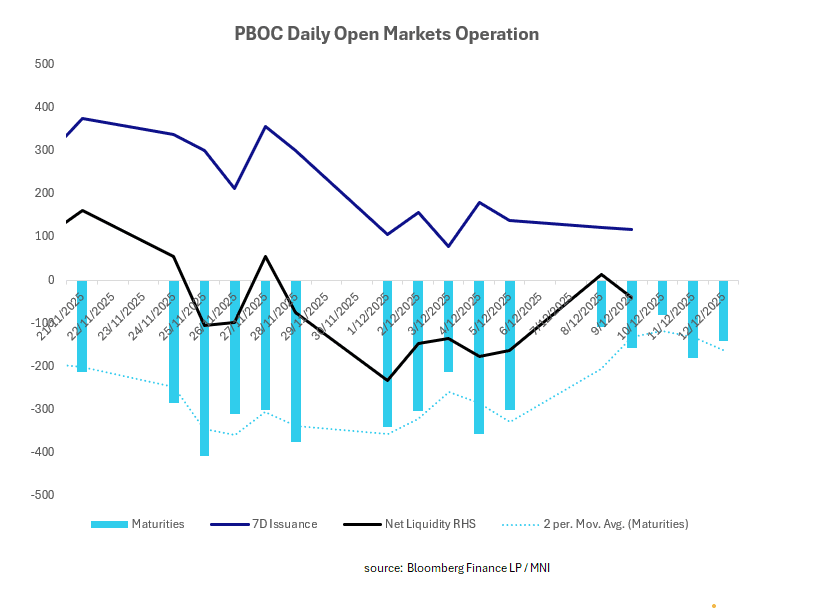

CHINA: Central Bank Withdraws CNY39bn via OMO

Dec-09 01:28

The PBOC kicked off the week with a modest injection yesterday ahead of a light maturity profile for 7-day repos, following the withdrawal of over CNY800bn last week. However today the OMO sees a move back to modest withdrawal despite signs that repo rates are trying to move higher.

- The PBOC issued CNY117.3bn of 7-day reverse repo at 1.4% during this morning's operations.

- Today's maturities CNY156.3bn.

- Net liquidity withdraws CNY39bn.

- The PBOC monitors and maintains liquidity in the interbank system through the issuance of reverse repo.

- The CFETS Pledged Repo Deposit Institutions 7 Day Weighted is at 1.40%, from prior close of 1.44%.

- The China overnight interbank repo rate is at 1.32%, from the prior close of 1.20%.

- The China 7-day interbank repo rate is at 1.43%, from the prior close of 1.46%.

MNI: CHINA PBOC CONDUCTS CNY117.3 BLN VIA 7-DAY REVERSE REPO TUES

Dec-09 01:26

- CHINA PBOC CONDUCTS CNY117.3 BLN VIA 7-DAY REVERSE REPO TUES

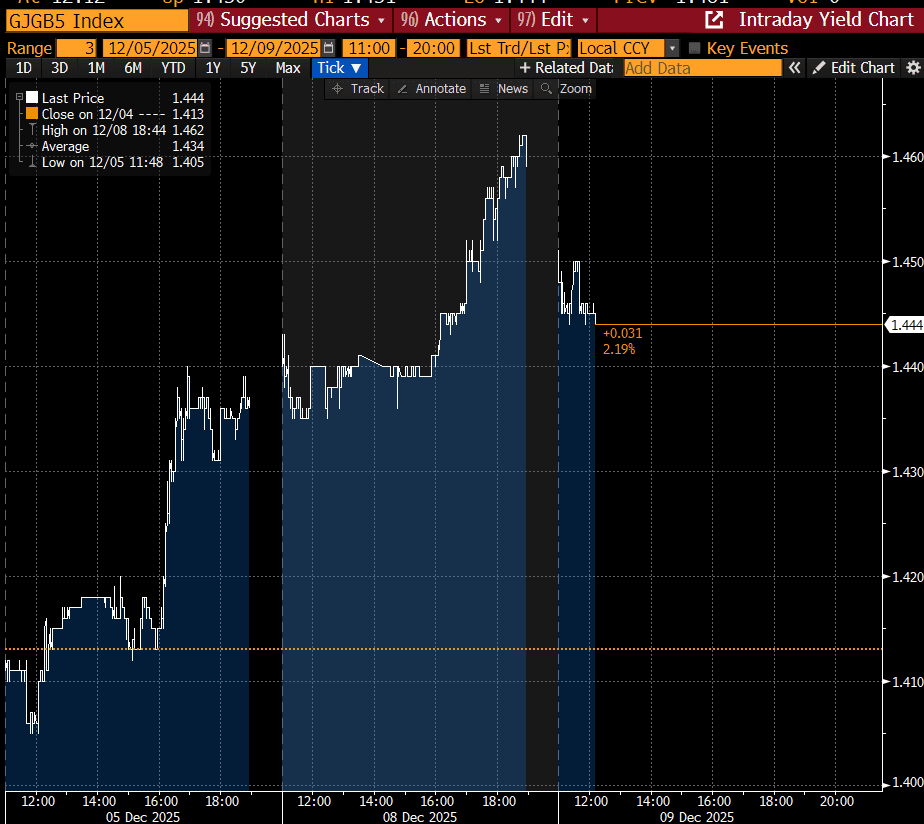

JGBS: 5Y Rally Ahead Of Supply, BOJ Ueda Due In Parliament

Dec-09 01:22

In Tokyo morning trade, JGB futures are stronger, +8 compared to settlement levels, after reversing overnight weakness tied to US tsys.

- BOJ'S UEDA SCHEDULED TO APPEAR IN PARLIAMENT FROM 2:30 PM JT.

- Cash US tsys are slightly cheaper in today's Asia-Pac session after yesterday’s modest sell-off. The Federal Reserve is expected on Wednesday to lower its overnight benchmark rate for a third straight meeting to 3.50%-3.75%, but with dwindling support for continued easing, the bar for further cuts next year moves higher.

- Cash JGBs are slightly mixed across benchmarks, with the 5-year outperforming ahead of today’s supply. The benchmark 5-year yield is 1.6bps lower at 1.445% versus the cycle high of 1.462%, set yesterday.

- While this month’s 10-year and 30-year auctions have delivered strong results, last month’s 2-year auction (28 November) was poor.

- Ahead of the prior 2-year auction, Reuters reported that the Japanese government will increase issuance of 2-year and 5-year JGBs from January as part of its stimulus-funding plan. Issuance is expected to rise by around 100bn each for the 2-year and 5-year tenors. Reuters also noted that there are no changes to the planned issuance for 10-40-year tenors.

- Swap rates are little changed.

Source: Bloomberg Finance LP