GERMAN T-BILL AUCTION RESULTS: 3/9-Month Bubills

Oct-20 09:33

| Type | 3-month Bubill | 9-month Bubill |

| Maturity | Jan 14, 2026 | Jul 15, 2026 |

| Allotted | E2.446bln | E1.78bln |

| Previous | E2.3bln | E2.03bln |

| Total sold | E4bln | E3bln |

| Target | E4bln | E3bln |

| Avg yield | 1.711% | 1.899% |

| Previous | 1.791% | 1.954% |

| Bid-to-cover | 1.95x | 1.80x |

| Previous | 2.57x | 1.23x |

| Bid-to-offer | 1.19x | 1.07x |

| Previous | 2.36x | 1x |

| Previous date | Sep 22, 2025 | Sep 22, 2025 |

Want to read more?

Find more articles and bullets on these widgets:

Historical bullets

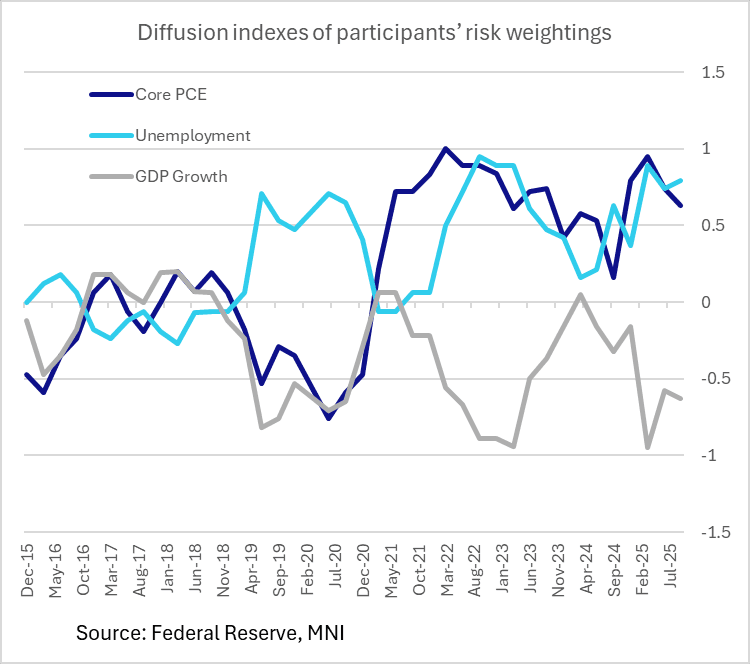

FED: Risks To SEP Forecasts Mostly Away From Recent Extremes

Sep-19 20:14

The FOMC's assessments of risks to its updated forecasts in September tilted a little more pessimistic on growth and unemployment than in the previous edition in June, in keeping with concerns expressed in the Statement about rising risks to the labor market.

- The diffusion index of participants' risk weightings for unemployment ticked up to 0.79 from 0.74 prior, elevated but well below the 0.89 seen in March (when tariff announcements were imminent). And conversely for GDP growth, they ticked down to -0.63 from -0.58 prior, again down from -0.95.

- The latest index showed 0.63 on core PCE, lowest since September 2024, down from 0.95 in March and 0.74 in June.

- This effectively means that the vast majority of the Committee sees risks to their unemployment forecasts as weighted to the upside, with a good number seeing the same for core PCE, and - to the downside - GDP.

- Having upgraded the medians for growth and inflation and lowered the unemployment rate forecast at this meeting, the expressed risks may simply be hedging against the direction of those changes.

- Even so, this is a less pessimistic balance of risks than late 2022/early 2023 when the Fed was still hiking - its core PCE/unemployment concerns were even more tilted to the upside, with GDP seen potentially weaker.

- (The Fed describes the methodology for these indices: "For each SEP, participants provided responses to the question “Please indicate your judgment of the risk weighting around your projections.” Each point in the diffusion indexes represents the number of participants who responded “Weighted to the Upside” minus the number who responded “Weighted to the Downside,” divided by the total number of participants. Figure excludes March 2020 when no projections were submitted.")

LOOK AHEAD: US Data: GDP Annual Revisions and PCE

Sep-19 19:56

- Thursday sees the third release for Q2 national accounts covering GDP and PCE amongst other components. GDP growth is expected to be unrevised at 3.3% annualized although personal consumption could be revised up to 1.9% annualized according to a limited early sample of analysts. Final domestic demand (or PDFP per Powell’s terminology) will be watched after being revised up to a second consecutive quarter at 1.9% annualized in the second Q2 release, still down from the 3% averaged through 2024.

- Note as well that this release comes with the BEA's annual update, which rather than just altering the prior quarter will see changes going back to 1Q20. That should see greater focus on a third release than would usually be the case, including when it comes to the recent core PCE profile.

- Friday’s monthly Personal Income and Outlays report for August will then provide greater clarity on recent momentum. That could include solid consumption growth after a stronger than expected retail sales report for August. Core PCE will also be watched with it widely expected to print softer than the 0.35% M/M seen for core CPI. We saw unrounded core PCE estimates with a median around 0.20-0.21% M/M after the mid-month PPI and CPI releases which could have been lifted by 1bp after import price data. As things stand, that would mark some moderation after the 0.27% M/M in July and 0.26% M/M in June, but would still be a fourth consecutive month running above 2% annualized.

- Away from data, mention also goes to heavy Fedspeak after last week’s FOMC decision. The committee remains particularly divided: taking into account of Wednesday’s cut, 6 members don’t want any more cuts this year (in addition to 1 dot who would have preferred not to cut at all), 2 look for one cut, 9 look for two cuts (i.e. one each meeting) and Miran wants to see rates another 125bp lower.

US PREVIEW: The US Macro Week Ahead: GDP Revisions, PCE, Heavy Fedspeak

Sep-19 19:47

From our Macro Weekly:

- Thursday sees the third release for Q2 national accounts covering GDP and PCE amongst other components. GDP growth is expected to be unrevised at 3.3% annualized although personal consumption could be revised up to 1.9% annualized according to a limited early sample of analysts. Final domestic demand (or PDFP per Powell’s terminology) will be watched after being revised up to a second consecutive quarter at 1.9% annualized in the second Q2 release, still down from the 3% averaged through 2024. Note as well that this release comes with the BEA's annual update, which rather than just altering the prior quarter will see changes going back to 1Q20. That should see greater focus on a third release than would usually be the case, including when it comes to the recent core PCE profile.

- Friday’s monthly Personal Income and Outlays report for August will then provide greater clarity on recent momentum. That could include solid consumption growth after a stronger than expected retail sales report for August. Core PCE will also be watched with it widely expected to print softer than the 0.35% M/M seen for core CPI. We saw unrounded core PCE estimates with a median around 0.20-0.21% M/M after the mid-month PPI and CPI releases which could have been lifted by 1bp after import price data. As things stand, that would mark some moderation after the 0.27% M/M in July and 0.26% M/M in June, but would still be a fourth consecutive month running above 2% annualized.

- Away from data, mention goes to heavy Fedspeak after last week’s FOMC decision. The committee remains particularly divided: taking into account of Wednesday’s cut, 6 members don’t want any more cuts this year (in addition to 1 dot who would have preferred not to cut at all), 2 look for one cut, 9 look for two cuts (i.e. one each meeting) and Miran wants to see rates another 125bp lower.

| Date | ET | Impact | Event |

| 22-Sep | 945 | New York Fed's John Williams | |

| 22-Sep | 1000 | St. Louis Fed's Alberto Musalem | |

| 22-Sep | 1200 | Cleveland Fed's Beth Hammack | |

| 22-Sep | 1200 | Richmond Fed's Tom Barkin | |

| 23-Sep | 830 | * | Current Account Balance |

| 23-Sep | 830 | ** | Philadelphia Fed Nonmanufacturing Index |

| 23-Sep | 855 | ** | Redbook Retail Sales Index |

| 23-Sep | 900 | Fed Governor Michelle Bowman | |

| 23-Sep | 945 | *** | S&P Global Manufacturing Index (Flash) |

| 23-Sep | 945 | *** | S&P Global Services Index (flash) |

| 23-Sep | 1000 | ** | Richmond Fed Survey |

| 23-Sep | 1000 | *** | NAR existing home sales |

| 23-Sep | 1000 | Atlanta Fed's Raphael Bostic | |

| 23-Sep | 1235 | Fed Chair Jay Powell | |

| 24-Sep | 700 | ** | MBA Weekly Applications Index |

| 24-Sep | 1000 | *** | New Home Sales |

| 24-Sep | 1130 | ** | US Treasury Auction Result for 2 Year Floating Rate Note |

| 24-Sep | 1300 | * | US Treasury Auction Result for 5 Year Note |

| 24-Sep | 1610 | San Francisco Fed's Mary Daly | |

| 25-Sep | 820 | Chicago Fed's Austan Goolsbee | |

| 25-Sep | 830 | *** | Jobless Claims |

| 25-Sep | 830 | ** | Durable Goods New Orders |

| 25-Sep | 830 | *** | GDP / PCE Quarterly |

| 25-Sep | 830 | ** | Advance Trade, Advance Business Inventories |

| 25-Sep | 830 | ** | Durable Goods New Orders |

| 25-Sep | 900 | New York Fed's John Williams | |

| 25-Sep | 900 | KC Fed's Jeff Schmid | |

| 25-Sep | 1000 | Fed Vice Chair Michelle Bowman | |

| 25-Sep | 1100 | ** | Kansas City Fed Manufacturing Index |

| 25-Sep | 1300 | Fed Governor Michael Barr | |

| 25-Sep | 1340 | Dallas Fed's Lorie Logan | |

| 25-Sep | 1530 | San Francisco Fed's Mary Daly | |

| 26-Sep | 830 | *** | Personal Income and Consumption |

| 26-Sep | 900 | Richmond Fed's Tom Barkin | |

| 26-Sep | 1000 | *** | U. Mich. Survey of Consumers |

Related bullets

Related by topic

German Fixed Income Securities

EGBs

Germany

T-bills