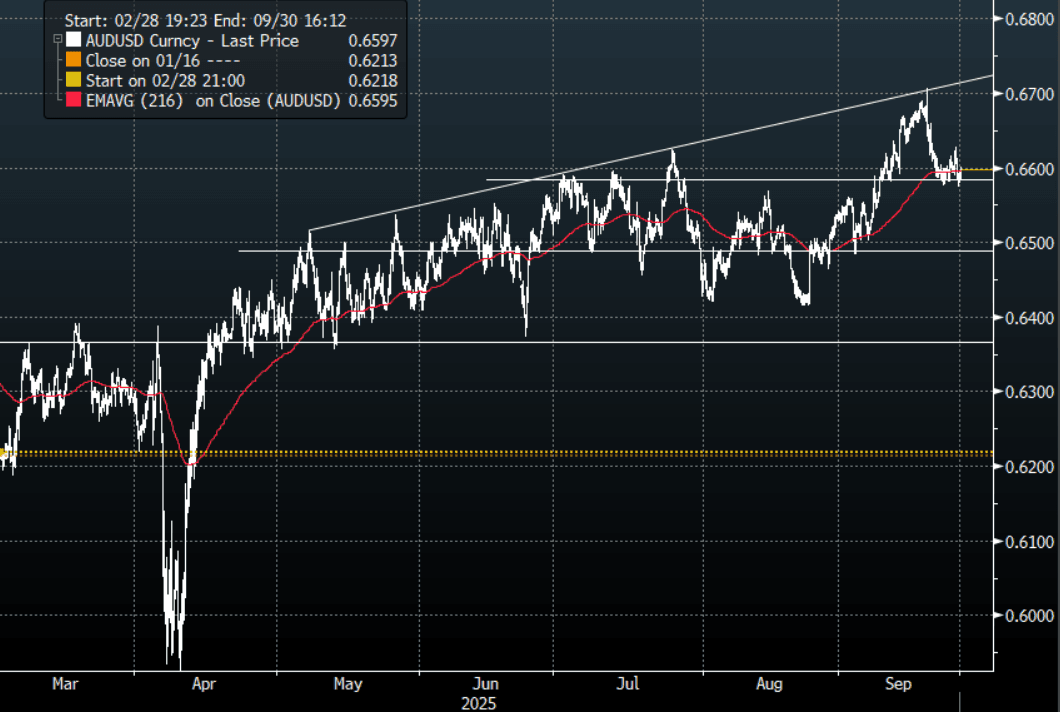

AUD: Asia Wrap - AUD/USD Drifts Back To 0.6600

The AUD/USD has had a range of 0.6581 - 0.6601 in the Asia- Pac session, it is currently trading around 0.6595, +0.20%. The AUD erased a good portion of its overnight losses as the market liked what Fed Governor Daly said regarding further rate cuts. The AUD/USD’s ability to build on this move higher will depend largely on the USD’s fortunes. The first buy-zone below this current support is back towards the 0.6500/0.6550 area should this bout of USD strength extend.

- MNI AU - Vacancies Signal Gradual Labour Market Easing: Job vacancies continued to normalise in Q3 but the pace has slowed implying a gradual easing in labour market conditions. In the 3 months to August they fell 2.7% q/q after rising 2.8% q/q to May but are now down only 1.5% y/y after-2.8% and -16.9% y/y in Q3 2024. The level is in line with February’s. The decline was fairly broad based with the ABS reporting that vacancies fell in 11 out of 18 industries in the 3 months to August. Other services and financial services were the weakest while retail and wholesale saw solid rises.

- MNI AU - Q3 CPI Data Add Uncertainty To Monetary Policy Outlook: The RBA decision is announced next Tuesday 30 September and we believe that it will maintain its caution and keep rates at 3.6%. It continues to focus on quarterly CPI as the monthly series are not yet complete (first full one to be published for October on 26 November but will take time for seasonal factors to be determined). July & August trimmed mean printed at 2.7/2.6% respectively suggesting that Q3 was similar to Q2’s 2.7%. Thus, as in July the RBA is likely to wait for the quarterly CPI on 29 October before deciding to ease.

- Options : Closest significant option expiries for NY cut, based on DTCC data: 0.6400(AUD323m), 0.6730(AUD466m). Upcoming Close Strikes : 0.6600(AUD777m Sept 30), 0.6625(AUD1.29b Sept 29), 0.6725(AUD1.19bm Sept 29) - BBG

- AUD/JPY - Asia-Pac range 97.90 - 98.16, Asia is trading around 98.10. The pair found solid demand back towards 97.00 and bounced yesterday with the help of the CPI print. While above 97.00 the focus will turn to September’s highs toward 98.50.

Fig 1: AUD/USD spot 2H Chart

Source: MNI - Market News/Bloomberg Finance L.P

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

AUSSIE BONDS: Yields Tick Up, RBA Mins Uncertain On Pace Of Easing

Aussie bond futures sit off earlier highs, but have traded tight ranges overall so far in Tuesday trade. YM was last near 96.60, -.01, while XM was last at 95.67, -.02. Earlier highs in this benchmark were at 95.70. Government bond yields are slightly higher across the curve, with the back end slightly firmer from a yield standpoint. US developments have been in focus, with Trump stating he will remove Fed Governor Cook, driving a steeper US yield curve. For Australia, the 3yr ACGB yield was last around 3.39%, up 1bps, while the 10yr was close to 4.31%, up nearly 3bps.

- We had the RBA minutes earlier, where we saw a brief yield pullback but there was no follow through. Given the August decision to cut rates was unanimous, the discussion regarding the outlook was the important part of the RBA meeting minutes. They were clear that further rate cuts were consistent with underlying inflation returning to the 2.5% mid-point of the target band. It was the pace of future easing that “was not yet possible to judge” with the risks around the outlook “in both directions”.

- There hasn't been a strong shift in RBA market pricing, with the OIS dated Dec contract still around the 3.23% level, which is where we ended Monday trade.

- In the swap space we have been relatively steady as well, with the 3yr last close to 3.25%.

- Tomorrow's calendar brings the July CPI print.

BONDS: NZGBS: Front End Yields Lower, Following US Lead, 2yr Swap At Fresh Lows

The initial impetus in NZ government bond yields was higher, but there was no follow through. The 2yr NZGB yield got near 3.04% in the first part of dealing, but we now sit back at 2.98%, off around 3bps. Other parts of the curve are down less in yield terms, but equally have moved off earlier highs. The 10yr was last around 4.36%, off earlier highs near 4.40%. NZ yields look to be largely following US developments, where US President Trump stated he is removing Fed Governor Cook, with immediate effect. This has weighed on front end US Tsy yields, but aided back end yields as the Tsy curve has steepened.

- In the swap space, the 2yr rate has made fresh lows, last near 2.74%, off around 5bps for the session so far. These levels were last seen in the first parts of 2022.

- Local news flows has been light. Via BBG: "NZ July Residential Mortgage Lending Is Highest Since 2021, Gains 36% y/y, Increases 3% m/m after seasonal adjustment: RBNZ". This may point to better housing market momentum, as we progress through the second half. Market expectations remain for further easing, while the RBNZ noted after its easing last week that the lags involved with monetary policy will continue to aid housing market sentiment.

CHINA PRESS: Shanghai No Longer Differentiates Housing Mortgage Rates

The People’s Bank of China’s Shanghai headquarters has adjusted the pricing mechanism for commercial housing loans, removing the distinction between first and second homes, China National Radio reported. The move followed the Shanghai government’s decision on Monday to lift purchase limits on homes outside the outer ring road for local families and for non-local residents with at least one year of social insurance or tax payments in the city, while also raising the loan quota under the personal housing provident fund.